Thought of the Week:

Last week, I was able to escape the swamp-like conditions of Washington, D.C., and trade them for the near perdition-like temperatures of Murfreesboro, Tennessee. There, I visited our Steel Summit subsidiary and made my way to Nashville for The Conference Board’s quarterly Government Relations Executive Council meeting. Hosted by Warner Music, the Council addressed such topics as the role of AI in policymaking, the relationship between state agencies and the federal government, and using social media campaigns to influence policy and politics. My retreat out of the nation’s capital roughly coincided with the start of the House’s August recess (the Senate is scheduled to go on recess today). August recess is a tradition on Capitol Hill, and it comes on top of periodic breaks that typically overlap holidays like Christmas, the Fourth of July, and Easter. In fact, the specifics of the congressional calendar, including recesses, are structured by the Constitution, existing law, and the choices made by the individual chambers. While the 20th Amendment established January 3rd as the start date of a new Congress, and Article I, Section 5 established the rule that the House and Senate must agree to adjourn if a break is to last more than three days, the August recess was formalized in the Legislative Reorganization Act of 1970. Interestingly, the Senate is technically in session for much of its summer break, scheduling “pro forma” sessions, which last no longer than a few seconds and include no more than a handful of members. These meetings are designed to check the power of the presidency, preventing temporary appointments and “pocket vetoes” of legislation that can occur if the Senate is in recess. Over the last decade, both chambers have averaged about 150 days in session per year. The reason for so much free time has to do with tradition—D.C. is uncomfortable in the summer, air conditioning wasn’t installed in the Capitol until 1929 (after several senators dropped dead during sweltering sessions), and the fact that it once took west coast legislators weeks to travel cross country. Regardless of advances in technology and transportation, extended breaks from Capitol Hill are considered essential for senators and representatives to maintain contact with their constituents. In fact, the House refers to its August recess as a “district work period,” while the Senate refers to theirs as a “state work period.” Whether Democrat or Republican, meetings with first responders, tours of local businesses, and/or eating hotdogs at county fairs are not merely performative. Rather, they enable members to engage in the most essential part of the representative process—hearing from constituents about what matters to them. While in Nashville, I was able to meet with state Representative Johnny Garrett, who has already declared his candidacy for Congress. He told me that Nashville isn’t real. Sure, he said it’s real in the sense of development, economic growth, and a widening of the tax base, but not real in the sense of meeting voters. According to Rep. Garrett, the only way to meet a real Tennessean, whether they vote or not, is to go to county fairs, farms, little league baseball games, and neighborhood porches. I knew what he meant. For me, D.C. isn’t always real, but Murfreesboro was; so was my visit to Interacid in Tampa earlier this year; and so will the Credit Manager’s meeting in Phoenix this October.

Thought Leadership from our Consultants, Think Tanks, and Trade Associations

Capital Alpha Asks What if the Courts Strike Down Trump’s IEEPA Tariffs? The Federal Circuit Court of Appeals held oral arguments on this very question yesterday. Because the courts, to date, have treated this question as an urgent issue, it’s possible that we get a ruling from the Federal Circuit by September; in fact, a ruling later this month may not be out of the question. Consider that the Court of International Trade took only two weeks to hand down its decision, and the federal district court handed down a preliminary injunction against the president in just two days. So, what would it mean if a third federal court rules that the tariffs are unlawful? Assuming that happens, the Supreme Court would be next in line. Taking a step back, while President Trump has built a global trade architecture based on IEEPA tariffs, two federal courts have already ruled that the tariffs’ use is unlawful. And although the White House has told trading partners that the latest stay is a sign that the court will ultimately rule in its favor, legal analysts aren’t so sure. Consider that as of today, the U.S. government is collecting upwards of $25 billion per month in tariff revenues, meaning that more than $100 billion would need to be refunded if the court rules against the president. If that were to happen, it is expected that President Trump would appeal to the Supreme Court and demand a stay of the Federal Circuit’s ruling to keep the IEEPA tariffs in place. It’s unclear whether the Supreme Court would grant a stay, as one would make no sense unless the Supreme Court anticipates that it plans to reverse the Federal Circuit. If the White House loses in court, expect a powerful reaction of some kind. The bottom line is that President Trump does not have a Plan B, and the timing of a court decision—in September, October, or November—could impact any number of international meetings, including an anticipated Trump-Xi summit this fall. White House officials claim that if the courts strike down IEEPA tariffs, the president can simply replicate them using authorities such as Sections 122, 232, 301, and 338. However, these provisions do not provide the same authority that Trump claimed under IEEPA, and the regime Trump could construct under Sections 232 and 301 would look vastly different than the tariff regime he has constructed under IEEPA. What’s more, after a loss on IEEPA, Trump would likely face a coalition of litigants eager to check his power to make unprecedented use of traditional tariff authorities. Although President Trump will retain the ability to build a protectionist wall around the U.S. if he wishes, a loss means he won’t have the free hand he hoped to have under IEEPA.

