Thought of the Week:

Earlier this week, sitting in an introductory pitch meeting with one of Washington’s leading public policy consulting firms, discussing the first 45 days of the second Trump administration, one word jumped out at me. I actually circled it in my notepad. Now, Washington is full of lobbyists, lobbying shops, law offices, and consulting firms. By some estimates there are more than 12,000 lobbyists in the nation’s capital, and lobbying is a more than $4 billion a year industry. Added to the ranks of D.C.’s advocacy class are hundreds more law offices (229 National Law Journal 500 firms alone) and scores of consulting companies. As one can imagine, when vying for new clients at the outset of any administration, it’s difficult for these K Street denizens to stand apart from one another; hyperbole may be one way to do it. So, as I listened to the well-connected political insiders at the conference table across from me, the single keyword that made me sit up and take notice? “Schizophrenic.” Whoa, here was a representative from a high-stakes public affairs firm equating current presidential policy with severe mental illness. Said in jest, to make a point, probably, but still it’s not the term I would have chosen when approaching a potential client for the first time. “Contradictory,” sure, I could have given them that. For instance, take the president’s call for a weaker dollar to help American exporters; well, tariffs, a staple of the Trump White House’s economic policy, would only serve to strengthen the dollar. Or what about promises to tackle inflation. It’s well known that tariffs and other import barriers are inflationary, but so are other aspects of Trump policy. Consider that the president has called for the largest deportation of illegal immigrants in history. Putting aside any social or cultural dimensions, the reduction in the nation’s labor force that would result from mass deportations would also lead to higher prices. Maybe it wasn’t just trade and immigration they were referring to, but the inclusion of other aspects of the Trump agenda as well. Take the new Department of Government Efficiency (DOGE). President Trump brought on the world’s leading entrepreneur, Elon Musk, to lead DOGE’s efforts. Psychological research has shown that the brain scans of highly creative people, like entrepreneurs, and those suffering from schizophrenia mimic one another, and university researchers from Stanford found that 49% of entrepreneurs deal with at least one mental illness such as ADHD, bipolar disorder, addiction, depression, or anxiety; in fact, a full 72% of entrepreneurs self-report their own mental health concerns. Still, “Schizophrenic” isn’t the word I would have chosen; DOGE’s actions to date seem relatively straight-forward. In the end, “Chaotic” is probably the word I would have used. Taken alone, the president’s frantic rollout of his on again-off again tariffs has injected a tremendous amount of business uncertainty into the economic outlook. Just two months into the administration, even supporters are beginning to question White House strategy. Chaos, confusion, contradiction is no way to run a business.

Thought Leadership from our Consultants, Think Tanks, and Trade Associations

Bloomberg Government Raises the Specter of a “Trumpcession,” Says it’s Not Just Tariffs, Other Growth Risks Too. President Trump’s latest trade-war, possibly the largest act of American protectionism since the 1930s, will likely put the brakes on U.S. growth in the near term—and it’s just one of the shocks piling up for consumers, businesses, and investors. There’s also DOGE’s cuts to the federal workforce, the clampdown on immigration, and a potential drag on business investment amid rising policy uncertainty. Add it all up, says a growing consensus among economists, and it spells a slowdown for the world’s biggest economy. While few see much danger of an outright contraction this year, and there are growth-friendly measures like tax cuts in the pipeline too, the specter of “Trumpcession” has been raised. An escalating tit-for-tat trade war would only amplify it—and President Trump has made plain that many more tariffs will follow the ones already imposed on Mexico, Canada, and China. Future targets include the European Union, autos, pharmaceuticals, and semiconductors, as well as the “reciprocal” tariffs that White House aides are calculating based on various barriers to U.S. goods overseas. While there might be some backsliding along the way, the tariff wave is cresting amid clear signals of slower growth and higher inflation. Consider that consumer spending fell by the most in nearly four years in January; confidence has weakened; factory activity fell last month; and a gauge of prices paid for materials surged to the highest since June 2022. Although analysts caution against reading too much into a single month of data, especially one skewed by severe weather, the Atlanta Federal Reserve’s real-time forecasting tool predicted a 2.8% first-quarter contraction. Yes, it’s an outlier, most indicators aren’t pointing to a severe downturn, but calculations based on models used by the Federal Reserve during the first Trump administration suggest the latest tariff shock could cut 1.3% off U.S. GDP and lift core inflation by 0.8%.

