Thought of the Week:

Among others, September is National Coupon, National Preparedness, and National Library Card Sign-Up Month; yesterday, was National Cheeseburger Day; and today, September 19th, my wife’s birthday, is National Love Your Lunch, National Butterscotch Pudding, and National Talk Like a Pirate Day. This week, we also observed Constitution Day, which recognizes the ratification of the United States Constitution and those who have become American citizens. Constitution Day is normally observed on September 17, the day in 1787 that delegates to the Constitutional Convention signed the document in Philadelphia. Although I’m not sure I know anyone who actually celebrates Constitution Day, recognition of the Constitution’s and Declaration of Independence’s centrality to the fabric of our nation may be needed today more than ever before. In fact, it seems that both Democrats and Republicans need remedial lessons in basic American principles. An increasingly secular Democratic Party has trouble understanding the basis of American freedom—God-given rights to life, liberty, and happiness. In fact, it was just earlier this month that a Democratic senator who represents Thomas Jefferson’s home state called the notion that rights come from one’s Creator, and not from laws and government, “troubling.” As a reminder, the second paragraph of the Declaration states, “We hold these truths to be self-evident, that all men are created equal, that they are endowed by their Creator with certain unalienable Rights, that among these are Life, Liberty and the pursuit of Happiness.” At the same time, a nationalist-populist GOP toys with a confined definition of nationhood that largely ignores many of the universal ideals that inspired the Founders. According to the American Enterprise Institute, the result is a politics unmoored from the philosophy of freedom and equality that gave birth to the Declaration and the Constitution and remains the source of American greatness. The political parties are not alone in their indifference to the Constitution. A recent CATO Institute survey found that although 85% of Americans have a favorable opinion of the U.S.’s founding document, just 56% said it is extremely important for protecting individual rights. While the favorability of the Constitution varies considerably across demographic groups (women, the young, diverse, and liberal have the most skeptical views of the Constitution), a majority (55%) of Americans under 30 would support writing a new Constitution “to reflect our diversity as a people,” and just 38% of Gen Z sees the Constitution as extremely important for protecting individual liberties; in contrast, figures for those over 55 are 25% and 73% respectively. When asked what form of government was created by the Constitutional Convention, Ben Franklin famously responded, “A republic, if you can keep it.” The quote, uttered on September 17, 1787, serves as a cautionary reminder of the fragility of the American republic and the ongoing responsibility of citizens to maintain it through their active participation and vigilance. We can only hope that next year’s 250th anniversary of the Declaration of Independence sparks a new found spirit in holding the Constitution’s ideals dear. In the meantime, tomorrow before her birthday dinner, I’m going to say to my wife, “Avast, matey. To avoid Davey Jones’ locker, and collect yer booty, best ye avoid that plank.”

Thought Leadership from our Consultants, Think Tanks, and Trade Associations

CSIS Looks for President Trump’s Plan B. While President Trump’s pending tariff litigation is at the Supreme Court, the administration is working on developing a Plan B in the event the justices decide against the president. To date, most of the analysis of possible alternatives to maintain the tariffs has focused on other statutory provisions that give the president authority to impose tariffs, including Section 122 of the Trade Act of 1974, which permits the president, in the case of a balance of payments crisis, to impose limited tariffs; Section 201 of the Trade Act of 1974, a “safeguard” provision designed to permit relief for industries seriously injured by an increase in imports; Section 232 of the Trade Expansion Act of 1962, the well-known national security threat provision that the White House is already using on steel, aluminum, autos, and copper; Section 301 of the Trade Act of 1974, which permits the president to take action to obtain the removal of any act, policy, or practice of a foreign government that is unjustified, unreasonable, or discriminatory, and that burdens or restricts U.S. commerce (Trump used this provision to impose tariffs on China in his first term); and Section 338 of the Tariff Act of 1930, a provision that permits the president to impose tariffs up to 50% on any country that discriminates against U.S. products, the drawbacks of which are hard to predict since the provision has never been used. Originally, President Trump selected IEEPA as his tariff tool because it had the fewest procedural limitations and the vaguest threshold for action. All others were less desirable because the rationale for action is too specific, or the procedural requirements stretch out the process and prevent quick action. Although Section 232 is the least constrained and one with which the administration has plenty of experience, using it to replace IEEPA-based tariffs would require such a broad definition of national security that credibility problems might emerge in the courts. In the end, President Trump might choose a non-legislative approach. For instance, he could argue that the tariffs covered by the agreements that have been reached are imposed pursuant to those agreements rather than IEEPA and thus are not affected by any court decision. In fact, the agreement tariffs, plus the Section 232 tariffs, which are not covered by the litigation, constitute a substantial chunk of U.S. trade, so the White House could salvage much of its trade program. Tariffs are not going away easily.

