Thought of the Week:

Thought of the Week:

What do Ted Williams, Michael Jordan, and Wayne Gretzky all have in common? That they were the greatest players of all time in baseball, basketball, and hockey, respectively? A good guess, but another answer might be that each was also a terrible head coach or general manager. In fact, if one looks across major American sports, they’ll notice that it is a rarity to find a star player who has made it as a successful coach. Although there are exceptions to every rule, stemming from the different skill sets required for each role, the notion that great players make poor coaches or managers is a common one. No doubt, exceptional playing ability doesn’t necessarily translate to managerial success. The very different skill sets required for success do not merely exist within athletics; consider business and politics. Although Warren Harding was very successful in business, he is consistently rated as one of the worst post-nineteenth century presidents. Conversely, Harry Truman, who failed in business, became a great president, and numerous surveys have shown that in the modern era, the number of successful businessmen who became successful presidents equals the same number of successful presidents who were successful businessmen—zero. Although it may be still too early to tell whether President Trump’s business acumen will translate into his success as a president, his repeated efforts at economy-wide interventionism risk damage to America’s market system. While I might be trapped in my own business school structured mindset, macroeconomic theory suggests that President Trump’s unilateral directives—to retailers, technology firms, and pharmaceutical companies—represent more than just flawed economic and financial policy, but strike at the essence of efficient market function. What has driven American prosperity is the combination of limited government and a rules-based free market system; “Trumponomics,” in the form of universal and reciprocal tariffs, pressure on retailers to “eat” costs rather than raise prices, direction on where firms should locate facilities, and demands on companies to meet arbitrary price targets is neither of these. Each intervention substitutes gut feelings for market intelligence, and embody Friedrich Hayek’s Fatal Conceit—the idea that “man is able to shape the world around him according to his wishes” and the assumption that politicians through industrial policy can orchestrate economic activity better than millions of consumers, businesses, and investors making independent decisions. Central planning distorts both the price mechanism and market incentives. Without profits and losses to guide business decision making, the motivations behind corporate efficiency and technological innovation tend to diminish (a direct argument against the type of rent seeking industries such as steel seek through protectionist tariffs). Trump administration industrial policy hinders the free flow of information conveyed by prices, scarcity, and preferences, and makes rational business calculations more difficult. What’s more, industries thrive on predictable rules, not political whims. We have already begun to see in the statistics businesses respond to uncertain White House trade policy with risk aversion and diminishing investment. Just as great ballplayers rarely make great coaches, the irony is that President Trump’s market micromanagement may ultimately undercut the economic dynamism he so often champions.

Thought Leadership from our Consultants, Think Tanks, and Trade Associations

Eurasia Group Predicts Declining Soft Power will Threaten U.S. Business Operations and Sales Abroad. The longstanding benefits of U.S. soft power—rooted in culture, values, and diplomacy—for American businesses—including increased global trust, easier market access, and favorable regulations—are on the decline, challenging the license to operate for U.S. companies overseas. As this advantage wanes, American firms will face growing challenges related to brand reputation, customer loyalty, regulatory hurdles, talent acquisition, and influence over global standards, with notable impacts such as consumer boycotts, increased preference for local competitors, and higher compliance costs. As the U.S. withdraws from international influence and takes a step back from foreign aid and supply chain human rights concerns, American companies will face challenges implementing their supplier codes of conduct. This will be reflected in reduced technical assistance, fewer monitors and reporting tools, and a weaker ability to shape supply chain regulations. Meanwhile, other competitors such as China are aspiring to fill the gap and expand their own influence in key regions. Chinese expansion offers opportunities—access to its markets, FDI, and joint ventures—but also brings tougher competition and regulatory hurdles.

Inside U.S. Trade Reports that Judges Targeted ‘Political Question’ in Tariff Hearing. Judges on the Court of International Trade (CIT) spent most of this week’s hearing addressing whether President Trump’s decision to use the International Economic Emergency Powers Act (IEEPA) to impose new tariffs on U.S. trading partners is a “political question” exempt from judicial review, appearing to narrow their focus in what has been wide-ranging litigation over the duties. State challengers claim that IEEPA does not authorize tariffs, and that even under a broad reading of his emergency powers the president has not shown that the duties “deal with [an] unusual and extraordinary threat” as the law requires. While much of the hearing was devoted to the question of whether an IEEPA provision allowing the president to “regulate … importation” in an emergency covers the power to set new tariffs, the judges spent little time on that subject. They focused instead on the “unusual and extraordinary” bar—questioning the plaintiffs on how courts can administer such a standard and the Justice Department on its position that whether an emergency order meets that test is a “political question” exempt from judicial oversight. While the White House argued that only Congress can review a president’s choice of actions under IEEPA, the judges worried that judicial oversight of IEEPA actions could limit the president’s ability to address genuine emergencies. The judges returned many times to the 1974 precedent known as U.S. v. Yoshida, where the Court of Customs and Patent Appeals upheld Nixon-era tariffs issued under IEEPA’s predecessor law, the Trading with the Enemy Act. While the DOJ repeatedly argued that Yoshida definitively establishes that IEEPA allows tariffs, the states countered that IEEPA’s language should be read more narrowly and that judges can review the president’s actions to ensure they have a “reasonable relationship” to the emergency. In fact, the states argued that persistent U.S. trade deficits cited to justify “reciprocal” tariffs are not “unusual and extraordinary” threats. As noted, the judges spent relatively little time on whether IEEPA allows tariffs at all, reasoning that that IEEPA’s explicit power to impose embargoes implies the ability to take the “lesser” step of imposing tariffs.

