Thought of the Week

How’s your “Dry January” going? Did you even try it this year? You know Dry January; it’s the public health initiative where after a period of overindulgence during the holidays, participants abstain from all alcohol for January’s 31 days. The idea is that by consuming zero alcohol between January 1st and the 31st, one might be able to improve their health, save money, sleep better, notice weight loss, increase energy, and reduce liver fat and blood pressure. Certainly, one of the key benefits of Dry January is the absence of any hangovers, which is more than can be said for the U.S. and other nation’s that attended last week’s World Economic Forum. According to Washington-based analysts, among the hangover risks that came out of last week’s Swiss-inspired cocktail party are:

- Greenland. Although the U.S., Denmark, Greenland, and NATO are trying to negotiate and reach a mutually acceptable solution, the issue could become a flash point again, particularly if President Trump’s demands cannot be met due to domestic Danish political factors.

- 100% tariffs on Canada. While President Trump is highly unlikely to follow through, the tariff threat was to put Canada (and others) on notice not to deepen trade relations with China.

- USMCA negotiations. Rather than tariffs, the White House is likely to retaliate against Canada during USMCA negotiations. Canada, compared to Mexico, will be singled out in an effort to score political points during the USMCA’s summer talks.

- The UK. Will President Trump criticize Prime Minister Starmer’s visit to China the same way he did with Canada. If so, it would be an indication that the administration is forming a short-term strategy to deter allies from cozying up to Beijing.

- Tariffs for Seoul? President Trump could implement higher tariffs on goods from South Korea in response to its legislature not yet ratifying the US/Korea trade agreement.

- IEEPA Tariffs. Do not expect any significant change in most tariff rates or trade policy if the Supreme Court strikes down the use of IEEPA. The Trump administration will simply swap to deriving authority from other laws, and continue, as much as possible, existing tariff rates. If the court allows continued use of IEEPA the current agenda will continue.

- Access to U.S. markets. If tariffs are not available, the White House may instead use the threat of denying trade partners access to American markets, including oil and LNG supplies. However, the risk of the administration following through with this threat is low.

What about my January? Mine was more “Damp” than “Dry.” While I reduced my intake from levels seen Thanksgiving through New Year’s Eve, “Dry January” enthusiasts would have generously referred to my occasional imbibes of celebratory libations as “slip-ups.”

Thought Leadership from our Consultants, Think Tanks, and Trade Associations

American Enterprise Institute (AEI) Says Not All Checks on President Trump have Bounced. The markets, courts, and Congress all restrained President Trump’s power in 2025, and they will do so again in 2026. While the president began the year flexing his muscles in Venezuela, Iran, Greenland, and Gaza, for all the talk of a second-term president running roughshod over the Constitution, President Trump ran into several guiderails. Limiting his room to maneuver more than most assume stands the markets, the courts, and Congress. Consider the attempt to acquire Greenland. While President Trump wanted the strategic island and was willing to ratchet up military and trade tensions to get it, in the end, he blinked. Speaking to the World Economic Forum, President Trump said he still wanted Greenland, but reassured the audience he wouldn’t use force to get it. A few hours later, tariffs were called off, and a “framework” was announced. Crisis averted; what changed? Financial markets. The day before his speech, stocks and bonds plunged, and markets rebounded as soon as he said he wouldn’t send in the Marines. Similarly, last April, when President Trump’s “Liberation Day” speech, announcing reciprocal tariffs, sent global markets into a tailspin, as soon as the president agreed to pause the tariffs, markets recovered. A pattern can be seen when one considers last October’s duel between Presidents Trump and Xi over rare-earth minerals. President Trump drives the global economy to the brink of a trade war; markets react sharply; and the president retreats. In short, President Trump tests institutional boundaries, and markets provide a real-time response. When the response is sharply negative, Mr. Trump goes in another direction. The courts provide a second check on the White House. In fact, many of President Trump’s executive orders have been tied up in litigation, and plaintiffs have won more legal victories than the administration. What’s more, the Supreme Court could soon rule against the White House’s attempt to fire Federal Reserve governor Cook, implement emergency tariffs, and ban birthright citizenship. While the markets and courts block the president overtly, Congress restrains him more subtly. Consider that President Trump signed fewer laws in his first year than any other modern president; more than 50 subcabinet appointments had to be withdrawn; and discharge petitions have forced votes on bills without White House support. The damage to the president from the markets, courts, and Congress has been real. Going forward, Democrats are favored to take the House in November. A Democratic Congress may not only impeach President Trump, but would end his legislative agenda, and, in the case of a Senate loss, stall executive and judicial appointments. President Trump’s reach doesn’t extend as far as either he or his detractors would like to admit.

