Thought of the Week:

Last year, during the Christmas holiday, I purchased each member of my immediate family one of those Page-a-Day Calendars that I thought matched their personality. Among others, I bought calendars on Zen, Dad Jokes, Sports Trivia, Cats, and Crossword Puzzles. If I would have bought one that included a Word-of-the-Day, there is no doubt that “tariff” would have popped up this week. Over the weekend, a number of those in my network who don’t reside directly within Washington’s political bubble, including certified financial planners and stockbrokers, franchising entrepreneurs, and tech executives who fill data centers with IT equipment all asked me about President Trump’s trade policy and expressed concerns about the impact of tariffs. On Monday, famed political analyst Charlie Cook’s Off to the Races series noted how the prospect of widespread tariffs had taken the trade-policy debate from the abstract to the very real in record time. By Tuesday, The Conference Board Community’s feature question asked, “Which executive action of the new administration has had the greatest impact on your business so far or will likely have the greatest impact on your business?” The overwhelming answer from corporate representatives was market uncertainty caused by tariffs (policies on federal government employment and DEI were distant seconds). By mid-week, the Washington office was visited by members of an Asian embassy’s Office of Commercial Affairs [not Japan’s] who were trying to gain a better understanding of Trump trade policy, specifically tariffs. We even had a discussion with a congresswoman in the Republican leadership who felt compelled to insist that President Trump remains “business-minded,” sees things through an “economic lens,” and his goal in using tariffs is to “level the global playing field.” She said the economy will have to endure short-term pain, but the tariffs will reset things for the long-term. “Of course there’s an appreciation for global supply chains, but it’s going to be messy and take a minute,” she told me. No matter where you turned in Washington this week—Uber rides, think tanks, sandwich shops, trade associations, bar stools, or lobbying shops—tariffs were the word-of-the-day. Although there seems to be a general understanding of what tariffs are—the Congressional Research Service (CRS) defines a tariff as a tax levied by one country on the goods and/or services imported from another country—there does not seem to be a widespread understanding of why tariffs, why now, and what’s next, even among those who should be in the know. For me, the answer isn’t to be found in narrowly focusing on the seemingly reactionary nature of President Trump’s tariff policy, which has led to wild market fluctuations. Discussions with former Trump administration staff, think tank scholars, and trade association analysts provide some insight. According to those who served in trade-related positions during Trump 1.0, the answer to why tariffs and why now is that those in Trump 2.0 just don’t believe tariffs will lead to enduring inflation. Their reasoning: they didn’t during the first Trump administration, and what’s more, tax cuts, deregulation, energy exploration, and investment promotion should counter the inflationary nature of tariffs, just as they did in 1.0. For good measure, they say that it even took President Reagan two years to turn things around. In terms of what’s next, most trade association and think tank explanations revolve around similar themes, but the clearest comes from the American Enterprise Institute (AEI). According to AEI, President Trump doesn’t think about foreign relations through the prism of diplomacy or trade. He sees foreign relations, whether economic or political, through his own self view: as a dealmaker. And in this realm, tariffs offer negotiating leverage. For those who view economics from a global commerce or international relations standpoint, tariffs are universally damaging; however, if you’re one who believes that everything comes down to dealmaking, then having the most leverage is clearly an advantage…and tariffs create leverage. While the on again/off again levying of tariffs risks a boy who cried tariff lesson, if one sees tariffs as a necessary evil on the path to a good deal, then tariffs make sense. Next week’s word(s): derivative products.

Thought Leadership from our Consultants, Think Tanks, and Trade Associations

Brownstein Places Trump Tariffs in Three Buckets. It’s no stretch to say that tariffs are a vital part of the Trump administration’s economic and international policy agenda. Less than two months into his new administration, the president has imposed tariffs on major trading partners, expanded product-specific tariffs to address national security concerns, and proposed a new system of reciprocal tariffs that would completely reform the current multilateral trading system. To date, the tariffs discussed by the White House can be placed in three buckets—Fentanyl Tariffs, Reshoring Tariffs, and Reciprocal Tariffs. Fentanyl tariffs, which for the most part have been imposed through a novel use of the International Emergency Economic Powers Act (IEEPA), target Mexico, Canada, and China. The administration formally cited Canada’s and Mexico’s failure to stop illicit immigration and shipments of deadly drugs such as fentanyl into the U.S. as the reason for imposing the tariffs. Concerning China, the White House cited the influx of synthetic opioids, such as fentanyl. Reshoring tariffs are intended to force manufacturers to shift production of targeted goods to the U.S. These tariffs target specific goods or industries, like aluminum and copper, and additional targeted tariffs, including on pharmaceuticals, are expected in the coming months. These are levied under Section 232 of the Trade Expansion Act of 1962 and either amend an existing tariff or direct a Commerce Department investigation. Reciprocal tariffs are expected to target specific countries based on tariffs imposed on U.S. exports as well as other non-tariff trade barriers that undermine U.S. market access. Initial recommendations for such tariffs will be made by the Secretary of Commerce and U.S. Trade Representative (USTR) on April 1 following the completion of a presidentially directed review. The president said he intends to announce these tariffs on April 2.

