Thought of the Week:

When facing a novel issue, entering a new environment, or trying to understand a complex concept one may go through a process of metacognitive situational awareness. Metacognition is the ability to realize how one is perceiving and understanding the environment around them, and it involves being consciously aware of one’s own thoughts and mental processes. At any one time, it tells us that we may live in one or more of four boxes: (1) I don’t know what I don’t know; (2) I don’t know what I know; (3) I know what I don’t know; or (4) I know what I know. When initially stepping into a new situation, a person typically resides into Box 1. The second box relates to situation in which one might have an underlying understanding of a topic, but isn’t aware that they know it. Box 3 is a positive steppingstone to learning as it entails being able to articulate what one doesn’t know and gives an individual the ability to ask questions and seek help. Box 4 is where we ultimately want to live as it demonstrates a certain mastery of the issue at hand and provides confidence in one’s ability to address it. In the whirlwind that is the second Trump administration and 119th Congress, each day seemingly brings Washington corporate offices a new exercise in metacognitive situation awareness.

In an effort to move through the process and toward Box 4, earlier this week, members of the Washington office attended the Global Business Alliance’s (GBA) Government Affairs Leaders’ Summit. As you know, the GBA, which SCOA is a member, is the only trade association that exclusively represents the interests of foreign subsidiaries operating in the U.S. The Summit included government affairs professionals and lobbyists from more than thirty major companies, including BAE, Hyundai, LVMH, Michelin, Nomura, Panasonic, and Siemens; and the topics covered spanned reconciliation, China, tax and trade, CFIUS, regulatory risk, congressional investigations, and more. The Washington office’s dual role—Intelligence and Government Affairs—is designed improve SBUs situational awareness with regard to U.S. government policy. Offered below are several pertinent takeaways from the summit that may serve your metacognition:

- The conventional wisdom is wrong—apart from a few high-profile issues like abortion, the GOP is not becoming more conservative but is moving left on a range of issues.

- GOP populism has a distinct leftward slant when considering such issues as labor, deficits, and entitlements.

- The links between the GOP and business are growing more tenuous.

- Business is particularly suspect with GOP leaders like Vice President Vance and Sen. Hawley (R-MO).

- Republicans are not running away from business, but are just not as close as they once were.

- Due to partisanship and small legislative margins, there will be few ways to reduce government spending.

- Because bill passage outside of reconciliation will require Democratic votes, 2025 will be a tough year for Speaker Johnson, and he may not last the full Congress.

- Passage of a reconciliation bill is not a sure thing; although one will probably pass, it may require Democratic votes.

- The draft timeline for reconciliation is a budget resolution (February); committees (March); President Trump (April); this is extremely aggressive.

- Companies should not expect reconciliation on that timeline but more likely by December or even January.

Thought Leadership from our Consultants, Think Tanks, and Trade Associations

Capital Alpha Says Trump Executive Order Puts IRA Grants, Loans, and Loan Guarantees at Risk. President Trump’s executive order on “Unleashing American Energy” puts grants, loans, and loan guarantees based on appropriated funding from the Inflation Reduction Act (IRA) and the Infrastructure Investment and Jobs Act (IIJA) at risk. The order directs federal government agencies to suspend disbursement of all funds related to the IRA and IIJA. The funds will be held back pending a review by the Office of Management and Budget (OMB), which could decide to cancel or withhold the funds permanently. The government assumes a legal responsibility to disburse obligated funding, but the disbursement is subject to terms and conditions. The Trump administration will deny funding unilaterally where it can, go to Congress with rescission requests, and go to court where necessary. IRA tax credits, direct pay, and transferability of tax credits are not affected by the executive order.

Eurasia Group Sees President Trump Moving Fast and Breaking Things. The Trump administration announced a “deferred resignation” program for all federal workers, only hours after a judge blocked its attempt to pause a wide tranche of federal spending. The buyout offer is an unexpected and radical move that underscores the administration’s intent to dramatically reshape the federal workforce and achieve cost savings in doing so. The administration estimates that between 5% and 10% of workers will take the buyout. The buyout offer is structured such that it will likely pass legal muster and likely does not need authorization from Congress, as it appears to make use of funds that are expected to be appropriated as part of the March funding bill. It is also the strongest signal yet that Elon Musk is playing a major role in the administration’s workforce policy. The ramifications of the buyout offer remain unclear. While an across-the-board 5% reduction in headcount would be survivable for federal agencies, a mass departure of staff in key functions, many of whom have private-sector opportunities, would likely worsen regulatory bottlenecks. With the buyout offer and the spending freeze—the latter of which caused considerable uncertainty about the status of key programs like Medicaid and will have its day in court next week—the Trump administration is moving quickly on key domestic policy priorities and is using innovative methods to do so. Not all of these moves will stick. Many face either issues in the courts or blowback from congressional Republicans. But their rapid and chaotic rollouts will create an increasingly uncertain policy environment for U.S. businesses to navigate, as the status of bedrock institutions and programs is thrown into day-to-day flux.

