Thought of the Week:

Unlike the elementary school where my son teaches, Washington’s five inches of snow this week did not shut down the start of the 119th Congress. In fact, official Washington has been abuzz the last several days with the election of Rep. Mike Johnson (R-LA) as Speaker of the House; the certification of Donald Trump as the 47th President of the United States; President Carter’s state funeral; fallout from President Biden’s blockage of Nippon Steel’s acquisition of U.S. Steel; and non-stop speculation from lobbyists, consultants, think tanks, and associations about what the next two years may bring. At the moment, absolute clarity on any issue is difficult to find. For instance, it even remains unclear whether Republicans, who control both houses of Congress as well as the White House, will pursue one reconciliation bill or two (reconciliation bills are unique in many ways, not the least of which is that they can pass the Senate by a simple majority vote thereby avoiding a filibuster). Complicating matters is the notion that the incoming Trump administration is comprised of two, often competing, groups—a pro-growth group and a nationalist/populist group. While the pro-growth group wants to focus on using deregulation, AI, expanded domestic energy production, and tax reform to supercharge economic growth, the populist group wants to use the power of the state to reshape America in a more U.S.-centric manner utilizing tariffs, “near-shoring,” deportation, and an “America First” foreign policy. Prior to President-elect Trump’s inauguration on January 20, in an effort to garner insight into where things may be headed, the Washington office had the opportunity to meet in a closed door briefing with current Congressional staffers, former Deputy USTRs from both the Biden and Trump administrations, and a former Deputy Director of the White House National Economic Council. Included among the points they all agreed on were:

- At the end of the day, we will see the imposition of some sort of global tariff simply because President-elect Trump wants one, and he will get one.

- Any global tariff will be broad based initially; while countries will be able to negotiate exclusions, product-specific exemptions will be handled on a case-by-case basis.

- Because of the difficulty in scoring and the GOP’s tight margin in the House, tariffs will not be used as “payfors” in any reconciliation bill.

- On day-one there will be a China tariff announcement, most likely building on the existing Section 301 process.

- Despite feeling less burdened than during his first term, President Trump will be responsive to how the stock market reacts to his actions.

- In response, trading partners will issue retaliatory tariffs on politically sensitive products—think Kentucky bourbon or Levi’s Jeans.

- In terms of mindset, the incoming administration does not believe that tariffs will have a large impact on inflation.

- Anyone who claims they know what Trump will do, doesn’t.

Thought Leadership from our Consultants, Think Tanks, and Trade Associations

The Conference Board’s U.S. Economic Forecast. The U.S. economy ended 2024 on strong footing after a year of surprisingly robust growth. However, a myriad of uncertainties loom over 2025, suggesting somewhat slower economic activity and material risks. The economy expanded 2.7% year-over-year in 2024; is expected to rise 2.0% in 2025; and real GDP growth in 2026 should settle at its potential rate of 1.8%. Inflation is expected to stabilize at the Fed’s 2% target by Q4 2025, later than the original Q2 2025 estimate. Consequently, the Fed may achieve its neutral rate target range of 3.0-3.25% in October 2025, also several months later than originally anticipated. The prospect of somewhat higher inflation and a more measured pace of interest rate cuts suggests that the economy may grow close to potential in 2025. Similar to the Conference Board, the Congressional Budget Office (CBO) estimates potential real GDP growth at 2.1 % in 2025. Upside risks to this projection include continued outperformance of American consumers and major revivals in housing and business investments as interest rates, while elevated compared to pre-pandemic norms, should be far lower than they are now. Major downside risks include trade wars, tax hikes, and government spending cuts, which would all dampen growth more than the 2% pace projected.

