Thought of the Week

Earlier this week, I walked into The Capital Grille on Pennsylvania Ave. to meet a lobbying colleague for Happy Hour. Renowned as a Republican hangout and lobbyist hotspot, and just a few blocks from Capitol Hill, it’s not unusual to bump into an occasional Senator or House member in the restaurant’s bar, particularly when Congress is in session. So, I didn’t think twice when I ran into Nadeam Elshami, former Speaker Pelosi’s (D-CA) Chief of Staff and Brownstein’s current lobbying practice head, in the lobby. And it wasn’t out of the ordinary when Senator Tim Scott (R-SC) strolled by shaking a few hands as he made his way past me. But then Congresswoman Beth Van Duyne (R-TX) walked in followed almost immediately by Rep. Byron Donalds (R-FL). And then it dawned on us…we were about to be surrounded by those Republican legislators who missed the cut in snagging an invitation to King Charles III’s state dinner. Without delving too deep into the guest list, and making comparisons, the White House dinner list did seem to be tilted in favor of tech titans and billionaires, Supreme Court Justices, and personalities from one particular news network. Still, comparisons can be instructive. Consider that in his comments to dinner guests, King Charles good naturedly pointed out his own comparison when he remarked, “Thank you, Mr. President and Mrs. Trump, for your splendid dinner this evening which, may I say, is a very considerable improvement on the Boston Tea Party!” The royals four-day visit to the U.S. illuminated a number of other comparisons between the two countries and America’s place in the world. For instance, it was noted that if the UK were an American state, it would rank 51st in per capita income but 1st in life expectancy (tied with Hawaii). Scrutinizing World Bank statistics on incomes and poverty rates across 115 countries (excluding a few micro-states like Singapore and Qatar), only Luxembourg, Norway, and Switzerland lead the U.S. in median daily income; the UK comes in 15th, Japan 25th, and China 58th. However, researchers at Johns Hopkins University and the Centers for Disease Control find that despite American affluence, over the last forty years, the U.S. has fallen behind much of the rest of the world across a number of health measures. For instance, on a global scale, the U.S.’s life expectancy of 79 years at birth places it at 44th; figures for Japan, Australia, and the UK are 84, 83, and 81 respectively. According to Johns Hopkins, four preventable causes of death can explain the entire 2+ year gap in life expectancy between the U.S. and UK: cardiovascular disease, overdose, motor vehicle crashes, and gun violence. So, as far as doleful cross-country comparisons go, while Americans might earn more money, they have less time to enjoy it. President Trump ended the night commenting on King Charles’ speech earlier in the day to a joint meeting of Congress stating that Charles “got the Democrats to stand—I’ve never been able to do that.” Perhaps, there’s something to learn from that comparison as well.

Thought Leadership from our Consultants, Think Tanks, and Trade Associations

Eurasia Group Contends that Economic Effects from the Iran War Will Persist Even as Major Disruption Risks Fade. Although a ceasefire has reduced the risk of major global disruptions, prolonged geopolitical risk premiums will keep energy prices above pre-crisis levels. Ongoing supply chain disruptions and Iran’s capacity to restrict Strait of Hormuz traffic will sustain these pressures. The shock will hit growth unevenly, with Southeast Asia and Europe most exposed. In addition, sustained AI investment and supportive fiscal policy, compounded by the supply shock, risk keeping inflationary pressures elevated. The balance of macro risks has shifted to the downside. High public debt constrains policy space, markets have repriced tighter monetary policy across developed economies since the war began, and failure to reach a durable deal will sustain stagflationary headwinds and downside risk to growth through 2026. What’s more, second-order effects of the conflict are likely to last years. Although the ceasefire is likely to hold, the second-order economic costs of the conflict are likely to persist. While near-term crude oil, fertilizer and food, and natural gas price shocks are significant but manageable, the war is likely to accelerate longer term trends toward supply chain resilience, industrial policy, and economic and national security. The U.S. decision to strike Iran and the resulting closure of the Strait of Hormuz has weakened confidence in American decision-making. Deep fissures with NATO allies and efforts to accelerate hedging against U.S. unreliability will amplify economic fragmentation concerns and the future of the global order. The conflict is likely to result in structurally higher risk premiums and costs to firms, moderately higher inflation, and higher interest rates for longer than would otherwise have been the case.