Eurasia Group Sees the U.S.-Japan MOU as a Template for Future Investment Deals. The $550 billion in investment commitments outlined in the U.S.-Japan trade deal will be directed by the U.S. through a newly created Investment Accelerator and funded by Japan, a model that will likely be repeated in other trade deals. Under the terms of the deal, the U.S. will review various investment proposals through a newly formed Investment Committee, with President Trump having final sign-off on any proposal that moves forward. Once a proposal has been made, Japan will have 45 days to approve funding. Rejecting a proposal risks tariff hikes per the terms of the deal. The administration will likely target industries relevant to national security, including semiconductors, pharmaceuticals, metals, critical minerals, shipbuilding, energy (particularly LNG and nuclear), and AI. The Investment Committee’s likely focus on AI is underscored by the White House’s transfer of responsibility for the CHIPS Program to the Investment Accelerator. The nearly boundless discretion afforded to the Investment Committee and the president himself in selecting projects suggests that personal connections to President Trump’s inner circle and highly effective lobbying will play a key role in determining which initiatives get funded. The industries outlined in the trade deal are also likely to see the U.S. government taking a direct equity stake in certain companies; however, this subset of firms will likely be vastly smaller than those targeted for foreign direct investment. The White House’s decision to take direct equity stakes in Intel and the Mountain Pass mine, as well as its “Golden Share” in US Steel, suggests that such firms are likely to be characterized by a combination of continued financial troubles, concerns about linkages to the CCP, and importance to key constituent groups in swing states.

Eurasia Group Says Net Immigration Estimates Point to Stagflationary Impact. The Congressional Budget Office (CBO) has updated its forecast of net immigration for 2025 to roughly 400,000, down from a 2 million projection earlier this year, underscoring that the U.S. has reached the end of the Biden-era immigration boom. Estimates of net migration vary due to differences in expectations for deportations. While the CBO projected 140,000 interior deportations in its estimate, others, including the Eurasia Group, expect total removals will land around 400,000. The CBO estimate should not be taken as definitive as other public- and private-sector estimates range from -500,000 to 1 million net immigrants this year. Over time, this may constrain labor-force growth and have a stagflationary impact on the American economy. This will materially affect the construction sector, which has long relied on a large immigrant workforce. Although the Trump administration—especially Commerce Secretary Lutnick—has touted 2026 as a banner year for construction jobs, achieving this will require that the administration backtrack on some deportation promises, provide targeted exemptions for the construction industry, or that large numbers of native-born workers switch into the industry. Elsewhere, the CBO report’s long-term picture for U.S. population growth has turned more negative; due to a drop in fertility, deaths are now projected to outpace births by 2031, two years earlier than previously anticipated. That will mean that net immigration will be the only source of population growth beginning in the early 2030s.

Observatory Group Offers Their September FOMC Meeting Postview. The Federal Reserve cut its policy rate by 25 bp and signaled via the median policy projections a further 50 bp in cuts by the end of the year. Chair Powell justified the move on the basis of a rise in downside risks to the labor market. Although the anticipated dots show a clear move in the dovish direction, analysts think it is foolish to infer too much based on the median dot, when all it takes is one policymaker changing their mind to shift it. The FOMC does not see their most recent action as the start of an aggressive rate cut cycle, but as a resumption of a gradual normalization that will not even be complete at the end of three years. In fact, the median inflation projections and the median policy projections together support the conclusion that the real policy rate will in fact rise between now and the end of 2028. Rather than see this as anything resembling a consensus, the most recent action should be viewed as a product of uncertainty coupled with the problematic nature of median projections. It is hard to predict what the Fed’s dynamics will be in a post-Powell world, but the prevailing view is for constructive cooperation and the conventional review of data, rather than constant tension and disputes.

