Thought of the Week:

In Great Expectations, Charles Dickens wrote that “Spring is the time of year when it is summer in the sun and winter in the shade.” How right he was. Consider that it’s March Madness, and while my team Maryland made it to the “Sweet 16,” they had to face Number 1 Florida to advance. They didn’t. Not to be outdone, the Washington Nationals start the season in first place (just like every other team), but their Opening Day opponents were the 2024 NL East champion Philadelphia Phillies, featuring former Nats star Bryce Harper. He homered, and the Nats lost in 10 innings. And while the Tidal Basin is currently bathed by the cherry blossoms’ peak bloom, like every year they will be as fleeting as they are beautiful. Next week, April 2, will also mark the advent of President Trump’s imposition of “reciprocal” tariffs on imports from around the world. The president insists that his tariffs will bring summer in the form of a “liberation day,” and White House officials claim the tariffs will help rebuild the U.S. manufacturing sector, bring down costs, raise trillions of dollars in revenue for the government, and force other countries to lower their own barriers to U.S. exports. However, many mainstream economists warn that President Trump’s tariff regime may represent more April showers than summer sun. They contend that higher tariffs are unlikely to bring in as much revenue as the White House projects and carry a number of costs that could far outweigh any benefits. As outlined in Politico, chief among their arguments against the use of tariffs are:

- Tariffs could boost manufacturing production, but not jobs. Any employment boost from a return of manufacturing is likely to be muted due to the advances and use of technology. What’s more, even if tariffs create new manufacturing jobs, there might not be workers to fill them. Studies estimate that there could be as many as 1.9 million unfilled manufacturing jobs by 2030 because of a skills shortage.

- Tariffs might not help trade-battered communities. S. manufacturing employment peaked at 20 million workers in 1979. While millions of those jobs were lost as production shifted out of the country, there is no guarantee tariffs will bring jobs back to the same communities where they were lost.

- Tariffs could increase costs on poor Americans. Most of the costs of the tariffs would be felt by Americans in the bottom 60% of the income bracket through higher prices for goods—with little or no offsetting gain from lower income taxes.

- Tariffs could make U.S. manufacturing less competitive globally. A third of U.S. imports are raw materials and “intermediate goods” used to make final products. Imposing tariffs on those goods would make it more expensive to build products in the U.S. compared to other countries. Also, tariffs on imported goods tend to increase the dollar’s value, making U.S. exports more expensive for buyers.

- Tariffs could help other export countries. Because not every country will retaliate, in some cases, companies that export to the U.S. will simply try to make up lost sales by finding new markets.

- The U.S. market is attractive, but maybe not that attractive. With tariffs, other countries are unlikely to trade in the same manner or same amount. For instance, investors might think twice about building new facilities if it becomes too expensive to import materials or policy becomes too unpredictable.

Thought Leadership from our Consultants, Think Tanks, and Trade Associations

Eurasia Group Believes a Middle Ground Tariff Regime Will Be the Likely Landing Spot. Reports that the April 2 tariff announcements will be “narrowed” do not imply a total walk-back of tariff plans; what’s more, with just a few days left, the reports could be overtaken by any number of events, including President Trump’s own unpredictable nature. To that end, the White House laid out a much more aggressive course of action after initial reporting of a tariff narrowing. The administration is still working out what they want to do, to whom, and when—and the only certainty is that we will see an avalanche of conflicting reporting as various White House advisors push their own preferred outcome and the president works to protect his image as a tough dealmaker. The landing spot for tariffs will likely marry elements of a broad reciprocal framework with more targeted actions, with tariffs on a select list of nations of particular concern likely the only actions taking immediate effect. Sectoral tariff investigations into autos, semiconductors, and pharma products have been floated multiple times by the administration, although any immediate announcements would likely focus on investigations that would play out over the course of months. This does not include tariffs imposed as part of separate actions targeting Canada and Mexico. Canada and Mexico should be considered separately from the reciprocal tariff announcement, with full implementation of the 25% rate likely. A negotiated climbdown to something more aligned with a reciprocal rate is possible but will not likely come together to stave off implementation on/before April 2. The final list of countries that will face immediate action is not yet settled—Treasury Secretary Bessent’s recent comments left the final target list largely unaddressed, although it is expected that it will focus on nations with both high tariff and trade balance disparities as well as nations with significant political impetus for the president. The most important thing about April 2 is that there is an April 3 and infinite days afterward; whatever happens now is just the start, not the sum of what will be imposed.

Observatory Group Says the U.S.’s Debt Limit Problem Should be Solved by Mid-Year. Analysts agree that the U.S.’s debt limit issue will be resolved by Congress sometime between June and July; without action, the Congressional Budget Office (CBO) reports the U.S. will likely breach its debt limit in August or September. There is a greater than 50% probability that relevant legislation will be dealt with separately from reconciliation. The debt limit will probably be part of a supplemental appropriations package that also includes provisions for disaster relief. Such a package would pass with bipartisan support, especially if Democrats are given wins on such efforts as robust disaster funding or a higher child tax credit. Senate Democrat support may be necessary to overcome a filibuster. Although Republican fiscal conservatives may vigorously oppose raising or suspending the limit, this will not be an issue if bipartisan support can be achieved. If that fails, then the package could still get through, but would require the promise of big spending cuts, to win the necessary votes in Congress. While the White House will need to lobby Republicans heavily for support, there is almost no risk of technical or actual default, even though there will be considerable brinkmanship along the way. At the same time, a bipartisan resolution could delay progress on the larger reconciliation package, pushing it to later in Q4 and making the U.S. fiscal trajectory more uncertain for a longer period.