Eurasia Group Believes Minerals Deal Could be Saved with Additional Concessions from Ukraine. After President Trump’s bust-up with Ukrainian President Zelensky in the Oval Office last week, the Ukrainian minerals deal is on life support. However, Zelensky is being urged privately to put his row with Trump behind him and to return to Washington to sign the deal, which he once appeared ready to embrace. This means the deal could still be saved, though it would require additional concessions from Zelensky—either material or rhetorical—that allow Trump to claim he maintains the upper hand. The reception in Ukraine to Zelensky’s actions in the meeting has been supportive so far, limiting the scale of concessions he is willing to make to Trump. But the minerals deal is vital to keep the U.S. involved: as long as the deal stands, Washington has “skin in the game” and a reason to remain invested in Ukraine’s future. Absent that, Trump will see limited incentive to maintain U.S. involvement. President Trump is not facing any meaningful pushback in the Republican Party from the meeting. Even prominent Ukraine supporters in the party, such as Senator Graham (R-SC), have become more critical of Zelensky in recent days, and pro-deal figures like Secretary of State Rubio and National Security Advisor Waltz have been partially sidelined. The lack of pushback will limit the extent to which Trump will be willing to reconcile with Zelensky and move back toward a position more aligned with the Ukrainians and European allies.

Observatory Group Sees the America First Investment Policy Memo as Previewing More U.S.-China Decoupling. Last month’s, America First Investment Policy memo was the Trump administration’s third aggressive move against Beijing in a week, after the maritime executive order and announcing another 10% tariff increase. The memo seems to indicate that Trump 2.0’s nationalist faction is currently dominant compared to the growth advocates vis-à-vis China, and the nationalists are setting the U.S. on a path to escalation against the PRC and speeding up U.S.-China decoupling in trade, production, and investment. The memo instructs the Committee on Foreign Investment in the United States (CFIUS) to tighten restrictions on investments by Chinese companies and those from other adversarial nations in key sectors such as tech, agriculture, and infrastructure, and it may lead to forced divestment. The Trump administration also plans auditing and potentially banning Chinese companies with ADRs from listing on U.S. exchanges. The memo’s scope is very wide: it even asks agencies to explore blocking Chinese access to U.S. human capital and revoking the 1984 tax treaty between the countries. At the same time, the memo encourages investment from entities based in allied nations, especially firms that can prove they do not have Chinese ties. As an inducement to invest, the memo proposes that companies fitting these parameters will have their security reviews fast-tracked. The memo also proposes new measures to stop outbound U.S. investment into the Chinese military-industrial complex. If implemented, it may also block ERISA and other pension funds from making any investments in China or other adversarial countries, including via global equity index products. From the memo’s approach, it seems clear that the Trump administration will eventually weigh going further, banning, or restricting sales of certain high value-added products in the U.S. from any company with supply chain or other links to China or other adversarial countries. The memo’s release should prompt urgent contingency planning for the vast number of companies operating or selling products in the U.S., especially in national security linked sectors, and it should be taken as a formal notice that businesses and investors will have to choose sides in the decoupling.

“Inside Baseball”