Politico Believes Warsh Will be Confirmed by Mid-May. The Justice Department’s decision to drop its criminal investigation of Fed Chair Powell clears the path for Kevin Warsh’s confirmation by mid-May. Senator Tillis (R-NC) from the Senate Banking Committee had blocked Warsh’s nomination pending the probe’s resolution. With it shelved and Warsh holding majority Republican support, the Senate is likely to move quickly. In fact, Sen. Tillis voted in committee in favor of Warsh earlier this week. Referring the investigation to the Fed’s internal inspector general was a major climbdown for the White House. While the arrangement satisfied the administration’s demand for scrutiny of the Fed renovation, it ended any criminal channel of inquiry and places the probe beyond White House reach. Although Chair Powell will likely resign well before his governor term ends, he announced that he would remain on the Fed board after his chair term ends on May 15, just long enough to see the inspector general’s report. There are three scenarios for Powell going forward: staying on until the June FOMC, until all investigations are concluded (could be months), or past the midterm elections. Markets now price in a 40% chance of a rate cut by year-end, viewing a Warsh led Fed as more dovish.

Inside U.S. Trade Reports Customs’ Refund System ‘Working Successfully,’ So Far. This week, Customs and Border Protection (CBP) gave its first overview of how importers are using the Consolidated Administration and Processing of Entries (CAPE) portal to seek refunds of the International Economic Emergency Powers Act (IEEPA) tariffs that the Supreme Court overturned in February. During its first week of operation, CBP’s tariff refund system received more than 75,000 claims covering over 10 million shipments, of which nearly 1.74 million have now been liquidated, clearing the way for payments to the original importers or their agents. Of the 75,306 declarations, 47,315 had passed “file validations” and moved on to processing. Because an importer can combine many shipments into a single declaration, those claims cover more than 10 million individual entries. CBP says it will take 60 to 90 days for submissions to move through the system. The current program is described as “Phase One” of CAPE, and it lacks the capacity to handle certain “complicated scenarios,” such as applications for IEEPA refunds on shipments that also have pending antidumping or countervailing duties. This initial system is expected to be able to handle about 63% of all entries that triggered IEEPA tariffs; the validation process is designed in part to filter out declarations for shipments that fall into the remaining 37%.

“Inside Baseball”

Bad News Polls for House Republicans. A new crop of House Republican-commissioned polls offers fresh insight into the political environment and a midterm warning sign for the GOP. Conservatives For America, a political organization linked to Republican Study Committee Chair Pfluger (R-TX), posted nine polls for GOP-held districts on its website. These polls, conducted in mid-March by Ragnar Research Partners, are of districts that range from deep-red ones to battlegrounds. What stood out from the data: First, President Trump’s numbers. President Trump is underwater in districts that he won in 2024. Obviously, he isn’t on the ballot this November, but if his poll numbers sink low enough, the president could pull vulnerable Republicans down. Although some vulnerable House Republicans have better numbers than President Trump, the danger is these GOP incumbents may not be able to run ahead of a slumping Trump. Second, generic ballots. Because Democrats are winning the generic ballot in many of the individual race polls, the numbers only underscore the GOP challenge. The good news for the GOP: most of the Republican incumbents beat their Democratic opponents in head-to-head polls. Still, it should be noted that most, if not all, of these Democrats have yet to begin advertising to raise their name ID, and it’s typical for an incumbent to lead at this point in the cycle. Democrats certainly have room to grow.

