Thought of the Week:

There is the seen and the unseen. In Washington, Congress can quite literally be seen in action when it is in session. But when it’s in recess, like it has been for the past two weeks, Capitol Hill is somewhat of a ghost town. In economics one can also find the seen and the unseen. Perhaps the finest articulation of this concept is Frederic Bastiat’s broken window fallacy. In the parable “What is Seen and What is Unseen,” Bastiat tells the story of a boy who breaks a shop window, and in the end, the townspeople conclude that the boy has actually helped the local economy. Their reasoning comes from what can be seen. The shop owner employed a glazier to repair the window, who, in turn, gained extra income. The glazier used that income to spend in other shops, which created a local multiplier effect. Overall, it appeared that the local economy had benefited from the flurry of activity stemming from the broken window. However, Bastiat explains that the local population failed to consider what was unseen. In having to spend money on repairing the window, the original shop owner was denied the ability to spend those same funds on a more efficient production process, which would have led to a rise in net investment rather than just the gross investment of replacing a broken window. In fact, the repair of the broken window did not increase the stock of goods and services at all; it just merely replaced what was already there. When considering both the seen and unseen, it can be concluded that breaking a window and repairing it, the seen, leads to an inferior outcome to the alternative of increasing the stock of new capital, the unseen. Bastiat’s principle can be applied to Washington’s most seen policy prescription of the day—tariffs. While policymakers have used tariffs as a political tool for centuries, they typically focus on the seen—the local benefits that flow from reduced competition and increased domestic production—without accounting for the negative effects that remain unseen. Although it’s true that by making imported goods more expensive, tariffs give local industries a competitive advantage in the short term (a benefit politicians highlight as evidence that tariffs “work” to protect jobs and boost domestic production), what remains unseen are the long-term damages that protectionist policies inflict on an economy, including:

- Higher costs for consumers and businesses. The unseen effect is that tariffs act as a tax, reducing consumer spending in other areas of the economy and increasing input costs for business.

- Disrupted supply chains. Modern production processes involve complex cross-border supply chains. If tariffs are applied at each crossing, costs escalate quickly, making final products more expensive and less competitive than they otherwise would be. The unseen effect being the disruption of industries that depend on smooth, tariff-free supply chains.

- When one country imposes tariffs, trading partners often retaliate, leading to a downward spiral of reduced trade. During the Smoot-Hawley era, global retaliation to U.S. tariffs contributed to a 60% decline in world trade. The unseen effects include lost exports, reduced foreign investment, and weaker trade relationships.

- Reduced productivity and innovation. Protectionist policies shield domestic industries from competition, reducing their incentive to innovate or improve efficiency. What’s unseen is the lost growth that could have been achieved through free competition and exposure to global markets.

- Structural economic damage over the long-term. Tariffs distort market incentives to allocate resources efficiently. Uncompetitive industries receive protection, while more efficient sectors are denied increased investment. The unseen consequence is long-term structural weakness, making the economy vulnerable to external shock.

So, while this post can been seen at any time, I’m going on vacation, and I won’t be seen for a week. You can catch my next blog on May 9.

Thought Leadership from our Consultants, Think Tanks, and Trade Associations

Trade Analyst Laura Chasen Talks Tariff Launch—Japan Leads, Others Engage, but the Endgame Remains Unclear and Remote. Last week saw the start of formal talks with several trading partners, led by Japan, aimed at reaching some sort of bilateral deal that President Trump could use to claim victory and thus lessen the tariff burden on a particular country. Although there are no indications that the President is willing to accept a complete end to his special new tariffs with any specific trading partner, as opposed to reducing them or giving cave-outs to specific companies or countries, the talks have been complicated by the fact that the administration has not offered any clarity on just what it wants from the talks. Japan has been declared a priority for talks while at the same time being slapped with a relatively high 24% reciprocal tariff rate—temporarily cut to 10% during the “pause” (as a major exporter of autos/parts, steel, and aluminum, Tokyo is particularly hurt by the 25% tariffs imposed on those sectors). Economists say Japan could lose about 0.8% of GDP if the tariffs remain in place. As spelled out thus far, President Trump’s demands are tough—calling for cuts to agricultural tariffs beyond what Japan conceded in the U.S.-Japan Trade Agreement, concluded under Trump’s first presidency; and Japan’s non-tariff barriers in key sectors including autos, seafood, agriculture, and medical devices are understood, at least from the U.S. side, to be on the table. Although cutting a deal is of great importance to both sides, it seems that to get there, one, or both, would have to make significant concessions. While it’s still early, and only the first round with Japan has been completed, officials made upbeat comments about how talks are progressing. One thing that is clear is that the U.S. is interested in winning concessions from Japan that go beyond the trade sector, e.g., a commitment to increased defense spending, more military purchases from the U.S., as well as more host-country burden-sharing. Closely tied to trade, the question of foreign investment is also figuring in the talks. The White House wants more investment in the U.S. The Trump team has also used the talks, with Japan and others, to try to force China’s isolation. Such efforts are meant to put a dent in China’s already struggling economy and force Beijing to the negotiating table with less leverage.