Eurasia Group Predicts U.S. or Israel is Likely to Bomb Iran in the Coming Months. Despite the decision to forego strikes in January, both the U.S. and Israel see an upside in taking military action against Iran; strikes are likely before April 30th (a 65% probability). While diplomacy talks will focus on Iran’s nuclear program, missile program, and support for regional proxies, there is no indication they will bear fruit on any of those issues, with the U.S. maintaining a hard line on Uranium enrichment and Iran seeing its missile program and proxy support as vital deterrents against foreign attacks. The U.S. will have assets in place—including at least one aircraft carrier—by the end of January, although it is more likely that action will come after a period of several weeks to allow for preparations and to give space for talks to run their course. The U.S. and Israel have a range of options for taking action; a purely symbolic strike is unlikely, with an attack most likely to focus on military targets or Iran’s missile program.

Democratic Political Strategist Doug Sosnick’s Midterm Election Outlook and the GOP Pushback. A clear majority of the country disapproves of the job President Trump is doing, as reflected in four January polls that have been released to coincide with the end of the president’s first year in office. While the polls are consistent in their findings and cannot be dismissed as “fake news,” the question remains whether things can only get worse for the GOP. Typically, a president’s polling rarely improves after their first year, and there is nothing in the most recent polls to suggest that President Trump will buck the trend. Most Americans do not believe the White House is aligned with their priorities, and views of the U.S. economy are generally bleak—most voters hold President Trump responsible, rather than his predecessor. Consumer confidence is near historic lows, and the president is even underwater on his favorite policy areas — tariffs and immigration. Despite this, Democrats face a real battle in the midterms, particularly in the race for the Senate. Democrats have hemorrhaged support from working class voters, who constitute 60% of the electorate, and as a result there are wide swaths of the country where Democrats cannot compete, greatly reducing their opportunities even with a “blue wave” election. Sosnick’s full memo can be found here: The full memo and here: Slide deck. The pushback: Republican sources familiar with the GOP’s midterm strategy have pushed back on Sosnick’s assessment of President Trump’s approval ratings, which they insist are comparable to previous presidents. Sources also stressed Democrats’ unpopularity within their own party, pointing to recent numbers suggesting that they aren’t faring much better than President Trump. Republicans expect the economy to keep improving over the first half of this year, boosting GOP chances in the general election. In addition, messy primaries in Democratic Senate targets like Maine and Michigan could have an effect, while the advantages of incumbency and fundraising should help in these swing seats.

“Inside Baseball”

Brookings Institution on President Trump’s ‘America First’ Trade Policy Agenda. Trade policy is no longer treated primarily as a mechanism for promoting efficiency within a rules-based system nor as a narrowly constrained instrument for mitigating discrete security risks. Instead, it now plays a central role in shaping the domestic economy and building bargaining power and leverage across commercial, strategic, and security domains. Rather than being used to facilitate market outcomes, trade policy has been deployed in ways that reflect an emphasis on pulling production and capacity into the U.S. or under American control. Whether one views the shift as necessary, dangerous, or misguided, it represents a departure from the framework that has guided U.S. trade policy for decades. The distinctions in governing logic and context matter because policy tools—tariffs, trade restrictions, investment screening, and enforcement measures—produce very different responses from market participants and trading partners. Understanding the shift in the role of trade policy is not only a prerequisite for evaluating its consequences, it clarifies the stakes of current debates about trade, economic security, and national security.

