Thought of the Week

One of the most surprising statistics from the 2024 presidential election was the surge of support President Trump received from Gen Z voters. Although these voters, born between 1997 and 2012, turned out in fewer numbers across all demographics in 2024 as compared to 2020, their voting preferences shifted considerably to the right. According to Harvard University’s Ash Center for Democratic Governance and Innovation, Gen Z favored Vice President Harris over President Trump in the 2024 presidential election by just four points, strikingly less than the 25-point margin for President Biden in 2020. The 2024 result marked the strongest showing for a Republican presidential candidate among young voters since 2008. With 2026 being a midterm election year, all 435 House seats and a third of the seats in the Senate will be up for grabs. Although President Trump will not be on the ballot, the narrow margins in both houses of Congress, particularly the House of Representatives, make a change in control on at least one side of Capitol Hill a distinct possibility. Beyond a tepid economy and historical precedent, which typically sees the president’s party lose seats in midterm races, a major concern for Republican campaign strategists is the notoriously finicky attitudes among young voters. Over the Christmas and New Year’s holidays, I had the good fortune to spend a considerable amount of time with younger Millennials and those in Gen Z, including my son, daughter, nephews, friends, neighbors, bartenders, and even golf buddies. While we never really sat down to talk politics specifically, it was extremely instructive to listen to what they had to say about the major issues of the day. While I would be reluctant to contend that their comments reflect the nation’s youth as a whole, I found them interesting, nonetheless. To no one’s surprise, they expressed concern about job availability, particularly in their preferred field. Ongoing inflation, apartment affordability, and their own personal high income taxes were commonly mentioned. Interestingly, illegal immigration, drug trafficking, crime, the Trump administration’s U-turn on DEI issues, and health insurance were not major topics of discussion, although there was an acknowledgement that crime in D.C. was higher than reported. None believed that Social Security would be there for them when they retired, and there was more discussion about 401k’s and savings than I expected. They disliked to the point of disgust things such as President Trump’s “Arc de Trump,” the proposed triumphal arch for Washington, D.C., envisioned by the president to celebrate the U.S.’s 250th anniversary, and the renaming of the Kennedy Center to include the president’s name; however, they could not have cared less about the renovation of the East Wing of the White House. They expressed a clear preference for the federal government to focus on domestic issues over foreign policy ones as I heard nothing about the Ukraine/Russia conflict (this observation was taken prior to U.S. action in Venezuela). Not one mentioned climate change or the environment. In the end, their comments and discussion reminded me of a book I read as a college student at about their age, George Orwell’s The Road to Wigan Pier. The book described life among the British working class whose labor the economy depended; its plea was for politicians to gain a self-awareness about their own hypocrisies; and its thesis was that what the citizenry truly wants is not wholesale change but the removal of society’s worst abuses and a maintenance of the present’s best—family life, sports, and the local community. I guess the more things change, the more they stay the same.

Thought Leadership from our Consultants, Think Tanks, and Trade Associations

Eurasia Group Releases its Top Risks for 2026. This week, the Eurasia Group released its top ten risks for 2026, as well as four red herrings. The top risk was a U.S. political revolution, while the second involved ceding leadership to China on the power source [electrons] that will run the defining technologies of the 21st-century. The risk that stood out to me was its sixth—state capitalism with American characteristics. Last year, the Trump administration was the most economically interventionist since the New Deal. In 2026, the risk is that the White House will expand this dynamic even further, reshaping the relationship between the U.S. public and private sectors. Although President Trump is hardly the first president to embrace industrial policy, his state capitalism is personal and transactional—businesses that align with his agenda receive better treatment while those that do not risk disadvantage. Increasingly, success in M&A bids, regulatory approvals, tariff exemptions, or access to deals requires not just alignment with the president’s agenda but proximity to his inner circle. Although some in corporate America have adapted to these new rules by playing the lobbying game, the transactional approach extends to foreign governments as well. In fact, White House leverage has been expansive, and has included tariffs, equity stakes, revenue-sharing deals, regulatory action, and access to U.S. markets and technology; Japan’s $550 billion fund to finance U.S. projects is but one example. This midterm election year, the White House will face pressure to show that the president’s agenda is delivering for U.S. voters. However, with consumer sentiment at historic lows, a softening labor market, and sticky inflation, the disconnect between a promised renaissance and the reality of job losses will be hard to deny, and the prospect of political setback will push the administration to double down. Although tariffs may be harder to use, intensification will come from elsewhere—equity stakes spread to new industries, more frequent revenue-sharing arrangements, sharper regulatory leverage, and expanded views of national security. Were the economy to tip into recession or inflation to spike, President Trump would become even more risk-acceptant and his response more interventionist. Pressure on the Fed might intensify, an AI bust could trigger selective bailouts, price controls could be instituted, and the federal government may take larger equity stakes in struggling strategic industries or force consolidations to create national champions. With more intervention, not less, over time, productivity will suffer as capital flows to politically favored firms rather than the most innovative. The rule of law may erode as transactional deals rest on contested legal foundations. The U.S.’s traditional edge—predictability, property rights, and rules-based governance—will shrink. Even worse, precedent will stick; once one administration uses such tools—equity stakes, golden shares, revenue sharing—the next administration will use them too. The mechanisms President Trump is normalizing could just as easily be deployed by a Democratic administration for climate policy, labor-friendly industrial renewal, or social equity. Two decades ago, western leaders imagined China would converge toward the American model; instead, it’s the U.S. that is borrowing from Beijing’s playbook. President Trump is creating a system where the president—any president—picks winners and losers on a scale not seen in modern history. For the complete list of top risks, please contact the Washington office.