Eurasia Group Says US—Canada, Greenland, Panama Canal Talk is an Expansion of the Playbook, Not a Sideshow. In his press conference earlier this week, President-elect Trump laid out several unconventional foreign policy demands, including taking control of Greenland, Canada, and the Panama Canal, and demanding that NATO members spend 5% of GDP on defense. These comments are an expansion of the Trump policy playbook, not a sideshow worth dismissing. Introducing a plethora of new foreign policy demands, some of them unrealistic, accomplishes several goals: it diverts attention away from domestic economic policy issues such as inflation; it increases the chances that Trump wins a subset of his foreign policy demands or at least delivers on key concessions; it signals to other nations, particularly China, his commitment to expand American shipping dominance in the West, its military in the presence in the Arctic, and its access to critical resources in order to compete vigorously on the world stage. The tone and tenor of the press conference also underscores a central argument: Trump is starting from a very different place relative to 2017, and he is willing to disrupt commonly held norms not only domestically but in foreign affairs as well. In fact, the president-elect’s willingness to flout norms related to national sovereignty will likely complicate future negotiations on disputed territories, chiefly in Ukraine.

Eurasia Group Says Biden’s Rejection of Nippon Steel Will Not Reduce Japan’s Appetite for U.S. Investment. President Biden blocked Nippon Steel’s $15 billion proposed purchase of US Steel on national security grounds. Blocking the deal gives Biden a final platform to burnish his protectionist record. The deal had been jinxed from the start because of acute political sensitives to a foreign firm buying an iconic American brand, drawing opposition not only from Biden but also from Donald Trump, JD Vance, and Kamala Harris. Nippon Steel fought mightily for the deal, but it was never able to reach an agreement with the leadership of the United Steelworkers, which strongly opposed it. While the Japanese firm is challenging the rejection in court, judges tend to be highly deferential to decisions by the executive branch on national security grounds. Although Biden’s verdict deeply disappoints Tokyo, a key ally of the U.S., Japanese government officials always recognized the political obstacles the bid confronted. Only in recent weeks did Tokyo step up its low-key campaign in favor of the transaction. Despite the rejection, Japan’s appetite for investing in the U.S. will remain strong; Japan has been the top foreign direct investor in the U.S. for the last five years—a trend that is likely to continue.

Global Business Alliance (GBA) Comments on Biden Administration’s Decision to Block the Nippon Steel-U.S. Steel Deal. Late last week, President Biden officially blocked the $14.9 billion sale of U.S. Steel to Japan’s Nippon Steel, citing a strategic need to protect domestic industry. Under intense political pressure, the Biden administration’s action comes after the Committee on Foreign Investment in the United States (CFIUS) deadlocked over its review of the proposed sale. The GBA, the only trade association that exclusively represents the interests of foreign subsidiaries operating in the U.S., released the following statement: “President Biden’s announcement to block this acquisition is barely news, given he committed to do so before the review process had even gotten underway. Japan is one of America’s strongest allies and Japanese companies have reinvested more into the U.S. economy and workforce than any other nation. [We are] concerned that today’s decision sends a powerful and negative signal to the rest of the world that America may no longer honor its longstanding open investment policy of treating major U.S. employers equally, regardless of where they are globally headquartered. To subvert national security laws to advance campaign pledges undermines the trust and economic cooperation that are central to our nation’s prosperity. International companies directly employ 8.4 million U.S. workers with high-quality jobs, including nearly three million U.S. manufacturing jobs. These investments are key drivers of America’s economic growth and job creation. This decision sets a dangerous precedent and sends the wrong message to our friends and allies.” Although President Biden’s announcement effectively prevents the acquisition from going forward, both Nippon Steel and U.S. Steel have filed a petition in the U.S. Court of Appeals for the D.C. Circuit challenging the decision as a violation of due process under CFIUS authorities.