Eurasia Group Sees Federal Reserve Chair Powell as Safe Even if Courts Expand Executive Power. The courts are currently considering cases that involve the 90-year-old Supreme Court precedent protecting members of independent boards and commissions from at-will removal by the president. Fully overturning the precedent could allow President Trump to fire Federal Reserve Chair Powell, undermining central bank independence and injecting even more uncertainty about the U.S. investment climate into already jittery markets. While a ruling could come from the Supreme Court as soon as June, if the court sits on the case, a ruling would be expected in the second half of the year or in 2026. Although it remains unlikely that President Trump will fire Chair Powell before his term expires in May 2026 (20% odds), that likelihood increases if the Supreme Court effectively gives the president the green light to do so. Still, the biggest element in Powell’s favor is that firing him with only a year left in his term is not worth the economic and financial fallout that a dismissal would engender in financial markets already doubtful about the investable climate in the U.S. President Trump’s backdown on reciprocal tariffs indicates that financial markets can still operate as a check—though not a definitive one—on the administration. Keeping Powell in place also meets a political goal for Trump, as it would allow him to place the blame for a potentially slowing economy on the Fed—thus deflecting it from the White House.

Inside U.S. Trade Observes an Administration at War with Itself Over Tariff Plans. The White House is locked in “a war with itself” over whether to make President Trump’s “reciprocal” tariffs permanent or lower them as it forges bilateral trade deals. The primary fear being that the White House may be unlikely to continue negotiating if it cannot secure at least a few “real” agreements by the end of a 90-day pause on duties. Even though the administration is actively in talks with a list of countries targeted for “reciprocal” tariffs, there is a divide between officials who consider the duties “a negotiating ploy” to be ultimately lowered or eliminated through bilateral deals and those who want to keep them in place despite “substantial financial risk.” For the first group, the end goal is getting to low, uniform tariffs, but the second view, which is associated with White House trade adviser Navarro, is not a low baseline tariff, but maintenance of high tariffs to reshore as much manufacturing as possible. Which camp ultimately prevails could be decided by whether the administration successfully negotiates lower barriers to U.S. exports during the 90-day “pause.” To date, the White House has publicly embraced the negotiation approach. At the same time, others hold that the administration’s primary tariff and trade agenda is focused on limiting Chinese economic expansion, particularly in manufacturing—the overall goal being to get a coalition of countries to put more pressure on China. As the U.S. continues to make deals with its closest allies—the UK, Japan, Korea, and Australia—there will be a desire to copy the framework to be developed under USMCA renegotiation. For this reason, expect high tariffs to remain on Chinese exports indefinitely, with baseline rates in the range of 35% to 50%. Some analysts counter that Trump’s escalation of policy tensions with U.S. trading partners means they will be less likely to follow the U.S. lead on China, and they argue that in order to effectuate change, the U.S. should be working hand-in-hand with trading partners instead of alienating them. In the long-run, it may be that the Trump administration will not be able to keep many of its newly enacted tariffs in place without action by Congress; the duties rely on a novel use of the International Economic Emergency Powers Act, and is already facing a number of court challenges.

