Thought of the Week:

My wife and I just returned from a vacation to the British Virgin Islands (BVI). There we sailed the islands Christopher Columbus “discovered” during his second voyage to the Americas in 1493. These are the same islands that, according to legend, Blackbeard used as his hideout and that Robert Lewis Stevenson made famous in his book Treasure Island. One thing I expected to see while island-hopping was Jost van Dyke’s world-famous Soggy Dollar Bar, known for its invention of the Painkiller cocktail (I may have had one…or two); one thing I didn’t expect in my line of sight while snorkeling through The Indians’ coral formations was a reef shark (although he seemed generally disinterested, the encounter led me to make a beeline back to the boat). Because I’ll be traveling for business next week to speak at the Interacid Group Summit, and there will be no new Washington Connection, what I thought I’d do in this edition is offer a sneak peek into a few of the conclusions I’ll offer in my presentation. I’ve been asked to speak on the broad topics of the U.S. economic outlook as well as the state of American politics over President Trump’s first 100 days. Not surprisingly, the overall theme of the presentation will revolve around uncertainty, volatility, and unpredictability. For the U.S. economy we see the risk of stagflation—a combination of stagnant economic growth and heightened inflation expectations—increasing largely due to an inversion of the yield curve, contractions in manufacturing, falling consumer confidence, and rising inflation expectations from both consumers and businesses. With the Trump administration’s telegraphed gameplan being tariff pain for the year’s first two quarters, followed by tax and deregulatory relief in the last two quarters, our thesis is for an expected rebound in 2026. This thesis draws on our belief that the Fed will begin to cut rates sometime in the second half of this year and then continue to normalize policy, that the Trump tax cuts will be extended through passage of a reconciliation bill, that additional deregulation will occur through the remainder of 2025, and that additional trade deals will be announced and finalized. In terms of politics, although the 2026 midterm elections are sometime away, our early analysis suggests that Republicans will maintain their hold on the Senate—the GOP currently holds a 3-seat majority, only six of the 33 races are deemed competitive, and of those Democrats are defending four seats while Republicans are only defending two. However, Speaker of the House Johnson (R-LA) will have his hands full trying to hold on to his slim majority. With the GOP enjoying just a seven-seat majority (with two vacancies in seats previously held by Democrats), and 13 Republican House members currently in districts carried by former Vice President Harris vs. only three Democrats in seats won by President Trump, it’s anyone’s guess right now which party will control the House. As always, feel free to contact the Washington office on either of these topics, we’re always ready to dive in.

Thought Leadership from our Consultants, Think Tanks, and Trade Associations

Eurasia Group Says a USMCA Deal is Unlikely During Trump’s Presidency. President Trump’s tariffs and focus on supply chain reshoring, coupled with ongoing struggles over immigration, fentanyl, and national security, reduce the likelihood over the next four years of reaching a comprehensive agreement while reviewing the U.S.-Mexico-Canada Agreement (USMCA). Several scenarios present themselves:

- Zombie USMCA (45% odds): the base case in which negotiations to update the agreement fail, but the three parties maintain the existing framework. This would result in annual reviews of the USMCA throughout Trump’s term, with ongoing sectoral tariff disputes, while Mexico and Canada hold out for a more favorable deal post-Trump.

- USMCA-Light (30% odds): The three countries reach a limited, less ambitious deal. This would allow for the reintroduction of certain tariffs and a weakening of the dispute settlement mechanism. While it would provide a degree of stability, it would also dilute the spirit of the USMCA and complicate future efforts to renegotiate terms after Trump’s second term.

- Trade War (10% odds): Trump’s sustained tariff policy leads to escalating tit-for-tat tariffs, degrading economic conditions without any country formally exiting the agreement.

- Fortress North America (10% odds): The U.S. focuses its attention on its trade war and competition with China, leading to deeper North American integration and a more cohesive regional bloc.

