Thought of the Week

Thought of the Week

I remember the United States’ Bicentennial celebration, and it was glorious. My parents bought me a 1976 proof set as a gift, which I still have in a shoebox full of Indian Head pennies, Mercury dimes, and Morgan silver dollars. To this day, I separate that year’s quarter with the dual 1776-1976 dates on the front and the Colonial drummer on the back from the rest of my change. That spring, I made my first visit, an elementary school field trip, to Ft. McHenry where “The Star-Spangled Banner,” the U.S.’s national anthem, was written, and I saw the tall ships float into Baltimore’s Inner Harbor. My father made it a point for me to put the flag out in the morning and take it down before sunset, and it seemed like the entire country was on board. I’m not getting that same kind of vibe for this year’s Semiquincentennial celebration, at least not yet. I don’t know. Maybe it’s because I’m not a kid anymore, and I’m just too jaded. Maybe it’s because my own kids are already grown. Maybe it’s because of the hyper-partisan environment we all live in that seems to taint everything in the nation’s capital. Or maybe it’s just because the chill of winter hasn’t quite left D.C. I know, I know. There will be Fourth of July fireworks; a re-creation, called Sail250, of the Bicentennial’s tall ships and military vessels parade, with Baltimore being one of the host cities; and, in two firsts, the president has announced that the UFC Freedom 250 will be held on the White House lawn and the Freedom 250 IndyCar Grand Prix will wind through the streets of downtown Washington. Although I’m sure I’ll witness a burst of patriotic sentiment as July 4th approaches, with the Department of Homeland Security (DHS) shutdown, ongoing war with Iran, percolating midterm election partisanship, and my own Congressman’s contention during a subcommittee hearing that Founding Fathers Thomas Jefferson and Thomas Paine were “undocumented immigrants,” I’m just not feeling it. For business, July 4th isn’t just a holiday this year; it’s actually one of 2026’s trickiest reputational moments. A discussion I had with Gravity Research, who is tracking how companies are navigating America’s 250th anniversary, revealed that the picture is messier than most companies realize. Consider that although B2C companies are 3 times more likely to sponsor America250 than their B2B counterparts, most are staying quiet about it; nearly half of all executives have ruled out sponsorship entirely and 36% are still undecided; and confirmed sponsors are avoiding any public promotion of their involvement. What’s more, the conflation between America250 (a bipartisan, congressionally mandated commission) and Freedom 250 (a White House-aligned initiative) means that any formal affiliation carries a degree of political exposure regardless of which entity a firm supports. Who would have ever guessed that celebrating the nation’s founding would involve a serious political risk calculation; that was never mentioned on my field trip.

Thought Leadership from our Consultants, Think Tanks, and Trade Associations

CSIS Delivers Policy Upshots Concerning the War in Iran. According to the Center for Strategic and International Studies (CSIS), the war with Iran could well be a case where President Trump’s normal pattern—act, wait to see what happens, react, rinse, and repeat—will not work. Having no coherent goal or strategy and only a set of ever-changing tactics is not a recipe for quick success, as the world is beginning to see. Things may get even worse if the war ends up lasting longer. Price increases will become supply shortages that lead to factory closings, primarily in Asia, that, in turn, will force Western manufacturers to once again readjust their supply chains, if they can find any locations that are not, or minimally, impacted. If a company doesn’t know what is going to happen next, it makes contingency plans, holds onto its money, and waits for the situation to stabilize; this increasingly seems more likely to take an extended period of time. What’s more, even a short war will fundamentally change the way investors look at countries previously deemed safe and reliable, like the Gulf states.

Observatory Group Says Republicans are in Trouble. Considering the erosion in President Trump’s sustained approval rating; the political fallout from immigration enforcement; and the persistence of the affordability issue, now compounded by the U.S.-Iran conflict, the momentum for Democratic success in the 2026 midterms for both House and Senate control is trending stronger. Although it appeared, until very recently, that the Senate would remain in Republican control, and on paper, it still should, views have shifted to there now being a 50/50 chance that Democrats take the Senate. Because there was already an 85% chance of Democrats taking the House, Republicans now risk losing the entire legislature. If Democrats secure control of Congress, expect there to be far more confrontation with the executive branch, minimal legislative activity, a slowdown in regulatory reform with Senate confirmations being blocked, and maximalist executive action particularly in foreign affairs. In fact, there could be a huge increase in Congressional investigations of the administration, including the start of impeachment proceedings against President Trump. In addition, there could be much more Congressional oversight of companies, as happened after 2018, even if Democrats only take the House. Therefore, in 2027, Big Business could face: higher reputational risks, for example from awkward questioning in front of committees; a greater volume of hostile litigation; and higher compliance burdens, with things likely to be far worse for those companies that Democrats believe are/have been close to the White House.

