Thought of the Week:

My first “real” job was at a company that stood just a block away from where SCOA’s Washington office sits today. During, and following, my senior year in college, I landed a role as a public relations assistant at a sports marketing outfit. ProServ was the name of the firm founded by former Davis Cup captain Donald Dell to represent tennis stars such as Arthur Ashe, Jimmy Connors, and Stan Smith. It became incredibly famous for inking Michael Jordan’s Nike shoe contract and launching the Air Jordan brand. My job was simple—maintain files, mail out press packets, produce highlight tapes (they really were tapes), and manage the Ivan Lendl fan club. At the time, Lendl was the number 1 tennis player in the world, and the requests for hand signed pictures, balls, racquets, and other collectibles were overwhelming; it’s no exaggeration to say we couldn’t physically open all the mail (yes, snail mail) he received each and every day, and it goes without saying that I got pretty good at signing Lendl’s name with a Sharpie. A different type of signature is in the news today, one made by autopen. According to several Republican reviews, many of the documents, including pardons, signed by President Biden over the course of his presidency made use of an autopen; an autopen is simply a device used to make automatic or remote signatures. The implication being that through use of the autopen, others, without the president’s knowledge, may have taken executive action on their own, which should render those auto-signed documents invalid. While MAGA-aligned Republicans press the courts to vacate controversial last-minute pardons signed by autopen, Democrats say such Trump administration efforts to overhaul the federal bureaucracy, limit birthright citizenship, eliminate DEI practices, and use the Alien Enemies Act of 1798 to deport Venezuelan nationals deemed terrorists, represent the most significant test in history of the U.S.’s system of checks and balances. Calls from both sides that the country is in the middle of a constitutional crisis, while concerning, seem overblown and wildly out of context. For one, successfully challenging President Biden’s use of an autopen is low. Various White House counsel’s offices have studied the issue and concluded that any president may sign a bill by directing a subordinate to affix the President’s signature, for example by autopen. In addition, the courts are unlikely to presume conspiracy, any challenge would have problems with standing, and President Biden acknowledged many of the signings, including those for pardons, publicly. Second, claims that the Trump White House will overthrow the Constitution and govern by decree might be credible if they weren’t so blatantly partisan. We never heard similar claims from progressives when President Biden forgave $400 billion in federal student debt or claimed emergency powers to require mandatory vaccinations. While there’s no doubt that unwarranted use of presidential power could cause a constitutional crisis, neither the autopen controversy nor Trump actions come close to the constitutional crises of the past. Consider President Washington’s claim of control over foreign relations; Andrew Jackson’s promise to close the Bank of the United States (today’s Federal Reserve); President Lincoln’s actions during the Civil War; or even FDR’s threat to pack the Supreme Court. To date, while the most recent Biden and Trump controversies seem more political noise that imminent crises, if you’ve ever happened to pick up any vintage signed Lendl sports memorabilia circa 1986 or 1987, you might want to get those verified for authenticity.

Thought Leadership from our Consultants, Think Tanks, and Trade Associations

Bloomberg Government Finds Slim Evidence that “Buy American” Efforts Work. To counter opposition to tariffs, President Trump has been telling supporters that buying products made in the U.S. will strengthen the economy. His is the latest “Buy American” appeal in a country that can trace such moves back to the Boston Tea Party. Yet, whether Buy American campaigns actually work depends on how one defines success. The most obvious indicator would be a durable, even if marginal, reversal in consumption trends at a national level. However, there is little evidence to this effect, although the data is somewhat muddled. The biggest Buy American campaigns have been introduced during recessions and paired with onerous tariffs, both of which on their own reliably tank the number of goods entering the country, according to the Federal Reserve. The same data shows that once a recession ends, imports tick back up to their previous trend line very quickly. If nationalist sentiment alone were enough to change American consumer habits, you’d expect to see that move the needle in ways that don’t adhere so tightly to the nation’s overall economic conditions. It also does not appear that Buy American campaigns grow or sustain the number of manufacturing sector jobs. What’s more, in a modern world of globalized supply chains, it is difficult to identify goods or services as straightforwardly foreign or domestic. Buy American campaigns do work in one respect—they turn consumers’ attention during tough economic times toward foreign producers, rather than toward domestic leaders. Supported by domestic corporate interests, Buy American campaigns take existing dissatisfaction and unrest among American workers and reorient them away from domestic powers and toward foreign threats. Suddenly the most important relationship isn’t between workers and owners, but between Americans and their foreign opponents—and U.S. business can more easily cast itself as an ally of the everyman.

The Conference Board’s Latest U.S. Economic Forecast. The unpredictability of Trump administration policy looms large over the outlook. A combination of potential tariffs on imports, substantial policy uncertainty, a sizable pullback in consumer sentiment and spending, elevated geopolitical tensions, and a reduction in federal spending has led analysts to revise down projections for growth over the forecast horizon. Simultaneously, both implemented and proposed trade, immigration, and fiscal policies will likely raise inflation. The impact of tariffs, DOGE layoffs, and policy uncertainty may also weigh on payrolls in the coming months and push the unemployment rate higher. Such “stagflationary” developments could lead the Fed to face hard choices with respect to its dual policy mandate of full employment and price stability. However, the negative impact on growth will likely overwhelm the impact of higher inflation, and result in the Fed reducing policy rates in H2 2025; three rate cuts should be expected—in July, September, and December. The economy should expand 2.0% year-over-year in 2025 (below the 2.3% growth projected in the February forecast), and U.S. real GDP growth in 2026 should settle below its potential rate of 2.0%. Inflation may rise in the coming months due to tariffs but will ultimately stabilize as possible growth jitters weigh on demand. Inflation should continue to normalize toward the Fed’s 2% target in 2026. Against this backdrop, the Fed will probably remain patient in the coming months and leave rates unchanged until there is more clarity on how the administration’s policies affect the economic landscape. The view remains that the central bank will resume normalizing policy this year, although the risk is that the Fed could err more on the side of caution and delay policy normalization given the pick-up in inflation expectations. The Fed will likely reach its long-run neutral rate target range of 3.00-3.25% by the middle of 2026.