In Other Words

“In the immediate aftermath of 9/11, when NATO invoked Article 5 for the first time, and the United Nations Security Council was united in the face of terror, we answered the call together as our people have done so for more than a century, shoulder to shoulder, through two world wars, the Cold War, Afghanistan, and moments that have defined our shared security,” King Charles III to a joint meeting of Congress conveying the message that the U.S. not renege on Article 5 because the British were there when it counted. (King Charles: The hidden messages in his speech to Congress – POLITICO)

“Of course not,” House Minority Leader Jeffries (D-NY) when asked if impeaching President Trump would be a priority if Democrats take back the House; although there will be pressure to impeach the president from the left wing of the Democratic party, the need for 67 votes in the Senate to remove the president means any impeachment effort would be doomed to fail.

Did You Know

At the end of March, the national debt hit 100.2% of Gross Domestic Product (GDP), according to the Bureau of Economic Analysis (BEA). Debt held by the public on March 31 was $31.27 trillion, while nominal GDP was an estimated $31.22 trillion over the prior 12-month period. With debt now above 100% of GDP, it seems only a matter of time until the U.S. passes its all-time record of 106% reached in the immediate aftermath of World War II.

Graphs of the Week

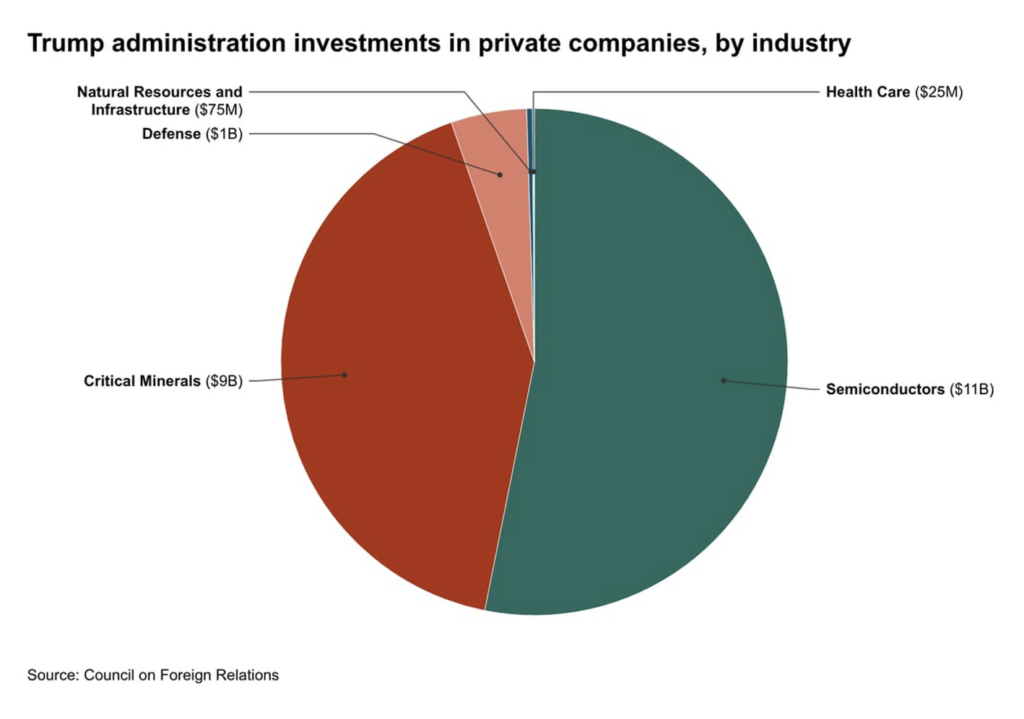

The Trump administration is in talks to finance up to $500 million to rescue Spirit Airlines, in a deal that could give the government as much as a 90% equity stake in the carrier. This is not an isolated move: The Council on Foreign Relations’ U.S. Government Deal Tracker shows that the federal government has invested $20.9 billion across 16 deals since President Trump took office. While most of the investments the administration has made are in critical minerals, semiconductors, and defense, the intervention in the struggling airline demonstrates a strategy extending to a wider range of industries.