- Full Withdrawal (5%): While unlikely, this scenario would occur if President Trump unilaterally decides to exit the USMCA after Canada and Mexico fail to appease his demands.

Regardless of the USMCA’s outcome, White House actions have already undermined North American economic predictability and the credibility of the agreement, stifling investment and regional competitiveness. Although Canada and Mexico will continue to seek U.S. market access, the future of trilateral integration very much depends on Washington’s preferences.

Inside U.S. Trade: Businesses Contend IEEPA’s ‘Silence’ on Tariffs Undercuts Trump’s Orders. A number of businesses have sued the Trump administration over its use of the International Economic Emergency Powers Act (IEEPA) to impose tariffs. They argue that the lack of any mention of tariffs in the law shows that it was never meant to enable them, and that recent Supreme Court precedent forbids judges from reading new executive authority into such “statutory silence.” The Justice Department’s claim that IEEPA provides authority for tariffs collides with Supreme Court decisions limiting deference to White House interpretations of unclear or ambiguous statutory text, says the New Civil Liberty Alliance (NCLA), a conservative law firm representing a coalition of businesses behind the IEEPA suit. The question of which court has authority over the challenges has become deeply intertwined with the core legal issue of whether IEEPA authorizes tariffs at all. While the Department of Justice argues that IEEPA allows the president to “investigate, regulate, or prohibit any transactions in foreign exchange” and “regulate importation” of foreign-owned goods in response to a national emergency, the NCLA says reading those provisions to cover tariffs runs afoul of the Supreme Court’s “major questions doctrine,” which requires clear statutory authorization for executive actions that carry “major economic or political significance.” What’s more, the NCLA points to the “statutory silence” on the issue, which it says was a key element of the Loper Bright Enterprises v. Raimondo decision. There, the Supreme Court scrapped its decades-old “Chevron deference” principle that gave agencies broad leeway to interpret unclear statutory text.

Institute of International Finance (IIF) Describes its Global Macroeconomic View as Being in “A Fog of Trade.” The effective U.S. tariff rate now tops 25%, the highest since the 1970s, and it is fueling global economic uncertainty. Over 30 nations face divergent outcomes, shaped by exposure, alignment, and negotiation speed. With more than 140 carveouts having been issued, inconsistent rules are complicating corporate planning. Although the 90-day pause on “extra” reciprocal tariffs has spurred talks, the overall process remains fragmented and opaque. Uncertainty has ceased to be a passing disturbance—it’s now baked into the policy landscape. What once felt like episodic turbulence, tied to pandemic shocks, energy disruptions, or supply-chain snarls, has given way to something more entrenched—policy-driven unpredictability. Trade is now the frontline. On April 2, the Trump administration unveiled a sweeping tariff package, triggering a cascade of bilateral responses and ad hoc recalibrations. Even with a 90-day grace period, the effective U.S. import tariff rate rose past 25%, surpassing the 2018–2019 trade war peaks, reaching the highest level since the 1970s, and potentially approaching rates not seen in a century. A fragmented negotiation process has followed with widely divergent country strategies and a broader erosion of predictability in global trade. What the world is witnessing is not a return to orderly managed trade or rules-based compromise—it’s a shift toward opacity, unilateralism, and an erosion of global trade visibility.

“Inside Baseball”

Broad U.S.-Japan Trade Deal Likely by Mid-June. Analysts report that there is about a 65% chance that the U.S. and Japan will reach a broad trade deal by the G7 Summit in Canada (June 15-17). The leaders of both countries are eager to strike an agreement. President Trump wants to show skeptics that he can reach a deal with a major trading partner, while Prime Minister Ishiba hopes to settle the trade dispute before upper house elections in July. Working-level meetings started on May 2, and by mid-May the two sides will speed their pace of ministerial-level meetings to about once a week. There is a 35% probability that it will take longer to reach an agreement. A key benchmark to watch is whether President Trump agrees to cut the 25% tariff on Japanese automobile imports. Given the importance of the automobile industry to the Japanese economy, Tokyo needs concessions on that tariff from Washington before a deal can be struck.

