Thought of the Week

It’s a lazy Sunday afternoon, your to-do list is checked off, and it’s raining outside. You nestle into your favorite spot on the couch, and with remote in hand, start scrolling through the cable TV guide. You’re tired of watching the news, the regular season sports matchups look boring, and you’ve already binged-watched most of Netflix’s top ten. Then you come across it, the movie you’ll stop and watch whenever it comes on. For me, it used to be Gladiator; more recently, it’s become Whiplash, the multiple Academy Award winning film that tells the story of an aspiring jazz drummer who is pushed to his limit by an abusive instructor. Which got me thinking: official D.C. is going through a kind of whiplash of its own. Over the past year, to win favor, corporate America spent millions of dollars hiring Trump-tied lobbying firms and donating to presidential priorities, like the White House ballroom. With the president’s approval numbers flagging heading into this year’s midterm elections, business reps are beginning to plot what to do if the script is flipped and Democrats win the House and/or Senate. Although winning a single house of Congress would not provide Democrats with the power to push through legislation, the Party would acquire the ability to launch investigations, issue subpoenas, and haul business and agency leaders into hearings. According to political strategists we’ve spoken to, Democratic leaders are itching to lead high-profile oversight hearings investigating not just President Trump but also the companies and industries who have benefitted from his tenure over the past two years. The whiplash for lobbyists now will be in making inroads with Democrats while trying to remain on good terms with the White House. Such an abrupt U-turn on K Street has historical precedence. When Democrats won control of the House in 2018, they not only impeached the president but also held oversight hearings that called business and industry leaders to Capitol Hill. With rising populism in both parties, the politics of this year’s election will be a factor in the next Congress, and no doubt, the risk to entire industries and individual companies could escalate quickly. It is for this reason that the Washington office maintains relationships with firms that have connections on both sides of the aisle, and over the course of this year, we’ll also be reaching out to staffers representing districts where SCOA has a presence to prepare for the 120th Congress.

Thought Leadership from our Consultants, Think Tanks, and Trade Associations

Eurasia Group Says the Reversal of the EPA’s “Endangerment Finding” Will Limit Climate Regulation Long After the Trump Administration’s End. The rollback of the Environmental Protection Agency’s (EPA) “endangerment finding” on greenhouse gas emissions is a major shakeup of the environmental regulatory landscape in the U.S. that, combined with the overhaul of Social Cost of Carbon calculations, removes the legal and economic basis for a large portion of climate regulation. Although auto producers will see limited upside from the rollback as they balance lower compliance costs in the U.S. with the need to meet regulatory standards in international markets, over the medium- and long-term, the rollback will disincentivize renewables expansion. What’s more, any future Democratic administration will face substantial hurdles to reimposing the finding quickly, due to the need to conduct a full rulemaking process, likely preventing an immediate U-turn early in a Democratic term.

National Journal Asks Whether House Democrats Can Cross Over with Voters. Based on President Trump’s deteriorating approval ratings and voters’ sour take on the economy, analysts continue to make bullish cases for House Democrats in this year’s midterm elections; however, any forecast of a “Blue Wave” probably needs to be tempered. Regardless of how good the fundamentals may appear for the minority party, their upside is simply not as great as it was in 2018, when Democrats gained 41 seats in President Trump’s first-term midterm. Looking at the data, the Democratic Congressional Campaign Committee (DCCC) has identified 44 seats it would like to flip. When those districts are mapped to the 2024 presidential vote, the average margin is Trump +7, remarkably similar to the Trump +6.7 average the DCCC targeted in 2018. What’s different this year is the raw number: in 2018, Democrats’ “Red to Blue” campaign targeted 92 districts, winning 43 of them (47%); Democrats also targeted 25 GOP held seats Hillary Clinton carried two years earlier; and when redistricting is factored, there are only five such districts on their list that Kamala Harris carried in 2024. Crossover districts are largely a thing of the past, as voters have retreated to partisan corners up and down the ballot. This demonstrates the fundamental problem for Democrats who predict a wave election—by historical standards, there is a lack of pickup opportunities. Consider if Democrats win their target districts at the same 47% clip as in 2018, that will yield 20 seats, well below the post-World War II average minority party midterm gain of 28 seats. If they were to flip only the five crossover districts (and defend all their current seats), they would have one of the smallest House majorities in history. Because Democrats’ ability to have a great night will depend on how deeply they can crack the parliamentary wall voters have constructed, talk of a “Blue Wave” is probably wishful thinking.