White House Seeks to put 443 Federal Properties Up for Sale. The federal government is considering selling a portfolio of properties across 47 states, the District of Columbia, and Puerto Rico, part of President Trump’s campaign to shrink the federal workforce—and the buildings it occupies. An inventory of 443 “non-core” assets posted by the General Services Administration (GSA) includes many prime commercial buildings. In total, the structures represent almost 80 million rentable square feet of usable space—12 times the size of the Pentagon. The GSA estimates that selling them could save more than $430 million in annual operating costs. It’s not clear how much the government’s buildings could be worth, given the idiosyncrasies of each property and market, or even what it could expect to net in a sale. Overall, commercial real estate is still reeling from higher interest rates and the Covid pandemic. Remote work has also cut demand for office space, leaving many big cities with more vacancies, and converting commercial buildings to residential use is difficult at a time when construction and financing costs are steep. While commercial tenants tend to prefer new space with more amenities, many buildings in the federal portfolio are old and in need of significant repair. About a third of the buildings on the list are in the Washington, DC, metro area, and they make up a disproportionate share of the square footage. Among the departments whose buildings are up for sale are Agriculture, Energy, Health and Human Services, Housing and Urban Development, Labor, Justice, and Veterans Affairs. Any relocations from these properties would threaten the already hard-hit D.C. office market. As it is, the share of D.C. office space available for lease was nearly 24% at the end of 2024, higher than the city’s pre-pandemic availability and above the current level in Manhattan.

In Other Words

“Tariffs are about making America rich again and making America great again. And it’s happening, and it will happen rather quickly. There’ll be a little disturbance, but we’re OK with that. It won’t be much,” President Trump during an address to a joint session of Congress.

“I don’t feel like people are blaming him on that yet, but I think that’s a risk you get three, six months down the road,” Georgia Governor Kemp on whether high prices could weigh on the Trump administration’s popularity; at 48%, Trump’s approval rating is fairly strong, but his net approval has fallen from +8 to +1 since his inauguration.

Did You Know

Earlier this week, President Trump addressed a joint session of Congress, essentially delivering his fifth State of the Union address. At over one hour and forty minutes, the speech set a record for the longest such presidential address. The previous record for longest State of the Union address belonged to former President Clinton, who approached an hour and a half in 2000. The record for shortest modern address belongs to President Nixon, who spoke for a little under 30 minutes (Presidents Carter and Reagan also delivered speeches around the 30-minute mark). However, the shortest State of the Union was delivered by President Washington; it was just 1,089 words Only two presidents failed to deliver a State of the Union address: Presidents William Henry Harrison and Garfield—they both died before they got the chance.

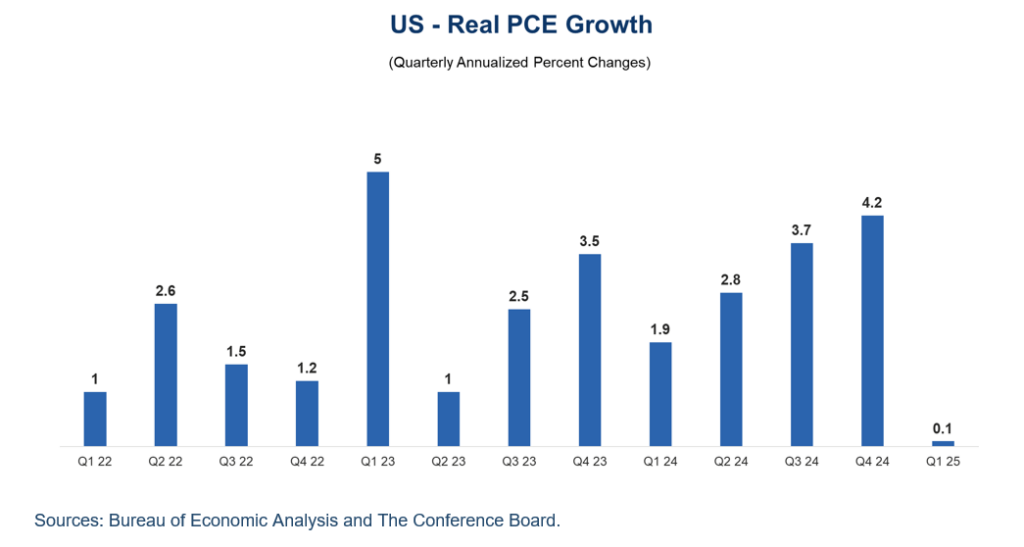

Graphs of the Week

Conference Board Says Consumer Pullback Amid Falling Optimism Points to Growth Slow-down. A sharp pullback in consumer spending at the beginning of the year, despite rising income, corroborates declining consumer confidence numbers, supports projections for economic growth to slow this year, and for the next Federal Reserve move to be a rate cut.