pictured above: Winslow (far left) Lobbying U.S. Congressional Representative Beth Van Duyne (R-TX) (center)

Thought of the Week:

This week, D.C. felt like D.C. Not the D.C. of the last five years, but the D.C. BC (before Covid). My metro rides to and from work were crowded; there was a line at Subway for my Wednesday guilty pleasure—the Meatball Marinara “Meal of the Day;” and downtown happy hours on outdoor patios spilled into the sidewalks. Congress, both the House and Senate, were back in session; Republicans defeated Democrats 13-2 to extend their winning streak to five in the annual Congressional baseball game; and the President and First Lady attended opening night of “Les Misérables” at the Kennedy Center. Tourists flooded the National Mall; the SecDef, Treasury Secretary, and three Democratic governors all testified before Congress; and preparations were being made all over the city for this weekend’s celebration of the Army’s 250th birthday, to include only the second military parade Washington has seen since the end of World War II. Today, in a phone call, Japanese Prime Minister Ishiba is expected to discuss tariffs with President Trump ahead of next week’s G-7 meeting in Canada. The energy pulsing through D.C. also extended to the Washington office. On Thursday alone, we met with Congresswoman Van Duyne (R-TX) and four other Congressional offices, including those of Sen. Johnson (R-WI), Rep. Moran (R-TX), and Senate Majority Leader Thune (R-SD). The primary purpose of the meetings was to discuss the chilling effect Section 899 of the reconciliation bill (the One Big Beautiful Bill or OB3) could have on foreign direct investment in the U.S. SCOA’s footprint across the country, IRA credit rollbacks, and U.S. trade and tariff policy were other major topics of discussion with staffers. At present, the reconciliation bill has passed the House of Representatives and is currently being considered in the Senate. Based on the time it took to get through security and the number of corporate advocates I saw tracing the halls of Congress, the bill is being lobbied heavily from all sides. The messages we took back from our meetings were:

- The House passed the bill, warts and all, knowing that the Senate would amend certain provisions.

- Certain sections, like Section 899, in the House-passed bill were meant to send a message; and they are having the intended effect.

- A House-Senate conference on the bill could take a month, tentatively moving passage from July 4 to August 1.

- SALT and Section 899 are the two most contentious issues in getting the bill passed.

- Because the bill needs to pass, 218 and 50 are the only numbers that matter in the end.

- While members recognize Section 899’s downside, they welcome hearing true solutions.

To receive the full readout from our Hill meetings, get an update on the reconciliation bill’s status, and/or discuss any legislative or public policy issue your office faces, do not hesitate to contact the Washington office.

Thought Leadership from our Consultants, Think Tanks, and Trade Associations

Eurasia Group Believes the New Geopolitics of Sourcing Will Create Risk at Every Stage of the Supply Chain. President Trump’s tariffs are accelerating a major restructuring of global supply chains. Protectionism and a fracturing international system are threatening both supply chain security and market stability. The consumer and retail sector faces a sourcing environment with rising international tensions, trade policy uncertainty, legal and customs compliance challenges, and divergent regulatory frameworks that will require a new approach to understanding geopolitical risk. Traditional considerations such as labor standards and infrastructure quality now exist alongside a host of political factors that will determine success, ranging from a company’s national origin to the physical security and viability of shipping lanes. Strategies such as developing region-specific or duplicate supply chains, maintaining enhanced financial capacity, and engaging policymakers in both sourcing and import markets will prove vital as companies navigate heightened unpredictability, declining consumer sentiment, and reputational risks tied to political polarization politics.

Eurasia Group Says Environmental Rules Rollback, if it Survives Legal Challenge, Will Boost Gas. The Environmental Protection Agency (EPA) has proposed scrapping limits on power plant emissions of CO₂, mercury, and other pollutants imposed under President Biden. If implemented, the proposal ordered by President Trump would scrap Biden-era emissions rules for power plants that had aimed to cut more than 1 billion tons of CO₂ emissions by 2047. It would also undo regulations on mercury and air toxics. The move is quintessential Trump deregulation and bullish for U.S. gas. It aligns with expectations for significant environmental deregulation, and natural gas would seem to be the biggest winner, especially for its use as a baseload fuel. Renewables should be OK. Despite the retreat on climate policy, renewables often outcompete fossil fuels on cost in many regions, even excluding Inflation Reduction Act (IRA) tax credits that now face an early sunset. Legal challenges will be a significant obstacle to the rules ultimately taking effect. The proposed rule’s justification—that power sector CO₂ is too minor to regulate—is on shaky legal ground and could conflict with precedent. In addition, internationally, the repeal increases the risk of retaliatory climate policy measures against the U.S., especially by the EU.

