Thought of the Week:

In his autobiography, when discussing how “figures often beguile” him, Mark Twain popularized the phrase “there are three kinds of lies: lies, damn lies, and statistics.” Delivered in Twain’s classic satirical style, although not directly attributed to him, the phrase resonates immediately as we all know what he meant. Statistics can be powerfully persuasive, and when presented without sufficient context they can be manipulated to support different arguments and create false impressions. Like any tool, statistics can be used ethically or unethically; it all depends on how the data is collected, analyzed, and presented. Earlier this month, President Trump fired Bureau of Labor Statistics (BLS) commissioner Erika McEntarfer following the release of a weaker-than-expected jobs report that painted an unfavorable picture of the economy and stoked concern about White House tariff policy. More specifically, after the July jobs report showed mostly flat numbers and revised job numbers from earlier months down, the president fired a widely respected, nonpartisan economist, who 86 senators voted to confirm to her position just last year, because he said the revisions were too big and designed to hurt him politically. In reality, as revisions go, they were about average, just not in a positive direction. As you may know, the BLS is a federal agency that collects and disseminates various U.S. economic and labor market data, including the Consumer Price Index (CPI), the Producer Price Index (PPI), the Import/Export Index (MXP), and various figures on employment, labor force participation, productivity, and wages. BLS statistics significantly impact corporations by providing crucial data for informed decision-making across various aspects of business operations. Companies rely on BLS statistics to understand market trends, manage costs, assess labor conditions, and make strategic choices related to investment, pricing, and hiring. To replace Dr. McEntarfer, President Trump has nominated EJ Antoni, an economist at the Heritage Foundation. Although he has a PhD in economics and is a highly entertaining figure on conservative talk radio, Dr. Antoni has only worked in conservative think tanks and has no experience managing an organization the size of the BLS. Whether he can replicate the experience of Bill Beach, President Trump’s first-term BLS head, who turned out to be a competent and respected commissioner despite a career in mostly right-leaning think tanks, remains to be seen. It’s almost certain that Antoni will be confirmed in a highly partisan Senate vote in September.Analysts tell the Washington office that the signposts to watch during his confirmation hearing include whether he commits to maintaining a data-collection and review process independent of the White House, whether he plans wholesale changes to senior staff, and whether he appears willing to be the bearer of bad news to the president himself. For the time being, his appointment has accentuated market concerns about the reliability of BLS data moving forward. Over the remainder of President Trump’s second term, we’ll have to see whether the BLS becomes a source of lies, damned lies, or just plain old statistics.

Thought Leadership from our Consultants, Think Tanks, and Trade Associations

Capstone Says the China Tariff Deadline Extension is Not a Sign of Thawing Relations. Earlier this week, President Trump signed an executive order extending the U.S.-China tariff truce an additional 90 days; however, a significant liberalization of U.S.-China trade remains unlikely. President Trump will look to maintain a baseline 30-40% tariff on most imports from China supplemented by Section 301 tariffs of up to 25% from his first term and Section 232 tariffs from recently completed and ongoing negotiations. While both sides think they can wait the other out, the Trump administration believes tariffs will begin to take a significant toll on China’s export-dependent economy over time and that pressure should grow because of transshipment provisions included in recent trade deals. On the other hand, Chinese negotiators believe they have uncovered a key U.S. vulnerability with restrictions on critical mineral exports and that President Trump is vulnerable to public opinion and pressure from the business community. Negotiators are working toward a “skeleton deal” like those signed between the U.S. and major trading partners such as the EU. U.S. priorities for a deal will include enshrining a substantial tariff baseline and obtaining commitments from China to purchase American goods. This may be a non-starter for Chinese negotiators who are likely to want to avoid the appearance of offering concessions without receiving anything in return.