Observatory Group Believes the Latest CPI Does Not Give the All-Clear for More Fed Rate Cuts. It is surprising how the financial markets reacted to last week’s January CPI release. The y-o-y reading fell to 2.4%, the lowest in several years, while the headline m-o-m number was 0.2%, a little better than expected. These factors led to a great deal of talk that the FOMC would now have more scope for rate cuts, and market pricing for Fed moves immediately jumped toward more cuts this year; it is now close to three cuts (as an aside, the core m-o-m January CPI was 0.3%, which does not bolster the case for cuts in the short run). What’s more, the breakdown showed that core services rose 0.4% from December to January while core goods prices hardly moved at all. Recall that at his most recent FOMC press briefing, Chair Powell said that the risks to both the inflation and employment mandates had eased in recent months, and his comments on inflation were pointed:

- While 2025 inflation did not improve from 2024, the composition was encouraging.

- Although the stickiness of core services prices had eased, goods prices, reflecting the impact of tariffs, rose in 2025.

- The median outlook for a rate cut in 2026 would depend on continued improvement in core services prices and that any tariff effects would have topped out in early 2026 without having triggered a renewed inflationary dynamic.

In other words, the current policy outlook rests on services prices continuing to ease and goods prices not accelerating. The January m-o-m data do not deliver that result. If one was going to go out on a limb concerning rate cuts, they need to wait for the January PCE report, which has more weight in the Fed’s policy debate than the CPI.

“Inside Baseball”