Inside U.S. Trade Predicts Supreme Court, USMCA Review Will Shape Trade Policy in 2026. A Supreme Court ruling on the legality of President Trump’s emergency tariffs and November’s midterm elections will bookend a packed year in trade, with an inaugural review of the USMCA in the middle. Early in the year, the high court is expected to decide whether President Trump properly used the International Emergency Economic Powers Act (IEEPA) to impose a slew of tariffs. Some are optimistic that the justices’ criticism of the administration’s legal defense during November oral arguments suggest the court will strike down the use of IEEPA to impose tariffs. White House officials say they have other means of imposing tariffs if they lose the case—and that tariffs are here to stay. If the Supreme Court rules in favor of the plaintiffs, the U.S. will be busy in 2026 dealing with the question of whether and how to refund billions of dollars in tariffs already paid. Also early in the year, WTO members will convene in Cameroon for their 14th ministerial conference. While a commitment to WTO reform is one possible outcome, some members also hope to expand MC14’s reform agenda. The U.S. is expected to use MC14 to push for a permanent moratorium on e-commerce duties. The Trump administration’s other major trade battleground won’t be in court or Cameroon, but in negotiating rooms with USMCA partners. The parties will hold their first review of the agreement on July 1—this month, they’ll begin to negotiate possible changes to it. The sides can decide to renew the agreement and extend it for another 16 years or let it lapse after 10. Neither USMCA nor its implementing legislation specify where or how partners must negotiate, or the pace of talks. USTR Greer is slated to meet separately with Canadian and Mexican counterparts in January for initial discussions. While USTR Greer has suggested the review’s negotiations will lean more bilateral than trilateral, both he and President Trump have said USMCA withdrawal on the table.

Observatory Group’s Lessons from President Trump’s Venezuela Operation for Beijing (and the World). Aside from the successful kinetic aspect of the recent U.S. operation in Venezuela, there was a fascinating diplomatic dimension. Hours before Venezuela’s ruler was captured, he met with China’s Special Envoy for Latin American Affairs, sent to Caracas to show Beijing’s support. Although the move was belated, and probably counterproductive, Beijing’s reaction afterward demonstrated how extremely reluctant it is to jeopardize its trade truce with the U.S. or President Trump’s visit to China in April. For China, the ideal scenario would have been for the Maduro regime to remain in power until April, which would have allowed China to use Venezuela as a bargaining chip in negotiations over Taiwan. Now, the events of the last week represent a huge setback for China’s multi-decade foreign policy in Latin America as they jeopardize all the investments made to become a strong presence in the region. Despite the public messaging on drugs and immigration, there were three underlying rationales for the U.S. operation: closing Chinese involvement with rare earth mining and processing in the region, ending Iranian drone manufacturing in Venezuela, and driving out Russian special forces as “advisers” to the Venezuelan military. Although the conventional view is that what President Trump has done in Venezuela points to a carving up of the world into hegemonic spheres, the conflict is more of a compilation of several goals in one action. While China may see the action as encouragement to be more aggressive vis-à-vis Taiwan, it would be shortsighted to heed this lesson; instead, the U.S. acted as a hegemon in its own backyard, rather than signalling that a spheres-of-influence approach is acceptable.

Politico Says it’s a New Year with New Problems. Redistricting, transgender students in sports, and abortion access were top of the docket for state legislatures last year. But it’s a new year, and with it comes a whole set of new controversies to navigate. Here’s what’s likely to be in and out of legislatures’ agendas:

IN:

- Affordability. Voters will turn to Congress and their state leaders to address kitchen-table issues like gas prices and housing costs as economic concerns dominate the conversation for another year.

- Tariffs. After almost a year of President Trump’s signature economic policy impacting state agriculture and manufacturing, the economic strain will affect both legislation and state budgets.

- Immigration. Cities have seen the immigration crackdown first-hand. As the ICE shooting in Minneapolis showed, the battle over immigration is now a local issue.

- Political violence. With violence and threats of violence at an all-time high, the safety of legislators will become both a political issue and a budget item as many look to increase security.

OUT:

- Redistricting. Cracking open congressional maps was the name of the game last year. While there are still a handful in the air, the race to redistrict has settled down.

- Transgender policies. Issues like gender-affirming care and transgender students in school sports will remain on many legislators’ agendas, but they will take a back seat to affordability issues.

- Abortion access. State legislatures have quarreled over abortion bans since the 2022 Dobbs decision. For the most part, the dust has settled.