Inside U.S. Trade Reports U.S. Partners Look to G7 Summit to Make Case Against Steel, Auto Tariffs. Having submitted their final offers, countries continue to implore the U.S. to exempt them from new tariffs, set to take effect next month, with several leaders looking to use the sidelines of next week’s G7 summit to make their case directly to President Trump. The president will travel to Canada on Sunday for the G7 meeting, and the Office of the U.S. Trade Representative (USTR) confirmed it had given trading partners until June 4 to submit final negotiating offers to avoid trade deficit-based tariffs. While the administration had delayed the imposition of those tariffs from April until July 9, giving countries the chance to strike deals with the U.S., it also imposed 25% tariffs on autos and auto parts and doubled tariffs on steel and aluminum from 25% to 50%. Those new tariffs have become part of bilateral trade negotiations. The UK managed to secure a tariff-rate quota for autos, and Japan is also looking for a break on the auto tariffs. Last week, Japan offered a deal that would keep in place the U.S. tariffs, but lower them based on several factors, including how much a country contributes to the U.S. auto industry. Australia is trying to dodge the steel and aluminum tariffs by offering access to its critical minerals market. Although trade policy is not explicitly mentioned as a priority item for the G7, the issue is likely to be raised as part of the discussion. Still, the meeting will give leaders a chance to discuss bilateral trade issues on the sidelines. With less than a month to go, the only deal the administration has announced is a framework agreement with the UK. The details of that agreement are still under negotiation.

Observatory Group Says Federal Reserve Concerns about Inflation Expectations Reinforce Cautionary Policy Outlook. Federal Reserve policymakers are increasingly concerned that inflation expectations may not be well-anchored. The central bank is starting to suspect that even when longer-term inflation expectations are stable and near target, they may not indicate that consumers’ and businesses’ expectations are aligned. Many analysts now think it is important to look at inflation expectations at every horizon. If true, this means that the Fed may not have the luxury of ‘looking through’ price level increases from tariffs, even if policymakers are confident they will not persist. All things equal, these considerations make the FOMC less willing to cut rates in the face of modest weakness in the employment data. The latest prediction is that the Fed will hold rates unchanged and again signal great uncertainty about the economic and policy outlooks. Chair Powell will explain that the scope for substantive tariff impacts has expanded since the May meeting, but confidence in understanding the balance of those effects between inflation and activity has not. The slightly tight policy stance remains a critical element in maintaining a consensus for rate cuts sometime later this year, and the expectation is for one or two cuts in 2025. Expect the overall message from next week’s meeting to be a lack of confidence in any outlook without more hard information on the tariff economy, which may be weeks, if not months, away.

“Inside Baseball”

Institute of International Finance (IIF) Offers Their Global Macro View—A Slower World, A Sharper Lens. Global growth is now expected to slow to 2.7% in 2025 from 3.1% in 2024 amid structural policy shifts and fragmented recovery. U.S. growth is projected to decelerate sharply, with fiscal expansion and tariff uncertainty shaping sentiments. The Euro and Japan areas face muted growth constrained by divergent fiscal and monetary adjustments. China’s growth remains moderate and heavily reliant on policy support, being limited by global spillovers. Emerging market growth is resilient overall, but future capital allocation will be increasingly selective and policy sensitive.

In Other Words

“I think there is growing momentum to get rid of [Section 899] in the Senate. Senators recognize that it’s counter-productive to the economic vision for the administration, which has made a big point about trying to get more investment to the U.S.,” Jonathan Samford, president of the Global Business Alliance (GBA), quoted in The Financial Times on investors’ lobbying push to strike Section 899 from the House-passed reconciliation bill (SCOA is a member of the GBA).

“I’m not going to give you legal analysis on whether Gavin Newsom should be arrested. But he ought to be tarred and feathered, I’ll say that,” Speaker Johnson.

Did You Know

Pickleball was invented by Rep. Joel Pritchard (R-WA) and two friends in 1965.

Graphs of the Week

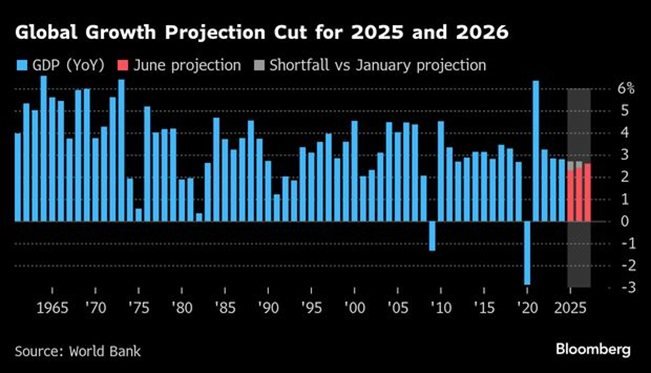

The World Bank Warns that the 2020s Face the Weakest Global Growth Scenario Since the 1960s. The World Bank has cut its forecast for global growth this year and warned that the 2020s are on track for the weakest performance of any decade since the first Apollo moon landing because of trade tensions and policy uncertainty. The Bank has lowered its 2025 outlook to 2.3%, from 2.7%, which would be the weakest in 17 years, outside of the recessions in 2009 and 2020 created by the shocks of the global financial crisis and Covid-19 pandemic. It also warned—based on current forecasts—that global growth in the first seven years of this decade is on course to average 2.5%, the slowest for any decade since the 1960s.