Eurasia Group Says Trump Course Corrections Show Political Risk of Moving too Fast. Last week, President Trump ran up against the third rail of U.S. politics, especially Republican politics: a combination of agricultural interests, manufacturing, equity markets, veterans, and Social Security. The White House’s rapid reverse pivot on tariffs was driven primarily by direct intervention from automakers facing a near-existential risk from proposed tariffs on Canada and Mexico. Commerce Secretary Lutnick used the moment to advance a more process-driven approach that aligns with the core of the GOP (and their constituents). However, last week’s reversal does not alter the view that tariffs are far less “deal-able” this time around and that tariff rates will increase through 2025. In fact, tariff delays for Canada and Mexico do not preclude tariff application in the future, although the delays suggest that threats on both may be rolled into larger USMCA negotiations set to unfold later in the year. Beyond tariffs, GOP Senators pitched DOGE and Elon Musk on using congressionally directed recissions to enact cuts to already-approved government funding. While the Senate has endorsed some of Musk’s push to cull programs, they are telling him that they will have the final say in what exactly gets cut. And President Trump later reiterated that cabinet secretaries—not Musk—have the final say over federal workforce decisions. Exactly what that may change is unclear but politically it gives cabinet secretaries a clear foothold to push back on some of Musk’s initiatives. Clipping Musk’s wings, albeit only slightly, may narrow his influence, but it does not mean he will play no role going forward.

“Inside Baseball”

Former Ambassador to Japan Rahm Emanuel is mulling a run for president. The former congressman, mayor, and White House chief of staff is doing the media rounds at the moment; name a political podcast and Emanuel has likely already been on it or will be shortly. It appears that the one-time DCCC chair is road-testing the first outlines of a stump speech, or at least an issue he can make his own. His current message involves the need, in his eyes, to discuss the classroom rather than the bathroom, a reference to the debate over transgender students’ access to restrooms.

In Other Words

“I have every major industry in Kentucky lobbying me against them: the cargo shippers, the farmers, the bourbon manufacturers, the homebuilders, the home sellers—you name it—fence manufacturers. The bourbon industry says they’re still hurt from the retaliatory tariffs [during the Trump 1.0]. So do the farmers,” Sen. Paul (R-KY) on complaints from business about the potential impacts of Trump’s tariff policies.

Did You Know

President George Washington signed the Tariff Act of 1789 on July 4, 1789. It was the first substantive piece of legislation passed by Congress.

Graphs of the Week

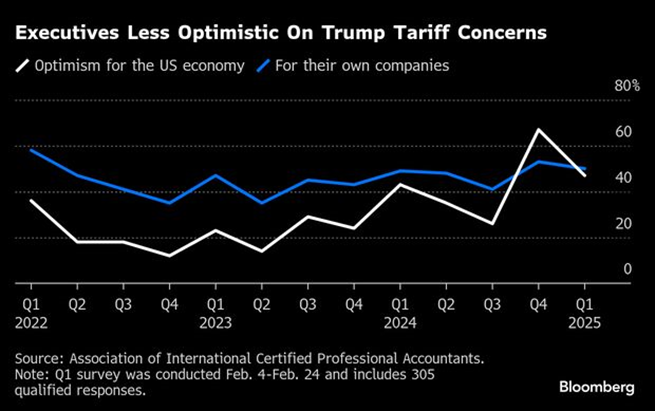

Uncertainty Around Tariffs, Inflation has Hurt Business Optimism. In the two months since President Trump’s return to the White House, we have seen a sharp reversal from the buoyant mood originally expressed by business executives. In fact, less than half (47%) say they’re confident about the economic outlook for the year ahead, down from 67% in December. The findings coincide with data showing eroding consumer sentiment and rising inflation expectations, driven by concern about the effects of President Trump’s tariff policy. To date, the relentless aspect of the tariff agenda has overshadowed the administration’s other more business-friendly plans, including proposed tax cuts and lighter regulation.

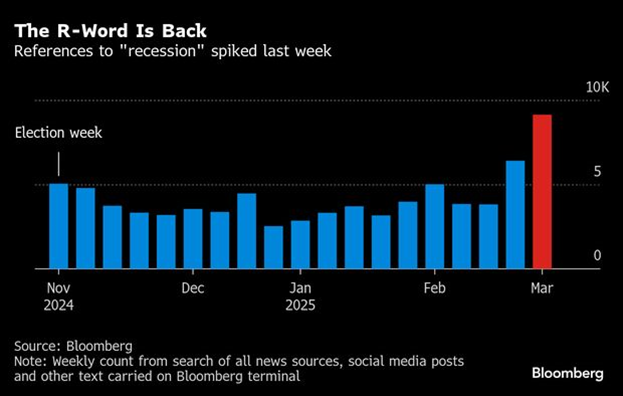

In his First Term, President Trump Slashed Taxes Before Beginning a Trade War. Today, it’s the other way around—and the economic backdrop looks shakier, with high interest rates squeezing markets and inflation proving sticky. Above all, his second-term tariffs are both steeper and less predictable, as the on-again, off-again levies imposed on Canada and Mexico have shown. All of this is driving a slump in stock markets, which President Trump has always viewed as a barometer, and triggering recession talk, although tax cuts could revive animal spirits, as they did in 2017.