Bloomberg Government Sees Corporate America Retooling its Lobbying Strategies in Trump 2.0. Executive branch decision-making is increasingly centralized with President Trump, and companies need to engage in high-level conversations with the administration to achieve their goals. The lobbying industry has seen a shift in hierarchy, with firms having close ties to the president seeing their revenue increase, and companies are now targeting a narrow group of individuals with administration ties. Companies are working to be proactive rather than reactive to the Trump administration’s agenda, and are using strategies such as sending in CEOs and donating to fundraising efforts to influence policy.

In Other Words

“Now, if the U.S. military, acting jointly with us, comes under attack, and Japan does nothing and retreats, the Japan-U.S. alliance would collapse,” Japanese Prime Minister Takaichi in the case of a Taiwan crisis.

“If we don’t change our approach, it will have a negative effect on the midterms, for sure,” Rep. Newhouse (R-WA) on the Trump administration’s approach to immigration enforcement.

“I think Gavin Newsom may be cracking up, some of these things he’s saying. I think he may be in over his hairdo…To say strange things like President Trump is a tyrannosaurus rex, what the hell does that mean? I can say Gavin Newsom is a brontosaurus with a brain the size of a walnut,” Treasury Secretary Bessent at the World Economic Forum.

Did You Know

The only current U.S. governor not born in the U.S. is Nevada Governor Joe Lombardo, the Republican was born in Sapporo, Japan, while his father was stationed there with the U.S. Air Force.

