Thought of the Week:

The counterculture author and original gonzo journalist Dr. Hunter S. Thompson (seen above on the left with SCOA Corporate Communications Senior Manager Stephen Pitalo in 1995) is credited with the quote, “Half of life is just showing up.” Actor and director Woody Allen put his own spin on the quote, saying “80% of success is showing up.” I had my own “just showing up” moment last week on a business trip to Nashville. No, it wasn’t the presentation I gave; I actually put in quite a few hours constructing, tweaking, and practicing it. My moment came after the presentation, after the dinner, and after the conference concluded when several of us headed out to Music City’s famous Broadway. There, without prior notice, without any planning, we found ourselves smack dab in the middle of a pop-up Keith Urban concert. We were rewarded with an incredible live performance merely for just showing up. Every two years, and maybe more importantly every four years, politics has its own “just showing up” moment in November—it’s called Election Day. But how often have you heard someone say, “It doesn’t matter, my vote won’t count anyway.” Well, the 2000 presidential election was decided by a mere 537 votes out of 5,825,043 cast in Florida; in 2016, if not for 77,740 votes out of 13,940,912 cast across three states (Michigan, Pennsylvania, and Wisconsin), Hillary Clinton would have been the 45th president; and a just 44,000 votes out of 11,685,327 cast in Arizona, Georgia, and Wisconsin separated Joe Biden and Donald Trump from an Electoral College tie. These margins are so close they don’t even reach the level of statistical significance. In response to these recent election outcomes, a growing number of companies have recognized that “just showing up” is important and have launched internal Get Out the Vote (GOTV) campaigns. Companies that want to play an active, nonpartisan role in helping employees vote are doing such things as:

- Providing time off or adopting flexible schedules to make voting easier;

- Launching internal Election Centers to serve as one-stop shops for election information such as how to register to vote and where to get candidate information;

- Offering information on dates and deadlines, as well as links to election resources;

- Emailing reminders of dates, deadlines, and logistics such as the location of polling places; and

- Holding election-related events, including inviting analysts or candidates from both parties to speak.

While companies once shied away from elections, fearful they could alienate employees or customers, more are emphasizing greater involvement. Nonpartisan, information-based GOTV programs can be good business—they enable firms to engage their workforce directly and reinforce government affairs and corporate communications departments as trusted sources of information. What’s more, companies that facilitate civic participation and build trust also create groups of advocates who can be called upon to contact public officials in a time of need. In fact, a growing number of companies believe ignoring an election that dominates the national conversation may be in itself risky. Encouraging employees to “just show up” while maybe not the best days of their life also won’t be Wasted Time.

Thought Leadership from our Consultants, Think Tanks, and Trade Associations

Eurasia Group Recognizes that Global Markets Were Calmed by the Fed, but Now Must Confront U.S. Election Risks. The U.S. election is the most immediate geopolitical risk for global markets. Despite escalation risks that could still trigger “stagflationary” shocks, the conflicts in the Middle East and Ukraine have had less macroeconomic impact than expected earlier this year. Other geopolitical conditions challenging growth and constraining economic policy include China’s incremental approach and the EU leadership vacuum, although the U.S.’s monetary policy easing offered some offset. The Fed’s easing cycle began as a “recalibration,” aimed at a soft landing for the U.S. economy, provided tailwinds to markets, and has given emerging markets’ central banks more policy flexibility. While the Fed’s decision was not overtly political, it has significant domestic and international political ramifications. Should Trump win (EG’s base case) his inflationary policies could force the Fed to reverse course in late 2025, strengthening the dollar, and limiting policy space for emerging markets benefiting from current Fed easing. In such a scenario, the Fed’s independence would be tested. Markets are pricing in a tepid growth outlook with declining inflation and interest rates; a further supply shock—in the form of inflationary policies by an incoming Trump administration or commodity market or trade spillovers from the Middle East or Ukraine crises—would pose upside risk to interest rates and inflation volatility, as well as a significant downside risk to risk assets.

Eurasia Group Predicts Trump Likely to have Unified Government, but Harris Likely to Face Divided Government. Democrats stand to gain in the House, even as divided government remains the base case. At present, there is a 75% likelihood (up from 65%) that the House will flip to Democrats if Kamala Harris wins the presidency, while Donald Trump would still likely retain the House (60% odds) if he wins. While Trump would still likely carry the House on his coattails, Democratic gains in generic-ballot polling and in fundraising, as well as the Democratic tilt of the swing districts in this year’s election, have made a Democratic House under Harris more likely than ever. Republicans remain very likely to flip the Senate, with a pickup in West Virginia a near certainty and wins in at least one of Montana and Ohio likely; overall, the odds of a unified government under Harris have marginally risen. Divided government would matter more for Harris than Trump, as Trump would be able to enact major parts of his policy agenda—including immigration restrictions and higher tariffs—even if he did not control Congress; under Harris, divided government would lead to legislative gridlock, restricting the extent to which Harris can raise taxes, enact new spending programs, and confirm progressive nominees.