Observatory Group Says Forced Divestment of Chinese-Owned Firms may be Coming. The America First Investment Policy memo is one of several recent actions by the Trump administration against China, and it comes despite public statements by President Trump that he wants to meet with Chinese President Xi. Despite hype over the meeting and the prospect of improved U.S.-China relations, the base case is that the relationship will deteriorate over time and global companies with an interest in both countries should prepare accordingly. Trump 2.0’s nationalist faction is currently dominant over the growth advocates vis-à-vis China, and the nationalists are blocking the foundations for any détente, setting the U.S. on a path to escalation, and speeding up decoupling in trade, production, and investment. The memo instructs the Committee on Foreign Investment in the United States (CFIUS) to tighten restrictions on investments in key sectors such as tech, agriculture, and infrastructure by Chinese companies as well as those from other adversarial nations. Should relations sour enough, forced divestment may also occur. Divestment is a long-term play by the nationalists, but the mandate could come quickly, and investors should be prepared. It is also possible that current Chinese owners may anticipate problems and transact in advance. In addition, the memo encourages investment from companies based in allied nations, especially firms that can prove they do not have Chinese ties. As an inducement to invest, the memo proposes that companies fitting such parameters will have their security reviews fast-tracked. The memo puts every company and investor on notice that they will have to choose sides in the decoupling, and the risk of forced divestment should prompt urgent contingency planning for companies in the U.S. or its allies interested in acquiring firms that are Chinese owned; planning should also cover risks of retaliation by the Chinese government.

“Inside Baseball”

According to Punchbowl New, it’s never too early to look to 2026 where the Senate map seems unfavorable toward Democrats. So, the House will likely be the only game in town for the minority party in Washington. Unlike the early days of President Trump’s first term in March of 2017, Democrats don’t find themselves with the type of political wind at their back that would indicate any sort of favorable result. At a similar point in 2017, Democrats held a nearly 7-point advantage in the generic ballot; this time, the latest NBC poll gives Democrats just a 1-point generic ballot lead and clocked the Democratic Party with its lowest-ever approval rating in the survey’s history. At this point in Trump’s first term, Democrats had the beginnings of a wave that ultimately transpired. But with a president as popular as ever and a shrinking House battlefield, 2026 is trending toward a political knife fight for the fourth cycle in a row.

In Other Words

“J.D. Vance, to me, is the frontrunner. And the likely nominee in 2028,” Sen. Daines (R-MT) on his 2028 Republican presidential candidate prediction.

Did You Know

According to the most recent NBC News poll, the percentage of voters who say America is on the right track is at its highest level since 2004; at the same time, 54% of voters disapprove of President Trump’s handling of the economy, the first time he’s ever had majority disapproval on that metric.

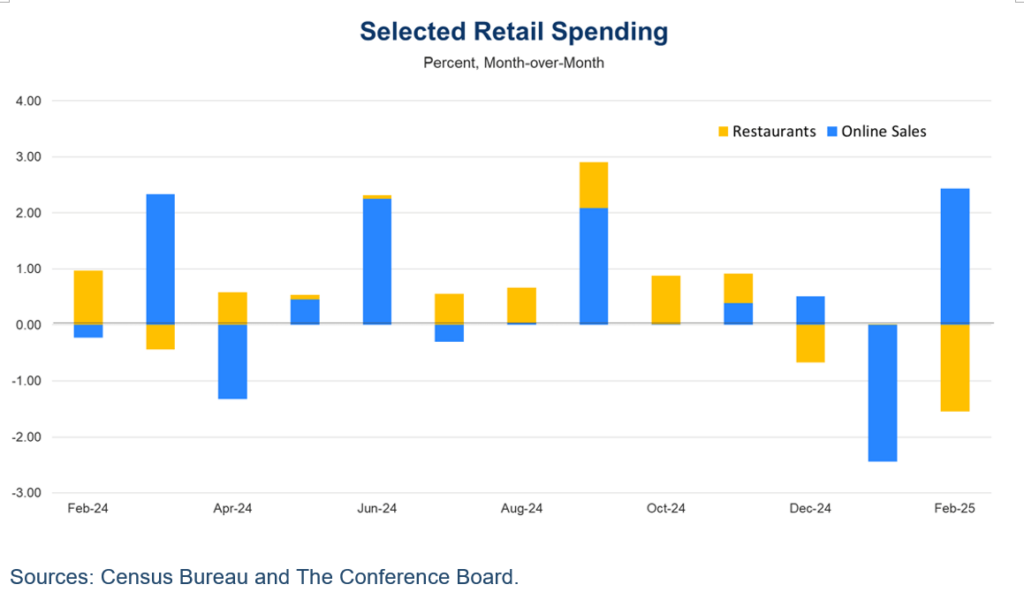

Graphs of the Week

February’s weaker-than-expected rebound in retail sales highlighted consumer pull back from discretionary spending as growth in sales was concentrated in necessities. Such consumer behavior corroborates estimates that consumption growth will slow this year, limiting overall economic growth. Redirecting dollars towards necessities that have become more expensive, and away from durable goods such as cars, furniture and electronics, shows that declines in consumer optimism are starting to materialize in the hard data. While the data does not suggest consumers are in crisis mode, the latest report does show consumers are becoming more cautious amid an uncertain economic outlook and rising prices.