Eurasia Group Says Markets Still Exposed to Stagflationary U.S. Policy Mix. While President Trump’s trade rhetoric has created uncertainty for investors, the equity markets’ response to escalating tariffs has been relatively muted thus far. While this may reflect either an assumption that Trump will ultimately back down or that the current policy mix will achieve a “goldilocks” scenario of continued growth, modest inflation, and falling interest rates, a clear risk of disappointment exists. Although near-term growth risks have receded, tariffs will damage growth in the longer term. Come the end of the year, the Trump administration will have signed a number of relatively thin trade deals that will keep the average effective tariff rate somewhere between 13-17%, up from 10-15% previously. This is much higher than historical standards, but lower than the rates Trump announced in early April. Even factoring in a reduced risk of rapid decoupling from China, this level of tariffs does not represent a benign outcome. While the risk of a near-term disruption to trade flows and GDP may be lower than a few months ago, the longer-term damage is likely to be substantial. What’s more, the One Big Beautiful Bill is anything but, as it substantially worsens the outlook for U.S. public finances, with no prospect of consolidation or creation of fiscal capacity for a rainy day. Tax cuts and spending increases in the bill are front-loaded, while controversial, and deeply redistributive, spending cuts are delayed. This approach is likely to have a limited growth impact, while at the same time incurring high political costs. The net result: continued upward pressure on both nominal and real interest rates. This policy mix can be described as stagflationary. The combination of tariff, fiscal, and immigration policies is projected to reduce growth by about 1-2 points below trend in both 2025 and 2026, while maintaining the inflationary pressures that slow the pace of Fed easing, even slower than other developed market central banks.

Inside the EPA Reports EPA’s GHG Risk Finding Repeal as an Unprecedented Deregulatory Move. EPA Administrator Zeldin has declared that the agency’s imminent proposal to undo its 2009 greenhouse gas endangerment finding and related vehicle GHG rules “will be the largest deregulatory action in the history of America.” The upcoming declaration criticizes the Obama EPA’s 2009 finding for what are called “mental leaps”—declaring that CO2 when mixed with other GHGs contributes to climate change “how much they don’t say”—and that climate change endangers human health. According to the EPA, the Obama administration “did not actually study carbon dioxide individually, but made assumptions on science that actually turned out not to be true, didn’t go out for public comment, and didn’t weigh the economic impacts of the regulations that would follow” from the endangerment finding. Administrator Zeldin added that the EPA started “regulating the heck” out of just carbon dioxide and ignored the fact that carbon dioxide numbers in the U.S. have gone down. He frames the proposed scuttling of the findings and associated vehicle rules as something that will lower costs for Americans, and as something the public elected President Trump to do.

“Inside Baseball”

Eurasia Group Believes President Trump’s “Not-Bad” Approval Ratings will Prove Surprisingly Durable. A recent Wall Street Journal poll placed President Trump’s approval rating at 46%, strengthened by perceptions of a brightening economic outlook; polling averages have the president’s approval at 44.7%. The most important indicator from the poll is that there is no sign the president is losing ground with the Republican base; he maintains 88% approval inside that group. The lack of any movement among the GOP base, despite tariff-related turmoil, suggests that concern about base support is not likely to motivate any policy U-turns in the coming weeks. In fact, President Trump’s approval rating has proved surprisingly durable. While the mid-forties is not strong by any means, it is not weak either, and it is higher than President Biden’s was for much of his presidency. Should this situation endure, it will slightly bolster Republican hopes in the midterms.