“Inside Baseball”

Republicans have just about reached the deadline to introduce measures aimed at nixing the final rules of the Biden era without having to worry about filibusters from Democrats. Bloomberg Government recently took a close look at the Congressional Review Act (CRA), and found that Senate Republicans had until roughly March 25 to introduce resolutions opposing specific regulations under the Congressional Review Act. After that, they will have slightly more time—potentially until early to mid-May—to use the expedited procedures that lets them bypass Democratic support. The exact deadlines will depend on how many days the House and Senate are in session, and final official determinations will be made by the Senate parliamentarian. House members will have until roughly April 1 to introduce their CRA resolutions. The CRA gives Congress a chance to reject executive-branch rules finalized in the last 60 legislative days of a congressional session without its action being subject to a Senate filibuster. To see the CRA in action, the House will take up measures on the floor to relax new energy efficiency standards for freezers and refrigerators (H.J. Res. 75 and H. J. Res 24).

In Other Words

“April 2nd is Liberation Day in America! For decades we have been ripped off and abused by every nation in the world, both friend and foe. Now, it is finally time for the good ol’ USA to get some of that money and respect back. God Bless America!” President Trump.

“You can’t even answer the question of whether you were on the chat?” Sen. Warner (D-VA) to Director of National Intelligence Tulsi Gabbard.

“I think there’s this notion…[that] we’ve all got to be like Winston Churchill, [or] the Russians are gonna march across Europe. I think that’s preposterous,” Steve Witcoff, President Trump’s top overseas envoy.

Did You Know

There have been five bills introduced in the House of Representatives over the past two months that would: (1) put President Trump’s face on the $100 bill; (2) create a new $250 bill with President Trump’s face on it; (3) make President Trump’s birthday (June 14) a federal holiday; (4) rename Dulles Airport after Donald Trump; and (5) carve the president’s face on Mount Rushmore.

Graphs of the Week

Staggered Tariff Rollout with Immediate Impacts on April 2. The first week of April will likely see the staggered rollout of country-wide, reciprocal, and product-specific tariff investigations (a 70% likelihood), with some reciprocal tariffs having an immediate impact on high-risk countries. Broad reciprocal tariffs based on the International Emergency Economic Powers Act (IEEPA) will likely apply to countries with the highest trade imbalances and quantified non-tariff barriers. The administration’s analysis, driven by a January executive order on an America First Trade Policy, will focus on calculating reciprocal rates and product-specific targets to execute policy priorities, such as reshoring manufacturing and addressing Chinese overcapacity; automotive tariffs will be the first product-specific duties applied in this vein. While year-end average applied tariffs may reach 15%, resulting in as much as a 1.5% reduction in GDP and as much as a 1.5% increase in price levels, the administration will concurrently seek avenues for negotiating more favorable market access amid the staggered tariff rollout.

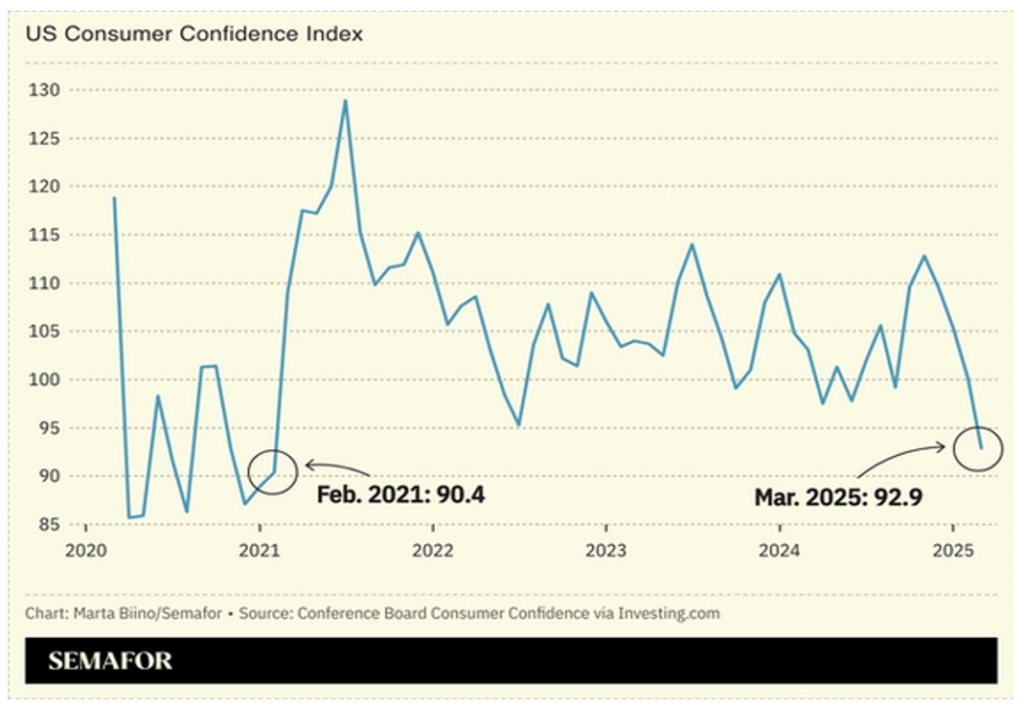

The Conference Board’s U.S. Consumer Confidence Index fell to its lowest reading in four years, new data showed, as Americans face higher costs and fret the fallout of President Trump’s trade policy. A second metric that measures Americans’ expectations about the economy’s future also reached a 12-year low. The findings show how the Trump administration’s tariffs, the trade war, and market volatility have begun to weigh on households. As economists warn of the rising odds of a recession, consumers are also facing sticky inflation and higher borrowing costs.