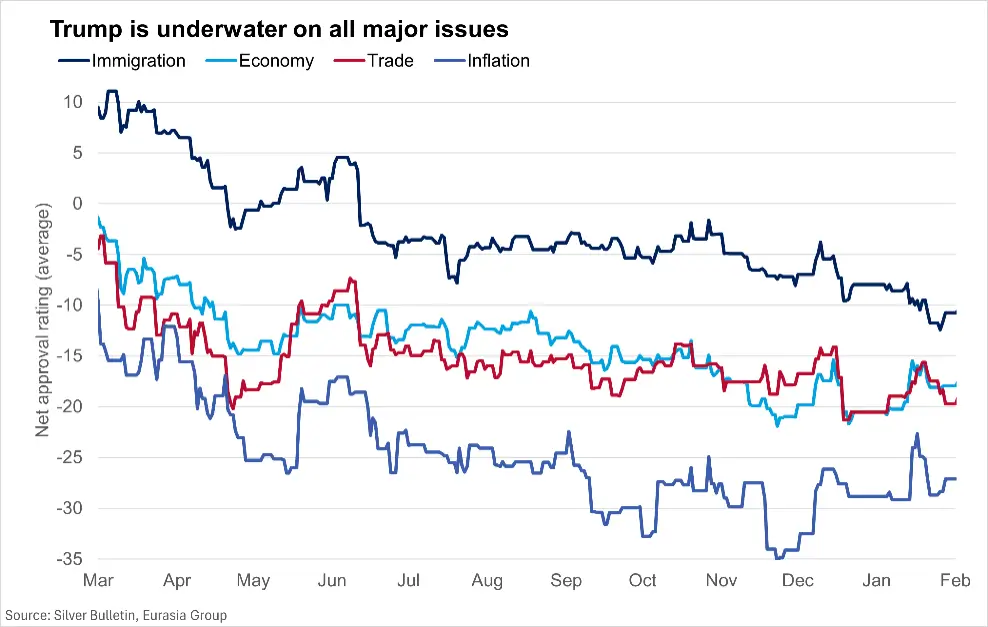

President Trump is Not Digging Himself Out of His Polling Hole. Recent polls would seem to indicate that the Trump administration remains broadly unpopular. In fact, President Trump’s approval rating has fallen below 41%, the lowest of his term so far. Signs of the mid-2025 rebound in voters’ views of the economy and of the country’s direction have disappeared—only 34% of voters have a positive view of the economy, while just 29% believe the country is headed in the right direction, and on specific policy issues, public opinion has turned decisively against the White House. As demographic groups return to their historic baselines, there are growing signs that the coalition of unusual Republican voters that President Trump cobbled together in 2024 is falling apart. Both the negative mood and the shift in issue-specific polling (see chart) are substantial headwinds for an incumbent administration and point to a Democratic-leaning national environment in the midterms, even making the Senate a more plausible flip (35% odds). To dig himself out, at a minimum, the president needs strong job growth and low inflation over the next year. Going forward, ahead of the midterms, congressional Republicans are increasingly likely to seek to differentiate themselves from the administration.

In Other Words

“The end of the transatlantic era is neither our goal nor our wish…we will always be a child of Europe,” Secretary of State Rubio during his speech at the Munich Security Conference.

Did You Know

George Washington is the only American president to be elected unanimously, and he did it twice. Washington won the electoral votes of all ten states that participated in the first election in 1788 (New York, North Carolina, and Rhode Island did not participate), and in 1792 he carried all 15 states.

Graphs of the Week

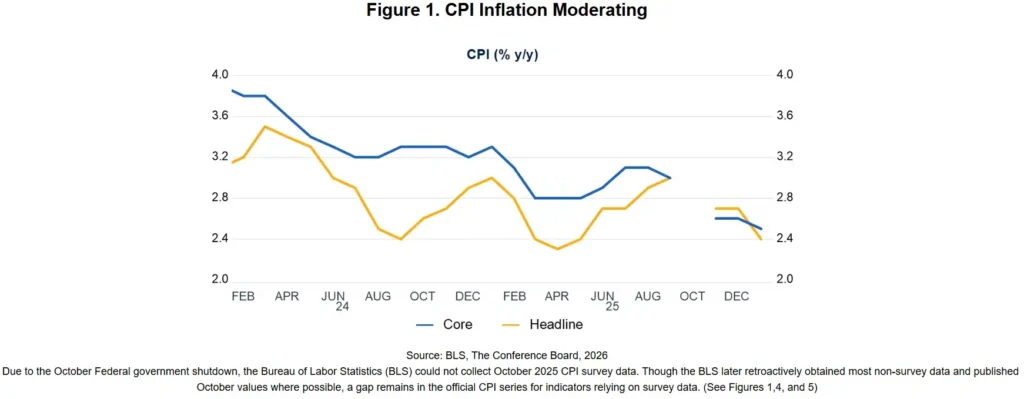

Conference Board Says January CPI Raises More Questions Than It Provides Answers. Moderating inflation in recent months suggests that the Fed may cut rates later this year, even if the FOMC puts cuts on hold in H1. While inflation is expected to rise over the coming months, it should subside in the second half of the year. Despite the improving consumer price index (CPI) picture on the surface, underlying details are less clear. In fact, the Fed’s preferred inflation gauge, the PCE deflator, shows an expected rise in coming months; the December release on February 20th is likely to show core inflation (total excluding food and energy) approaching 3.0% y/y, up from 2.8% in November. The CPI and PCE inflation paths have diverged lately, partly because of uncollected data for the CPI during the federal government shutdown at the end of 2025. While PCE inflation is forecast to peak in H1, the goods CPI inflation has not reached its apex as tariffs continue to flow through the economy and should eventually overwhelm the recent moderation in services prices. While services inflation continues to moderate, it remains sticky, particularly in certain categories related to discretionary spending by higher income households, such as airline fares, insurance, and recreation.