Graphs of the Week

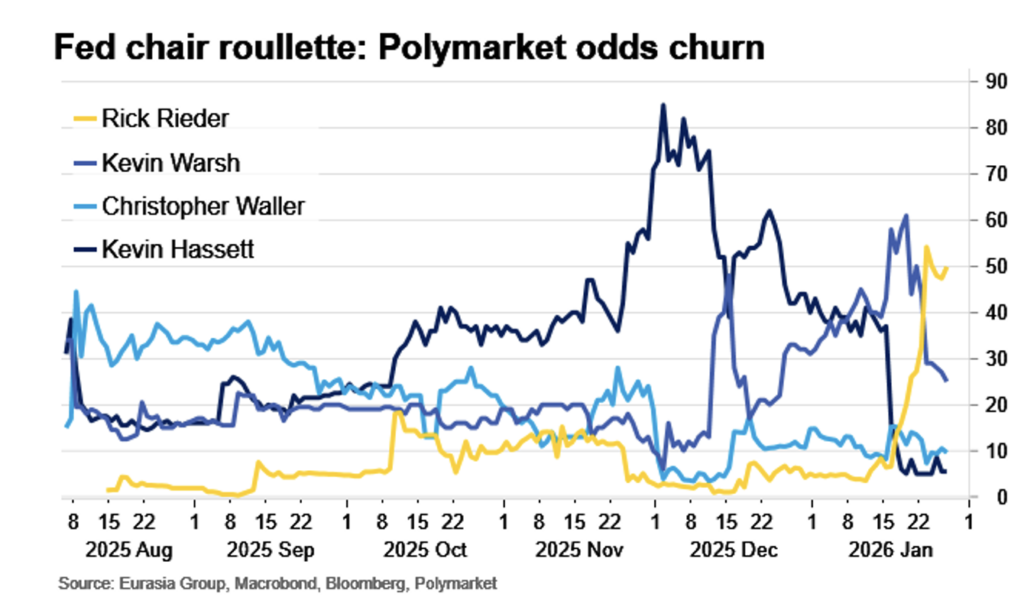

The Fed Will Resist Politicization, Regardless of the Chair. No one should expect an imminent announcement concerning a new Fed chair as there is no immediate deadline to force President Trump to do so. On the shortlist, Rick Rieder is the frontrunner. Of all the candidates, he would make the president look best: a Wall Street success story with credibility with financial markets. His lack of association with the Fed could also make him palatable to Treasury Secretary Bessent, while his lack of association with the Trump administration could be attractive to pivotal Republican votes like Senator Tillis (R-NC). Kevin Hassett is likely underpriced in betting markets at under 10% odds. Although Hassett is not the favorite, he remains the only Trump loyalist on the shortlist. Should the president prefer a loyalist—as he has across the executive branch—Hassett would be the pick. Regardless, the Fed will resist politicization. Events of the first year have demonstrated that the guardrails surrounding Fed independence remain strong. The fact that monetary policy requires a vote of the entire FOMC means that the chair must be a consensus-builder, and political and judicial constraints on the president’s ability to politicize the Fed remain robust.

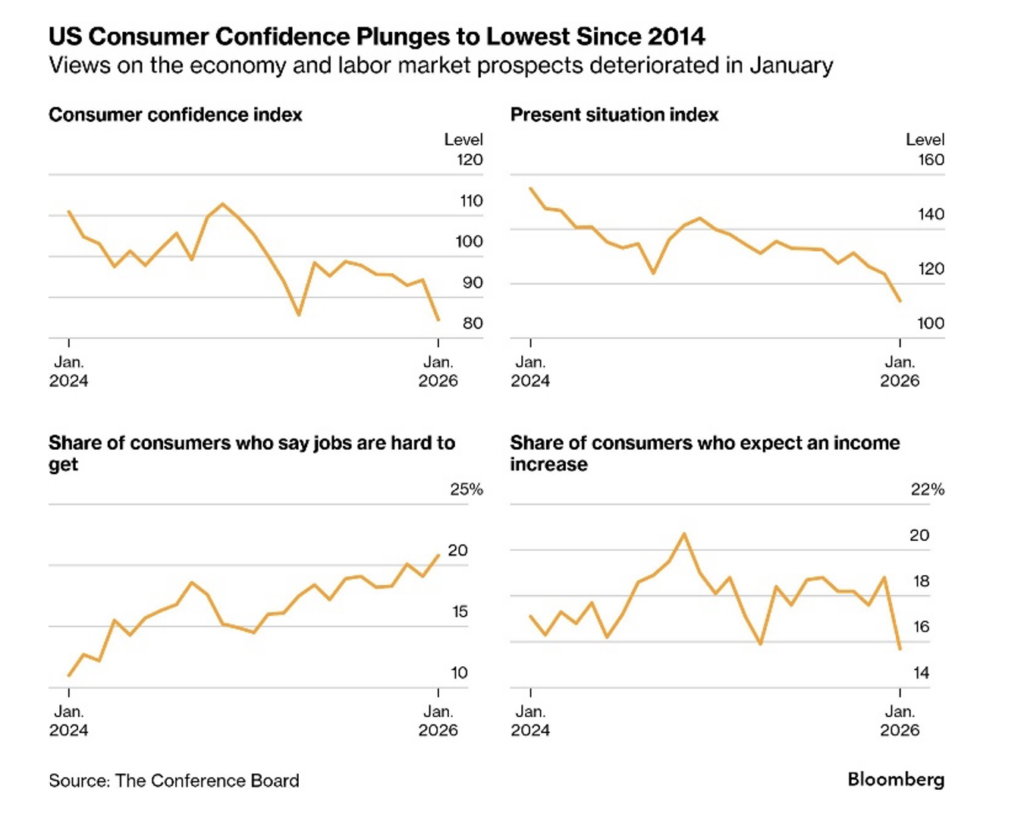

Confidence Tanks. Consumer confidence plummeted in January to its lowest level in 12 years on more pessimistic views from Americans worried about the nation’s economy, inflation, and a weakening labor market. The Conference Board gauge decreased to 84.5, from an upwardly revised 94.2 last month. The figure was the lowest since May 2014, and it fell short of all estimates in a Bloomberg survey of economists.