Observatory Group Sees Treasury Secretary Bessent Shifting Trade Policy Towards Economic Security Against China. Treasury Secretary Bessent, USTR Greer, and others in the Trump administration have coalesced around a “Trade 2.0” policy, sidelining more nationalist voices in doing so. The new policy uses the leverage created by reciprocal tariff policy to build an economic security ringfence around the U.S. and its military allies to improve the U.S. position vis-à-vis China. The clearest example is the U.S.-UK deal. Under its terms, the UK gives the U.S. explicit authority to raise red flags about conduct of any UK business in specific sectors for which the U.S. agrees to tariff reductions—starting with metals and pharmaceuticals. These concerns cover investment, ownership, and conducting business relations with adversarial nations (i.e. China). The UK has also pledged to cooperate with the U.S. on security via investment screening, export controls, and ICT (tech) vendor security. Perhaps the most disruptive part of the agreement is a provision that changes UK policy regarding forced labor in supply chains. This is likely to result in changes to UK green tech suppliers, as most procurement is from China—in effect, exporting elements of the U.S.’s China policy. Expect that deals with Japan, South Korea, and Australia will contain similar elements, also in exchange for tariff breaks on certain sectors with national security significance. The deals are likely to include investments in areas where the U.S. is weak—maritime capacity, battery technology, legacy semiconductors, and extraction and refining of rare earths and critical minerals. The U.S. is likely to pursue similar objectives with unallied trade partners. For example, it would like preferential access to pharmaceuticals and their ingredients from India, and refined critical minerals from Malaysia, backed by secure supply chains and plant ownership. For any deal, President Trump will need to include talking points for opening markets, but the thread running through “Trade 2.0” is addressing China by creating stronger economic alliances and constructing secure supply chains.

“Inside Baseball”

Ratings Downgrade Not Enough to Shock Political System into Action. Last week, Moody’s became the latest major ratings agency to downgrade the U.S. from its highest level. The agency cited federal debt and rising interest payments as key factors behind the move. The downgrade reflects the reality that political dysfunction is behind Congress’ limited progress in tackling fiscal challenges related to the mismatch between rising entitlement costs and tax collections. The downgrade will not derail the tax bill’s progress on Capitol Hill, but it does provide another point for fiscal hawks pushing deeper spending cuts. The downgrade potentially opens the door to high-income tax increases, floated by President Trump, but market conditions would have to deteriorate for the Senate to add those in at this late date. Republicans are unified around ensuring taxes do not go up and on delivering President Trump’s campaign promises of additional cuts. Fiscal conservatives will, however, use the downgrade to accentuate what they see as the need for significant cuts to Medicaid and the Supplemental Nutrition Assistance Program, and it will bolster their case that the Senate should not water down the House’s draft cuts.

Reconciliation Reality. Although it will be reported that Speaker Johnson (R-LA) delivered a win in passing the reconciliation bill before Memorial Day, a win on Capitol Hill does not necessarily equate to a political win. The vote represents the framework for both parties’ messaging on major issues like taxes and health care in the runup to 2026. Republican candidates will defend the vote on the premise of tax cuts and immigration, while Democrats are prepared to convince voters they will lose health care under ths bill. Only time will tell how much of a win this was for Republicans as the messaging wars are about to begin.

In Other Words

“We want more balanced trade, and I think both sides are committed to achieving that…Neither side wants a decoupling,” Treasury Secretary Bessent at a briefing in Geneva concerning U.S.-China trade.

“A friend of mine who’s a businessman—very, very, very top guy, most of you would have heard of him—a highly neurotic, brilliant businessman, seriously overweight, and he takes the fat shot. And he called me up…he’s a rough guy, smart guy, very successful, very rich … ‘Mr. President, could I ask you a question? I’m in London, and I just paid for this damn fat drug I take.’ I said, ‘It’s not working,’” President Trump discussing drug pricing.

Did You Know

Connecticut, Georgia, and Massachusetts didn’t ratify the Bill of Rights until 1939, the 150th anniversary of congressional approval of the amendments.