In Other Words

“This is Biden. And you could even say the next quarter is sort of Biden because it doesn’t just happen on a daily or an hourly basis,” President Trump after the GDP report showed a decline in Q1.

“America is the Schelling point of global finance. We have the world’s reserve currency, the deepest and most liquid markets, and the strongest property rights. For these reasons, the United States is the premier destination for international capital,” Treasury Secretary Bessent citing Nobel laureate Thomas Schelling at the Milken Institute Global Conference.

Did You Know

Since taking office January 20, President Trump has granted pardons or commutations to about 1,600 people. The bulk of those have been for people charged in connection with the Jan. 6, 2021, riot at the Capitol. The remaining include white-collar criminals, anti-abortion activists, cryptocurrency entrepreneurs, and two ex-associates of Hunter Biden who turned on the former president’s son. You may recall that President Biden pardoned his son, his siblings, and political allies during his final hours in office. The Constitution puts almost no limits on the practice, although leaders typically wait until the end of their tenure to award clemency.

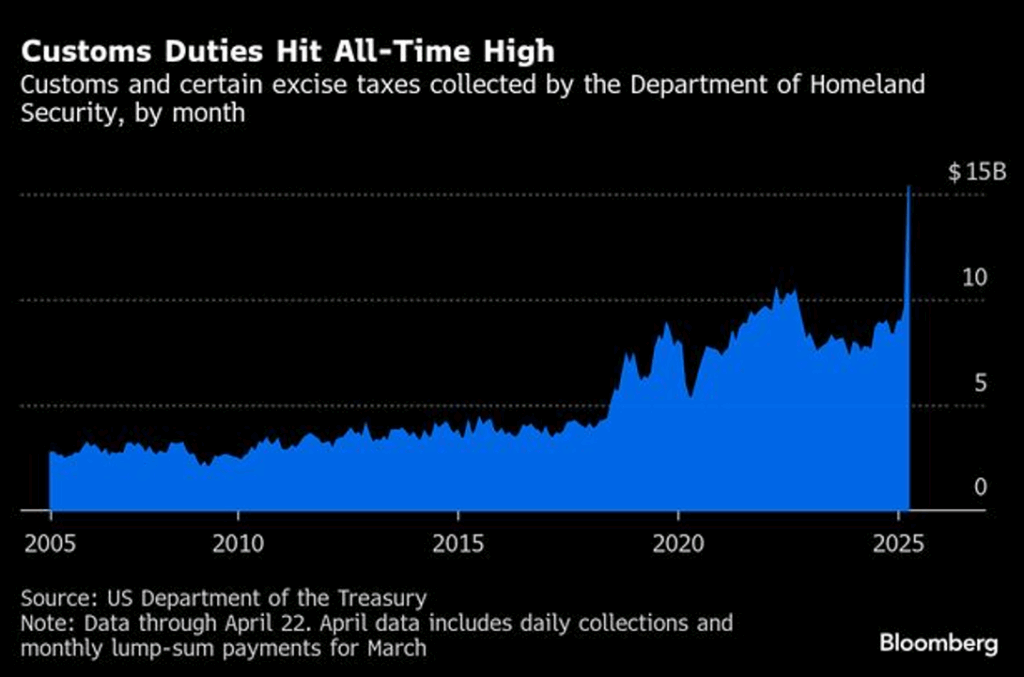

Graph of the Week

U.S. Customs Duties Hit New High as Trump Tariffs Take Effect. Revenue from customs duties spiked more than 60% in April as the first of President Trump’s new tariffs took effect, bringing in at least $15 billion, according to the Treasury Department. While the data reflects customs duties that importers/brokers paid in April on imports arriving in U.S. ports in March, the numbers largely do not account for the 10% universal tariff that was announced on April 2—meaning that collections in May could surge even further.