Any Government Shutdown Could Last Weeks. With Congress way behind schedule in its annual appropriations process, a late September continuing resolution (CR) might seem all but assured. However, several Democratic Senators, including Minority Leader Schumer (D-NY), broke with the party last March to approve a CR and avoid a shutdown, making Democratic buy-in this time unlikely, and making a shutdown the base case. What’s more, a shutdown could last longer than the week or so that has become routine for recent shutdowns. The truth is that the White House may not mind a shutdown, since it would allow Office of Management and Budget Director Vought to essentially pick and choose what parts of the government would remain open. If President Trump does not push Republicans to deal, ending a shutdown would require Democrats to accept a lopsided bargain right about the time midterm campaigning starts. Consider that the House will likely pass, along mostly party lines, an amended CR with additional spending cuts and social policy changes. These changes, needed to gain House Freedom Caucus support, will make the bill even harder to sell to Democratic senators, and the Senate needs at least some bipartisan support to clear its 60-vote threshold.

In Other Words

“Did you get to see my drive on the first hole? Pretty long. Pretty long. That’s no Joe Biden, let me tell you,” President Trump when asked if his trip to Scotland was a promotional trip for his family business.

“Constipated. Leaderless. Confused. A cracked-out clown car. Divided. These are the words I hear my fellow Democrats using to describe our party as of late. The truth is they’re not wrong: the Democratic Party is in shambles…The Democratic Party is steamrolling toward a civilized civil war. It’s necessary to have it. It’s even more necessary to delay it,” longtime Democratic strategist James Carville.

Did You Know

Al Gore is the only Vice President to be born in Washington, D.C. From 1993 to 2001, during Bill Clinton’s presidency, he served as the 45th VP.

According to the National Republican Senatorial Committee (NRSC), Apple’s latest operating system update will introduce new message filtering that marks political fundraising texts as spam by default.