Graphs of the Week

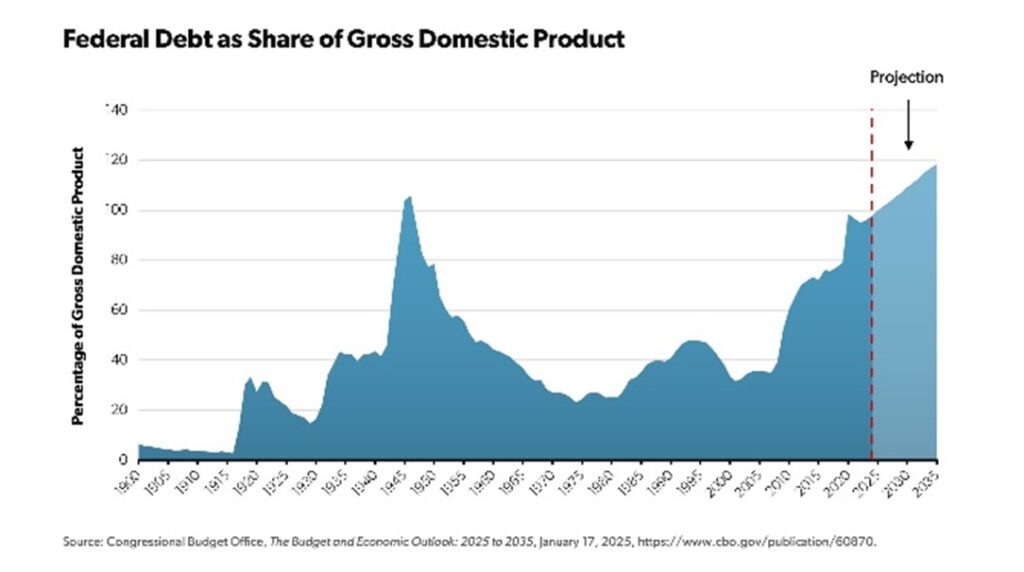

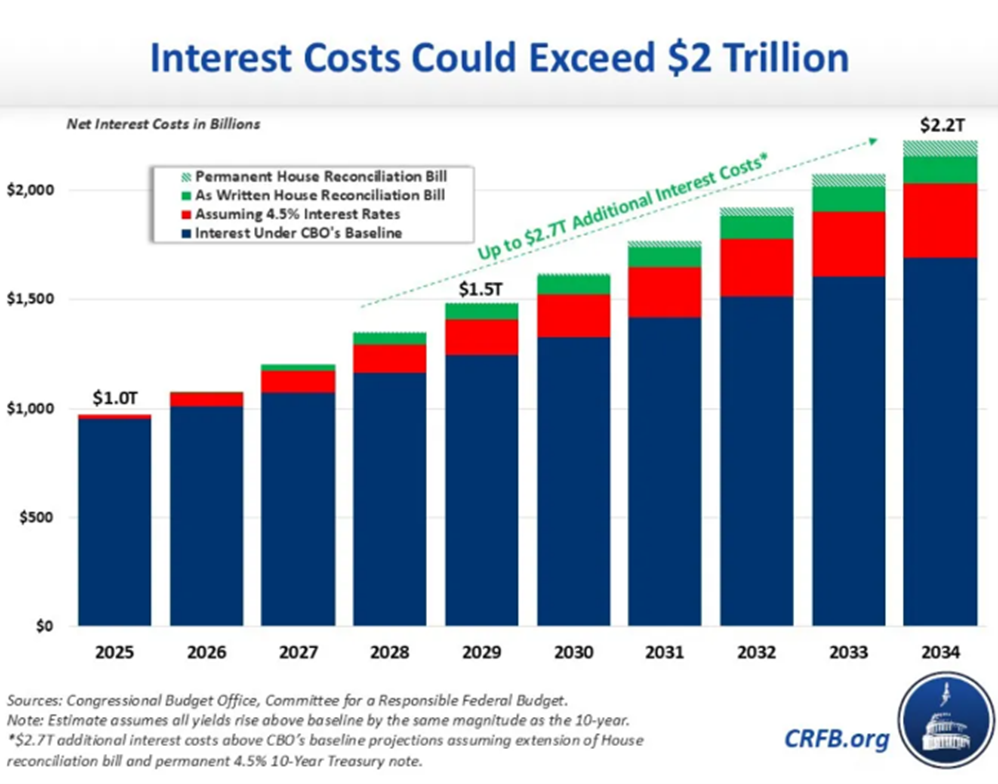

By 2035, the Congressional Budget Office (CBO) projects federal debt will reach 118% of GDP. To correct the skyrocketing deficit, Congress needs to address entitlement spending rather than discretionary spending. What’s more, if current tax rates are maintained, the federal debt is projected to expand to over 200% of GDP over the next three decades; the last time the federal debt equaled the size of the economy was during World War II. While entitlement spending accounts for a larger percent of the federal budget than discretionary spending—50% to 14%, respectively—as the federal debt climbs and interest payments consume a growing share of the budget, critical investments in defense, diplomacy, and domestic priorities will be put at risk. Although debt is neither inherently good or bad, excessive debt constrains policy options and creates risk. This erosion of fiscal space is no longer theoretical; it is already reshaping America’s strategic posture. The most consequential manifestation of the shift can be seen in the changing dynamics of global capital flows, particularly the U.S.’s growing dependence on sovereign wealth funds. Trends suggest that the window for enacting meaningful reform—particularly re: entitlements; tax; and discretionary spending—without painful consequences is closing. The longer reform is delayed, the more disruptive eventual adjustments will have to be.