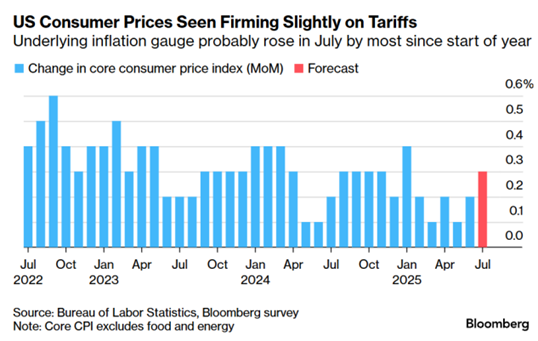

Observatory Group Points Out the Fed’s Conundrum. Since January, the Fed has been saying that it expected tariff effects to raise prices and cut economic growth. And if that became the case, the policy outlook would be cloudy, given that both the Fed’s mandates would be threatened. Moreover, it would be difficult for policymakers to anticipate any move far in advance, given the unknown timing and extent of potential tariff effects. With the release of the July CPI, the U.S. finds itself in exactly that position. Core inflation accelerated to 3.1%, well above the Fed’s 2% target and higher than the readings that prompted the FOMC to pare back its rate cut outlook late last year. Although financial markets seem to have viewed the number as good enough to assure a rate cut, a number of Fed policymakers are not so relieved given strong expectations of an acceleration in goods prices. In fact, most Fed policymakers generally assume that tariff effects have only begun to materialize, and that it will take a few more months to discern who is paying the bulk of the tax and how consumers are managing. In the meantime, inflation expectations are no longer as sensitive to tariff announcements as they were earlier this year, which is good news. At the same time, the labor market has shown clear signs of weaker demand and weaker supply. Weak labor demand became a more compelling factor in the policy debate this week, despite the alarming inflation data and outlook. If a survey of FOMC members were held today, it would almost surely reveal a majority for a 25 bp rate cut; however, this could change several times before the next FOMC meeting, given the amount of data still to be released before September 17, which is why the market’s 90%+ odds of a rate cut is aggressive.

$2.3 trillion Worth of Imports Could be Hit by President Trump’s Latest ‘Reciprocal’ Tariffs. Most of President Trump’s long-awaited reciprocal tariffs took effect August 7. After months of uncertainty, a 10% baseline tariff was levied on nearly every country, with some major trading partners, like India and Brazil, seeing steeper total rates of 50%. Those totals are the highest on record since the Great Depression. The U.S. imported nearly $3.3 trillion of goods in 2024, almost all of which will be subject to the reciprocal tariffs. Mexico and China, who both received a 90-day pause on the new tariffs’ implementation, were notably absent from the recent series of executive orders, although previously applied tariffs are still in effect. The two countries alone made up $944 billion in imports last year. Many American businesses have already reported billions in increased costs due to the tariffs, even as countries like Japan, members of the EU, and the U.K. struck deals to invest billions in American energy and infrastructure projects.

In Other Words

“Our economy is booming, and E.J. will ensure that the numbers released are HONEST and ACCURATE,” President Trump.

Did You Know

Of all the states, Nevada is the one with the least number of listings on the National Register of Historic Places.

Graphs of the Week

So Far, American Businesses have Taken Nearly 64% of the Hit from Tariffs; however, the burden will increasingly be passed on to consumers as companies hike prices. According to Goldman Sachs, U.S. consumers’ share of tariff costs will rise to 67% if the latest levies follow the patterns from previous years. The forecast adds credence to the widespread view among economists that the new fees on imported goods will fuel inflation—exactly the reason given by the Federal Reserve for the delay in lowering interest rates. As higher tariffs start to filter through to consumers, a Bloomberg survey projects that the core consumer price index rose 0.3% in July, which would be the biggest gain since the start of the year.

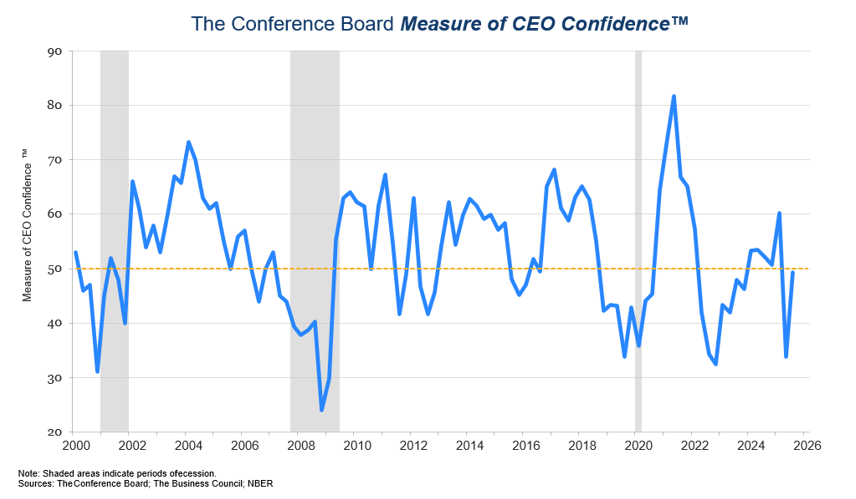

CEO Confidence Revived in Q3, but Remains in Cautious Territory. The Conference Board’s Measure of CEO Confidence rose to 49 in Q3, up 15 points from Q2 (a reading below 50 reflects more negative than positive responses). Although CEO confidence recovered, it still fell short of signaling a return to optimism. CEOs’ views on current economic conditions made the sharpest recovery. Their six-month expectations for the economy as a whole and in their own industries also improved. Fear of recession within the next 12–18 months eased dramatically, to 36% in Q3 from 83% in Q2.