Graphs of the Week

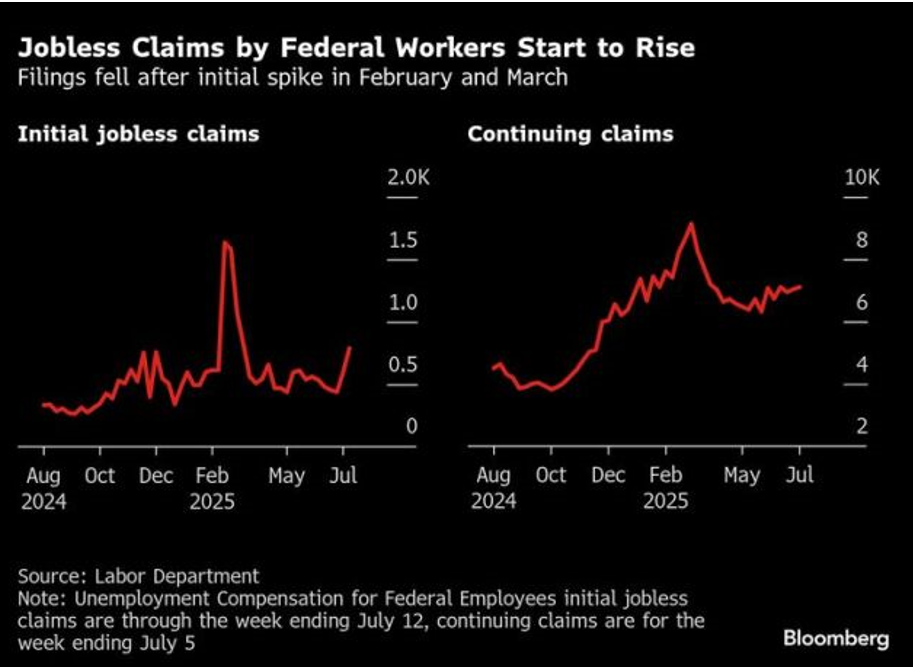

Washington, D.C.-area Federal Workforce Down 22,000. In and around the nation’s capital, the federal workforce has shrunk by nearly 22,000 people—and that number is poised to mount. Maryland experienced the steepest decline, dropping 5.4%, followed by Virginia, according to the Federal Reserve Bank of Richmond. Separate data shows that applications filed by federal workers for unemployment insurance are climbing following the Supreme Court’s ruling that cleared the way for the Trump administration to lay off employees across federal agencies. The “DOGE impact”— referring to the White House’s Department of Government Efficiency—was cited in 286,679 planned layoffs this year, including cuts across the federal workforce and its contractors. An additional 11,751 job cuts were attributed to downstream impacts, such as cutting funding to nonprofits and affiliated organizations.

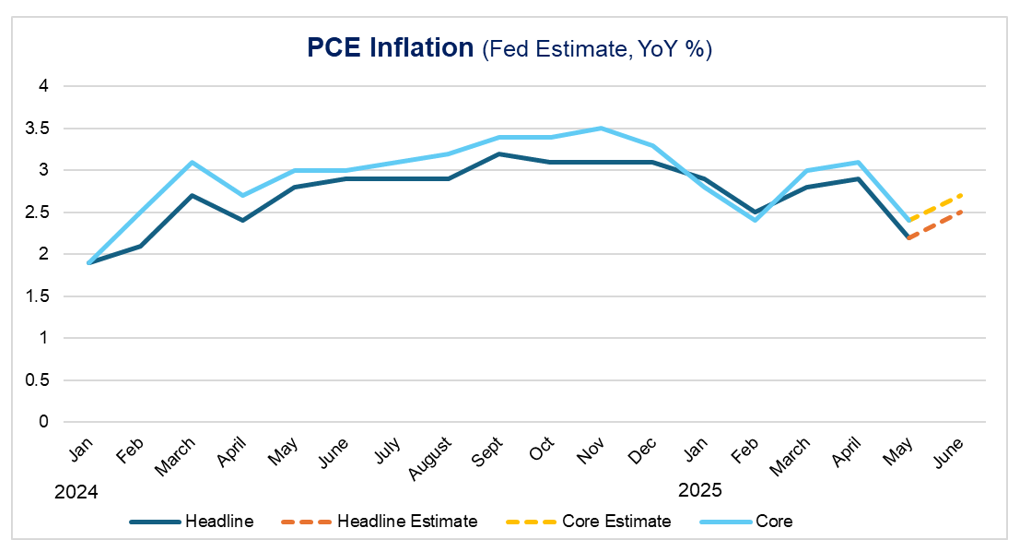

The Conference Board Sees a Hawkish Powell Looking Beyond September. Barring significant deterioration in the labor market, the Federal Reserve will stay on hold at the September FOMC meeting, as inflation is set to rise in the coming months. If the Fed needs to change this message as a result of new data, Chair Powell will have a chance to offer new guidance at the Fed’s August Jackson Hole symposium. The Chair’s assessment that inflation is further away from the central bank’s 2% target relative to where the labor market is with respect to full employment suggests a “modestly restrictive” policy stance going forward. While the Fed’s base case is a one-time rise in prices due to tariffs, increases in inflation are a risk that needs to “be assessed and managed.” In fact, as long as the labor market remains near full employment, the central bank will be able to stay in risk management mode. Ultimate Fed action will depend on which way current risks, as a result of tariff policies, go. While policymakers saw labor market risks and inflation as roughly equal at the June FOMC meeting, Chair Powell’s most recent comments suggest the risk assessment has shifted in the direction of higher inflation. Corroborating this view, PCE price inflation is estimated to rise materially, pushing inflation up to 2.5% (vs. 2.3% prior) in June in y/y terms. While data over the coming months will provide clarity on tariff effects, inflation is not expected to peak until Q4; as such, it is anticipated that the first Fed rate cut will come in December.