“Inside Baseball”

President Trump’s recent ambivalence on daylight saving time has kicked off a lobbying frenzy. After calling on Congress to “eliminate” Daylight Saving Time in December, the president then called it a “50/50 issue” in March, before suggesting this week that lawmakers should make Daylight Saving Time permanent. In fact, President Trump’s latest comments set off a flurry of activity among a small but highly engaged cadre of lobbyists advocating for industries that would benefit from permanent Daylight Saving Time and those who want to stick with Standard Time. It’s an issue that has pitted the golf industry and retail interests against sleep doctors and Christian radio broadcasters, as well as people pursuing passion projects on both sides. Advocates are planning new outreach to the Trump administration—including Elon Musk’s Department of Government Efficiency and RFK, Jr.’s Department of Health and Human Services—as well as to members of Congress who came close but fell short in advancing legislation to make Daylight Saving Time permanent in 2022.

In Other Words

“No [plans to fire Powell] whatsoever. Uh, never did. The press runs away with things. No, I have no intention of firing him. I would like to see him be a little more active in terms of his idea to lower interest rates. This is a perfect time to lower interest rates,” President Trump in response to a question on whether the White House plans to fire the Fed Chair.

Did You Know

Pope Francis was the first Latin American pope, the first Jesuit pope, and, in 2015, became the first pope to address a joint session of Congress.

Graph of the Week

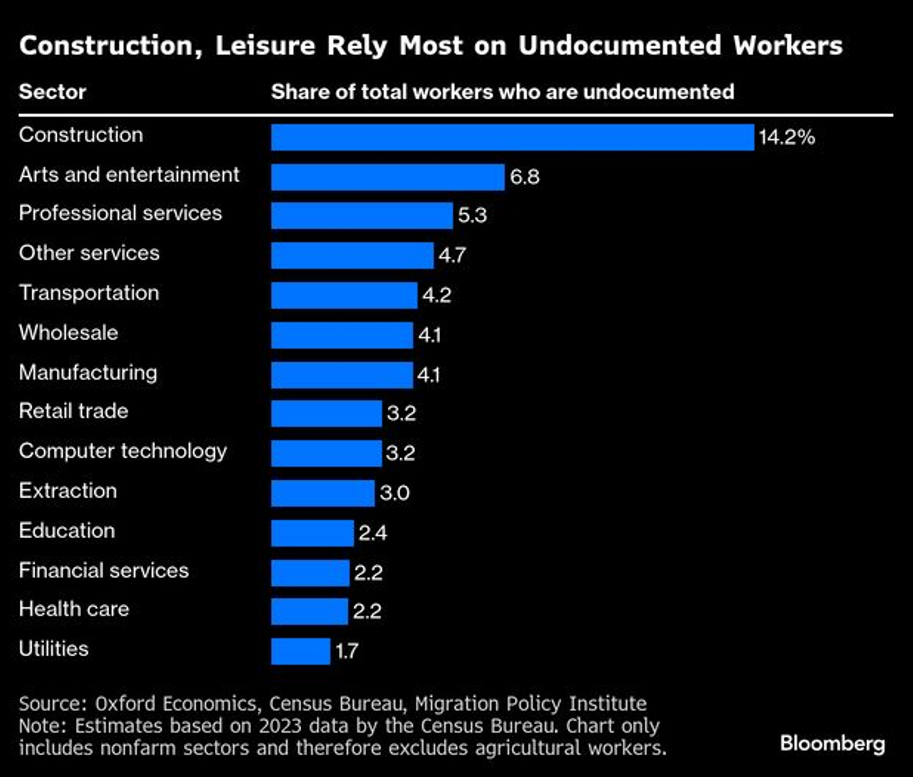

President Trump’s efforts to curb immigration are coming at a precarious time for the labor market, threatening to choke off a key growth engine just as tariffs are poised to drag down economic activity. Crossings of undocumented migrants came to a halt last month after surging to unprecedented levels during the Biden administration. While the crackdown is expected to intensify, economists say such action will reduce job creation and stoke inflation, exacerbating anticipated consequences of the administration’s trade policies, which are fueling recession fears. While the 5.5 million immigrants—undocumented and legal—who joined the workforce since 2020 helped fuel economic growth, current restrictions, and threats of mass deportations, risk derailing this trend. What’s more, not only has immigration fueled job gains, but it has also eased wage pressures across the economy. As tariffs increase price pressures, fewer available workers could make it harder for Fed officials to reach their goal of lowering inflation to 2%. At present, most economists and Fed officials say the labor market is in good shape, but longer term, curbing immigration may have profound implications as the workforce ages. In fact, the Congressional Budget Office estimates that without immigration the U.S. population could begin shrinking as soon as the next decade.