Observatory Group’s Update on Trump’ Tariff Decision-Making. President Trump has made scores of statements about tariffs since Day One, many of them confusing. His clear immediate focus though is on fentanyl and border crossing. His threats against Mexico and Canada are real, and analysts fully expect him to follow through and impose tariffs on Mexico and Canada on February 1; however, the collection of the duties will likely be suspended to allow for last-ditch negotiations. While Trump will up the ante, both countries have been rushing to meet his demands—Canadian ministers have been in Washington almost all week and additional meetings are planned. This approach serves Trump well because he placates two rival Republican camps. He satisfies growth advocates (and inflation hawks) by delaying collection of tariffs. He pleases the nationalists by quickly meeting their demands on fentanyl and illegal immigration—with Mexico and Canada paying for it. The growth camp has also won out on initial policy towards China; companies should expect limited action until a Xi-Trump summit in late March or early April. A 10% tariff on China related to fentanyl, again applied but suspended, is still a possibility, but not the base case. There seems to be goodwill on both sides going into the summit, although agreement could be derailed easily, given all the security risks stemming from the two country’s superpower rivalry and the China hawks in the nationalist camp. A global tariff on products linked to national security, e.g., defense, energy, and medical supplies, could be proposed within the first 100 days, but is more likely delayed past the China summit. Treasury Secretary Bessent has suggested a tariff on all imports or on all national security related products starting at a 2.5% rate, going up to 10-20%, but President Trump said he wants to start off higher. This debate will continue, but final decisions are not expected to be made until a later date.

“Inside Baseball”

Crash Could Spark Lobbying on DC Flights. Lawmakers could reprise of one of the biggest and costliest lobbying fights of the last Congress after a crash at Capitol Hill’s closest airport. Airlines and lobbyists are sticking to scripted messaging after the mid-air collision of an American Airlines flight and an Army Black Hawk helicopter that killed 67 people. The crash renewed debate about overcrowding at the airport that lawmakers rely on the most—DCA is just a 15-minute sprint by car from Capitol Hill. Some lobbyists anticipate lawmakers will consider changes, although proposals will likely depend on the outcome of the investigation. Congress could revisit a change included in last year’s FAA reauthorization that added a handful of new flights at Ronald Reagan Washington National Airport; those new routes haven’t actually taken flight yet. The lobbying fight fueled millions of dollars in lobbying and advocacy efforts, and pit United Airlines—which opposed the new flights—against Delta Air Lines, which supported additions. Delta was part of the Capital Access Alliance, advocating for more direct flights to and from Reagan National. American Airlines opposed the expansion. In addition, lawmakers’ personal interest in safety at the airport could prompt new restrictions on low-flying helicopters.

In Other Words

“A Fork in the Road,” the subject line of an email to all federal employees offering a plan of voluntary resignation.

“I think we have to pick our fights and not chase after every crazy squirrel,” Sen. Schiff (D-CA) on how Democrats should respond to President Trump.

Did You Know

The presidential use of executive orders (EOs) has dwindled since the Clinton administration*. While President Clinton issued 364 EOs during his eight years in office, President Trump issued just 220 during his first term. A run down of the total number of EOs signed by recent presidents is as follows: Clinton (364); Bush (291); Obama (277); Trump 45 (220); Biden (162); and Trump 47 (37).

*These figures include only executive orders and do not include other forms of executive action such as proclamations, memorandums, and/or discretionary executive actions.

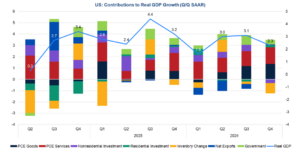

Graph of the Week

Annualized real GDP growth of 2.3% quarter-over-quarter masked a stronger underlying pace of growth in the economy at the end of 2024. In fact, the economy ending 2024 on a healthy note with GDP growing 2.5% year-over-year. This provides solid ground for the Federal Reserve to remain patient with respect to further normalization of policy rates in H1 2025. Companies should expect the central bank to stay on hold throughout H1 2025 and resume cuts in the latter half of this year as growth slows closer to potential and inflation returns to its downward trajectory. Robust consumer performance at the end of 2024 may pull some strength forward at the expense of future quarters as consumers appear to be stockpiling on computers, information processing equipment, and light trucks ahead of tariffs.