- AI regulation. While AI regulation and data privacy was a high priority for both states and Congress, most regulation and legal battles have gone through courts rather than through legislation.

“Inside Baseball”

In the wake of the attack on the Capitol five years ago, dozens of corporations announced plans to halt their political donations to the 147 Republican lawmakers who voted against certifying Joe Biden’s victory in the 2020 election. Half a decade later, just 10 of those companies have upheld their pledges to stop contributing to congressional election objectors via their corporate PACs. That group includes Farmers Insurance, Clorox, Whirlpool, and Expedia Group, which said they would suspend all political contributions after the January 6 attack. At the same time, Airbnb, Nike, Lyft, Qurate Retail (QVC), Eversource Energy, and Holland & Hart have all upheld their pledges to cut off donations specifically to election objectors.

In Other Words

“In our lifetimes, we have never witnessed an American president so committed to and so capable of changing the political system, and, accordingly, the United States’ role in the world,” Ian Bremmer, Eurasia Group, Founder.

“We need Greenland…It’s so strategic right now. Greenland is covered with Russian and Chinese ships all over the place,” President Trump aboard Air Force One.

Did You Know

Preparations for Japanese Funds to Finance U.S. Projects have Begun. The U.S. and Japan have begun to activate their “Strategic Investment Initiative.” Officials from the two countries met formally to move forward with Japan’s $550 billion of promised investment. Analysts believe the first project may coincide with Prime Minister Takaichi’s expected April visit to Washington, and the entire $550 billion is supposed to be invested before President Trump’s term ends in early 2029. The White House is eager to announce specific investments to showcase the success of trade policy in advance of midterm elections. While there remains skepticism about the agreement, centered on how much of the pledged investment will represent new money as opposed to investments that companies were planning anyway, the threat of snap-back tariffs is a significant incentive to at least appear to be complying with the deal.

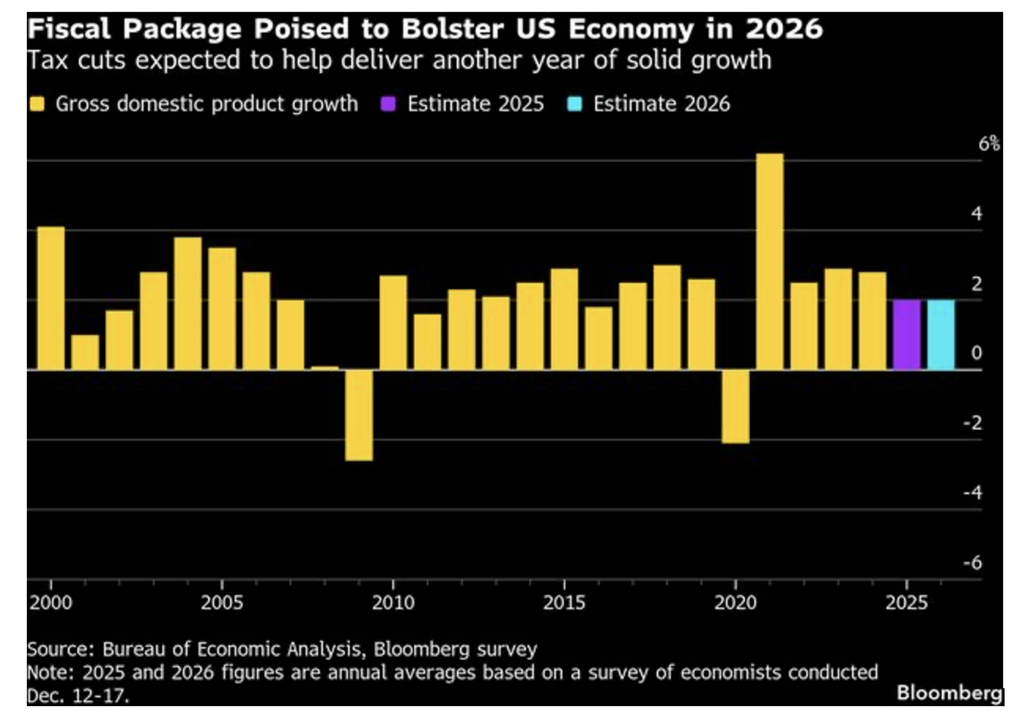

Graph of the Week

Tax Stimulus to Keep U.S. Economy on Track in 2026. After a year of policy shocks, the U.S. economy is set to get a lift from President Trump’s tax-cuts package in 2026. Americans will get bigger income tax refunds in the first half of this year, incentives for companies to invest in plants and equipment will bolster growth, and lower borrowing costs and steadier trade policy should also help. Still, forecasters see grounds for caution—any burst of consumer spending from fiscal stimulus will fade as the year goes on, tariffs will continue to weigh on businesses, unemployment is on the rise, concerns about affordability remain, the AI boom may not deliver broad-based growth, and the attack on Venezuela shows the potential for geopolitical instability. Adding it up, economists expect growth of 2% in 2026 (the same as the 2025 forecast).