“Inside Baseball”

Congress, Trump Look at Reconciliation to Address Legislative Priorities. This week, Congress began to consider President-elect Trump’s call to use the budget reconciliation process to pass a host of legislative priorities he says will be paid for with tariffs. Using reconciliation, the Senate can pass budget measures with a simple majority, bypassing the normal 60-vote threshold. According to Punchbowl News, reconciliation has gained favor among a growing number of legislators to pass a variety of Republican priorities, including tax reform. In addition, lawmakers and the new administration could attempt to use reconciliation to address a host of trade priorities, including Generalized System of Preferences (GSP) renewal; an overhaul of the de minimis program; and Trump’s own trade concerns—a 10% duty on all trading partners, a 60% rate for goods from China, an end to China’s permanent normal trade relations (PNTR) status, and an additional 25% tariff on China and Mexico due to fentanyl and immigration concerns. Reconciliation could also be used as a vehicle to allow Trump to impose reciprocal tariffs as a trade penalty. Although the president-elect has said he does not need Congress to enact his tariff plans, tariff-focused legislation, passed under reconciliation, would be more permanent and could mollify certain lawmakers who have expressed skepticism about the executive branch’s authority to move forward with sweeping trade policy changes absent congressional approval.

Proxy Voting for New Parents. A bipartisan group of lawmakers is pushing Speaker Johnson to allow proxy voting for new parents, reports Punchbowl News. While the Democratic-controlled House allowed proxies during the pandemic, and the practice continued after Congress returned to the Hill, some members abused the privilege by working from home. Once Republicans regained control in 2022, then-Speaker McCarthy ended the practice. Today, Rep. Luna (R-FL) is leading a charge to bring back the practice under a narrow scope. Luna gave birth to a son during her first term in 2023, and has asked Johnson for a proxy voting carve-out for new parents. Along with Reps. Pettersen (D-CO), Lawler (R-NY), and others, Luna is filing a resolution to allow new parents to vote by proxy. Besides the practical advantages of allowing new parents some flexibility, the resolution could also help Johnson’s tenuous political situation. At full strength Republicans have a 220-215 majority, leaving Johnson very little room for error on any vote. But he may not be at full strength until the second half of this year, thanks to the resignation of former Rep. Gaetz (R-FL) and upcoming vacancies left by members joining the Trump administration. For the next few months, Johnson will have just a 217-215 majority to work with. This leaves room for error, where even a single member’s absence could torpedo, or at least delay, President-elect Trump’s legislative agenda.

In Other Words

“I don’t welcome people who want to work solo or be a star. My team and I will not tolerate backbiting, second-guessing inappropriately, or drama. These are counterproductive to the mission,” incoming White House Chief of Staff Susie Wiles.

“Greenland is an incredible place, and the people will benefit tremendously if, and when, it becomes part of our Nation. We will protect it, and cherish it, from a very vicious outside world,” President-elect Trump.

“If, as I expect, tariffs do not have a significant or persistent effect on inflation, they are unlikely to affect my view of appropriate monetary policy,” Federal Reserve Governor Waller downplaying the extent to which the Trump tariff agenda might affect inflation. Waller is a contender to replace Fed Chair Powell in 2026, and remarks like this boost his reputation in Trump’s inner circle.

Did You Know

Following Richard Nixon and Al Gore, Kamala Harris became just the third vice president to take on the uncomfortable task of certifying their own presidential election loss.

Naomi Biden Neal and Peter Neal welcomed a baby boy to the world this week, making President Biden the first great-grandfather to occupy the White House.

Graph of the Week

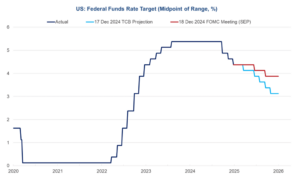

Conference Board Reacts to the Hawkish Fed Rate Cut and Sees a March Cut as a Maybe. As expected, the Federal Reserve cut interest rates by 25 basis points at its December 2024 meeting; however, the Fed also sent a strong message in its Summary of Economic Projections (SEP) that the inflation fight is far from over. Among the SEP’s material revisions was a delay from 2026 to 2027 in the return to a 2% inflation target and a slower pace of interest rate cuts. Additionally, the cutting cycle may not end until 2027 or even later, not in 2026. Although Conference Board projections also raised growth and inflation forecasts, lifted the unemployment rate for the next two years, and delayed the timing of convergence to the 2% inflation target, the SEP’s changes were more dramatic. While the SEP is not technically a forecast, at the least, expect a pause at the January 2025 meeting and be less certain about a March 2025 cut.