Inside U.S. Trade Reports that U.S. is Fully Reliant on Imports of Minerals for Key Security and Semiconductor Uses. The U.S. is almost entirely reliant on imports—including those from adversarial countries—for a slew of critical minerals with strategic defense and industrial uses, according to new research published earlier this week. In the report, analysts at Silverado Policy Accelerator (a think tank focused on trade, economic, and cybersecurity policy) identified 12 minerals they say pose the greatest threat to national and economic security because of the U.S.’ reliance on imports, the share of mineral production in foreign entities of concern (FEOCs), and the share of U.S. imports from FEOCs. The U.S. is either fully or almost fully reliant on imports for 9 of these 12 strategic defense minerals, and many of them also form the backbone of semiconductor production. This reliance creates critical vulnerability that could disrupt key industries if the supply is restricted or even suddenly cut off due to a variety of reasons, including government measures such as export controls or bans imposed for geopolitical or national interest reasons. In fact, the U.S. imports 100% of its arsenic, gallium, indium, natural graphite, scandium, tantalum, and yttrium. For rare earths and bismuth, the country imports more than 90% of its supply, and more than 80% for antimony, with FEOCs providing the bulk of those imports. Germanium and tungsten round out the list, with FEOCs dominating their production processes. Several of the minerals identified are already subject to Chinese efforts to limit exports. Last year, Beijing imposed export controls on graphite, gallium, and germanium and last month it unveiled new restrictions on antimony, a mineral with several uses in military applications, batteries, automobiles, toys, and airplane seats. Many of the minerals identified also have applications in the electric vehicle and battery manufacturing sectors, both key targets of the Biden administration’s reshoring efforts. Notably absent, however, are minerals like lithium, cobalt, and nickel that often dominate policy conversations about critical minerals and supply chain resiliency.

“Inside Baseball”

Observatory Group’s September Federal Reserve Review. Last week, the FOMC cut the policy rate by 50 bp, showed a median projection for another 50 bp in cuts by year end, and indicated a straight line to a terminal rate of 2.9% by sometime in 2026. The Fed avoided using any code word, not even “gradual,” to describe the policy outlook, saying in the statement only that in “considering additional adjustments to the target range” it will consider everything; the central bank did not even refer to a direction of adjustment. This may be a new norm for policy guidance rather than a true reflection of any internal conflict about continuing to cut rates. The dots are the guidance for now as we see the decision to cut by 50 bp combined with Powell’s mixed messages about whether policy is behind the ball as providing genuine scope for more rate cuts than the additional 50 bp the median 2024 dot now shows. Assessing the degree of behindedness is always as much art as science; so, unless the labor market steadies in the next two reports, an additional 50 bps in the 2024 median projection may be too little.

In Other Words

“If somebody breaks into my house, they’re getting shot. Probably should not have said that. My staff will deal with that later,” Vice President Harris.

“John Deere announced a few days ago that they’re going to move a lot of their manufacturing business to Mexico. I’m just notifying John Deere right now, if you do that, we’re putting a 200% tariff on everything you want to sell into the United States so that if I win John Deere is going to be paying a 200%,” former president Trump telling farmers at a campaign event that he will threaten the company with tariffs if they outsource their production.

“I guess it shows the economy is very bad to cut it by that much—assuming they’re not just playing politics. The economy would be very bad or they’re playing politics, one or the other,” former president Trump in response to the Fed’s rate cut.

Did You Know

Former President Trump is the second president to survive two assassination attempts following another attempt at his Florida golf course. The first was President Ford who survived two assassination attempts within 17 days in 1975.

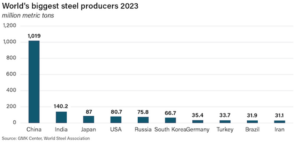

Graph of the Week

Global Steel Tariff War Sparked by China’s Construction Weakness Set to Worsen. China’s economic slowdown is depressing global steel and iron ore prices. As its domestic demand stalls and authorities avoid reducing surplus capacity, China’s steel exports could increase by 25 million tons to 115 million tons in 2024. This is triggering a wave of import duties as other steelmaking nations try to shield their industry from cheap Chinese exports; meanwhile, the stimulus package announced by Beijing will not change things in the near-term. Global steel and iron ore prices have both halved since their 2021 peaks, and many analysts believe they will slump further, unless China makes the necessary downward adjustments to its steel output.