National Journal’s Charlie Cook Says a Massive Midterm Wave Isn’t Forming. We live in an era of not just hyper-partisanship, but negative partisanship, where partisans hate the other side even more than they love their own. Thus, many voters tend to see politics on a binary basis. Every election is seen as either a landslide victory or an unmitigated disaster. There is little appreciation, much less tolerance, for gradations between those extremes. Republicans’ chances of losing their House majority are about as high as they could possibly be. The GOP edge in the chamber is currently 218-214, with three vacancies. If you push the vacant seats in the direction they would likely go, the advantage expands to just 220-215. Almost any loss would be sufficient to change control, and President Trump’s poor job-approval numbers, averaging just 41%, ensure that he will be a serious liability in swing districts. So, it’s inevitable that we hear declarations that a “blue wave” is coming. Yet, this ignores a set of factors that make it unlikely GOP losses will match the past Democratic waves of 2006 and 2018. True, the president’s approval ratings among Democrats (in the single digits) present a nightmare scenario for any Republican seeking reelection in a blue district, but only three Republicans sit in districts that VP Harris won. Among independents, President Trump’s approval ratings are in the high 20s or low 30s, but gerrymandering and political self-sorting by the population has shrunk the number of purple districts, diluting independents’ power. In fact, there are very few Republican-held seats in much peril. Among Republicans, the president’s approval ratings remain in the 80s, and stories of a split in the base are not found in the data. MAGA support is so deep that nothing—not the Epstein files nor the attacks on Venezuela and Iran—are peeling voters off; meaning, Democrats have their work cut out for them to flip any red districts. According to the latest The Cook Political Report with Amy Walter, only 17 GOP seats are rated as Toss Up or worse. Adding in the those deemed “Lean Republican” only brings in three more GOP seats, well below the post-World War II average midterm outcome of a 26-seat loss for the president’s party. Including the 15 GOP-held seats in the “Likely Republican” category brings the total to just 35 vulnerable seats. Democrats could nearly run the table, hold all their vulnerable seats, and still fall short of their 2006 or 2018 pickups.

“Inside Baseball”

Iran War May Permanently Reshape Global Energy Markets. According to Eurasia Group energy analysts, the Iran war has severed 15–20% of global oil and LNG supply via the Strait of Hormuz closure, triggering price spikes that threaten power, transport, heating, and cooking fuel across Asia, which buys roughly 80% of Gulf oil and gas. Governments are confronting policies previously ruled out: Japan will accelerate nuclear restarts and diversify LNG contracts away from the Middle East; India will likely pursue a mix of supply diversification, renewables, and—most critically—increased coal output as its cheapest near-term fix; and Germany will pursue aggressive green expansion and small modular reactor investment while avoiding new conventional nuclear builds. Even partial implementation of such responses carries a shared consequence: a permanent reduction of the Middle East’s role in global energy supply, mirroring the diminished role Russia has played since 2022.

In Other Words

“If the war were to be extended, it wouldn’t really disrupt the U.S. economy very much at all. It would hurt consumers, and we’d have to think about what we’d have to do about that, but that’s really the last of our concerns right now,” National Economic Council Director Hassett underscoring the extent to which domestic concerns—especially cost-of-living issues brought on by high gas prices—are not driving administration policy on the Middle East.

“Joe Kent is a crazed egomaniac who was often at the center of national security leaks, while rarely (never?) producing any actual work,” White House adviser Taylor Budowich on National Counterterrorism Center Director Kent’s resignation.

Did You Know

If confirmed, Sen. Markwayne Mullin (R-OK) will join others in President Trump’s cabinet who share his Capitol Hill background, including Secretary of State Rubio (Senate), Transportation Secretary Duffy (House), VA Secretary Collins (House), Labor Secretary Chavez-DeRemer (House), SBA Administrator Loeffler (Senate), Director of National Intelligence Gabbard (House), EPA Administrator Zeldin (House), and UN Ambassador Waltz (House).

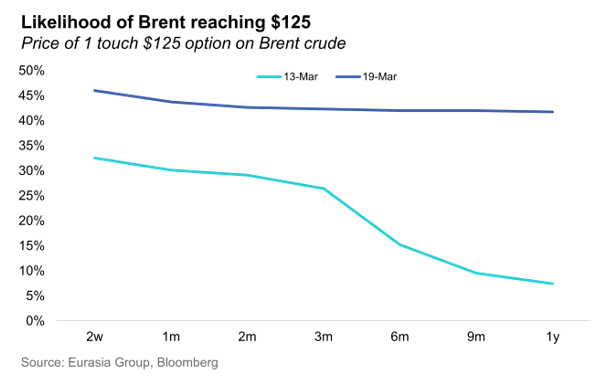

Graph of the Week

Oil Futures are Priced for a More Prolonged Disruption. Oil options are pricing in longer-lasting risks of high prices. During the early stages of the Iran conflict, oil markets priced in short-term disruption that would quickly fade. The recent change in pricing appears to reflect a significant reassessment of the duration of disruption to energy markets.