“Inside Baseball”

Government Funding Update. Punchbowl News reports that the battle over government funding has turned into this: each side claims they’re being completely reasonable while blaming their opponents for the looming showdown. Yet, with less than two weeks to go before the funding deadline, Republican and Democratic leaders are growing further apart rather than closer. Both sides seem content to stand pat, even if that leads to a government shutdown on 10/1 and a broader political crisis. While other analysts disagree and see a shutdown as unlikely, with President Trump in the White House and Republicans in charge of Congress a shutdown could spiral into a prolonged political stalemate. Democrats are dug in on health care demands, and they won’t move unless Republicans negotiate. At the same time, the Republican leadership has told its rank-and-file that they won’t negotiate on a seven-week CR. Any deal will be that much harder to reach if a shutdown does take hold. While House and Senate Democrats introduced a month-long funding proposal that would keep the federal government open until 10/31, the Republican plan extends funding until 11/21. Democrats are calling for the permanent extension of enhanced Obamacare premium tax credits, in addition to the reversal of Medicaid cuts from the One Big Beautiful Bill. Democrats also want to bar any future rescissions and restore public-broadcasting funding. While the price tag for these provisions is hundreds of billions of dollars, a massive amount on a short-term stopgap funding bill, nearly every provision in the package is a non-starter for Republicans. In fact, Republicans have no interest in negotiating. They feel as Democrats felt in the past: negotiating validates the Democrats’ position. Republicans are comfortable saying that they’ve proposed a clean CR, which is what Democrats usually ask for, to buy time for bipartisan full-year FY2026 funding talks. While Senate Democrats vow to oppose the House bill, all indications are that they will be able to filibuster any GOP CR. Still, some Democratic senators are leaving the door slightly open to back the seven-week stopgap, especially if it’s the only hope for averting a shutdown. Although the equivocations seem to reflect a desire to avert a shutdown at all costs, don’t expect any Democrats to back the CR but Sen. Fetterman (D-PA).

In Other Words

“You continue to lie from your perch and put on a show so you can go raise money for your charade. You are a political buffoon at best,” FBI Director Patel to Sen. Schiff (D-CA) during a hearing.

Did You Know

The only two presidents to be members of Congress after their presidency were President John Quincy Adams, who was elected to the House, and President Andrew Johnson, who was elected to the Senate.

Graphs of the Week

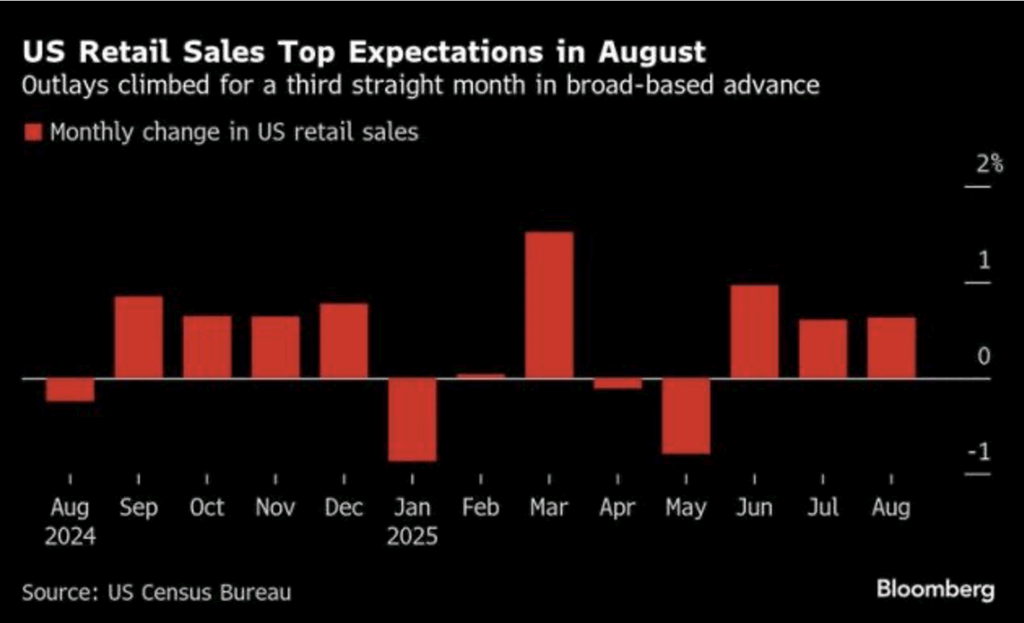

Retail sales rose in August for a third straight month, beating all estimates in a Bloomberg survey of economists. Nine out of 13 categories posted increases, led by online retailers, clothing stores, and sporting goods—likely reflecting back-to-school shopping and suggesting consumers remain resilient amid tariff-driven price increases. It is now estimated that the bulk of the tariff impact will begin to affect growth starting in Q4 and lingering into H1 2026.