Thought of the Week:

It’s spring break in Washington. Climb Capitol Hill, ride the Metro, or visit the National Mall, and you’re bound to see packs of teenagers in identical t-shirts roving the cityscape. For his spring break, a close friend brought his family from southern California to D.C. for the very first time. Among the sights, they toured the White House, the Capitol, the Smithsonian, and Arlington National Cemetery. Beyond being a visit back home for him, the idea was to introduce his wife to the nation’s capital and offer his young son some historical perspective. With President Trump’s Liberation Day tariff announcements last week and their subsequent 90-day pause, I couldn’t help but think of George Santayana’s old saying that “those who don’t know history are condemned to repeat it.” While the quote highlights the cyclical nature of history, where similar patterns and mistakes tend to recur, no doubt you’ve seen articles or commentary drawing parallels between President Trump’s tariffs and the Tariff Act of 1930, better known as the Smoot-Hawley Act. Smoot-Hawley imposed tariffs on approximately 25% of all imports to the U.S., raising the average tariff rate from 40% to 47%. Following its passage, trading partners responded with levies of their own, and as a result, U.S. exports to retaliating nations fell between 28% to 32%, nations that merely protested reduced their U.S. imports by 15% to 23%, and the Dow Jones Industrial Average slid precipitously, bottoming out in July 1932. Smoot-Hawley has long been recognized by leaders of both major parties as a mistake that severely damaged the U.S. economy. While FDR denounced them prior to taking office, eventually signing the 1934 Reciprocal Trade Agreements Act, decades later President Reagan famously remarked that “I well remember the antitrade frenzy in the late twenties that produced the Smoot-Hawley tariffs, greasing the skids for our descent into the Great Depression and the most destructive war this world has ever seen. That’s one episode of history I’m determined we will never repeat.” But Smoot Hawley isn’t the only historical trade parallel the current administration could draw upon. More than two centuries ago, President Thomas Jefferson signed into law the Embargo Act of 1807, which severely damaged the American economy by halting all international trade, ultimately failing to achieve its goal of forcing Britain and France to respect American neutrality. And like Jefferson, President Richard Nixon, a half century ago, embarked on an independent, unilateral course with unknown consequences. He rocked the international trading system by breaking the dollar’s connection to gold, levying a 10% tax on imports, and freezing wages and prices for 90 days; the plan flopped, created shortages, and fueled inflation. The parallels between Nixon’s New Economic Policy and “Liberation Day” provide a third cautionary tale for the Trump administration. Like Nixon who said unfair competition was behind the trade deficit and allies didn’t “bear their fair share of the burden of defending freedom around the world” (sound familiar), President Trump seems to be betting his legacy on an economic policy that experts deride while snubbing U.S. allies at the same time. In attempting to reshape the economy, both Nixon and Trump pressed their authority, used the heavy hand of government to protect manufacturing, implied they were open to negotiation, and viewed international competition as a zero-sum game. Perhaps Smoot-Hawley, the Embargo Act of 1807, and Nixon’s New Economic Policy have served as warnings to the White House after all. Just yesterday, President Trump said he is open to lowering or waiving the global 10% tariff he imposed on U.S. imports as part of his “reciprocal” tariff regime…depending on the concessions that U.S. trading partners offer. But if he’s not careful, history will repeat itself just like it did during my friend’s visit. The night before my friends left Washington, they attended the Washington Nationals, L.A. Dodgers game. That night, just as happened the night before, the Nationals beat the reigning World Series Champions.

Thought Leadership from our Consultants, Think Tanks, and Trade Associations

Capstone Says Trump’s Tariff Announcement Brings Policy Closer to Long-Term Strategy to Generate Revenue and Target China. On April 9th, Trump posted on Truth Social that his administration would pause the imposition of higher reciprocal tariff rates for specific countries for the next 90 days. Instead of raising rates as he had planned, the administration will maintain the 10% baseline tariff introduced on April 5th. We believe Trump’s announcement lays the groundwork for what will likely be a more durable version of his administration’s trade policy. Capstone previously forecasted that the 10% to 20% tariff range proposed by Trump on the campaign trail would be where the reciprocal tariff rates for most major US trading partners would land, and we continue to believe this. However, we note that tariff increases will still pose risks for tariff-exposed businesses. Countries that fail to offer meaningful concessions to the Trump administration may see tariff rates increase at the end of the 90-day pause. We also continue to believe that new, product-specific investigations targeting semiconductor and pharmaceutical imports are likely. Capstone does not expect Trump’s decision to pause the reciprocal tariff hikes to impact product-specific tariffs. We expect steel, aluminum, and autos to still be subject to the existing Section 232 tariffs. We believe President Trump’s decision to revert to a 10% baseline tariff from reciprocal tariff rates represents the long-term resting place for his trade policy. We do not believe this announcement precludes future tariff increases. We believe Trump will seek strategic decoupling with China through significant and durable tariffs, to raise revenue through universal tariffs, and to support the onshoring of strategic industries using Section 232.

Conference Board Makes Recommendations for Communicating Price Increases to Customers. Of the Trump administration’s actions to date, tariffs seem to be having the biggest impact on business, and 59% of Americans expect tariffs to increase prices. Although firms are negotiating with suppliers to reduce input costs and minimize customer price hikes, new tariffs are likely to result in higher prices for consumers. Companies can best communicate expected price increases by:

- Being transparent. Customers value proactive communication in times of uncertainty. Explaining increases and giving advance notice builds trust, while silence leaves room for interpretation.

- Remaining politically neutral. Unlike changes caused by supply chain issues or labor shortages, tariff-induced price increases may trigger political sentiments. Companies are best off remaining nonpartisan.

- Explaining how the company is working to mitigate price increases. Make clear that reduced margins are not sustainable long term and that price increases are a last resort.

- Coupling price increases with new product features.

- Offering more affordable product alternatives. Launching simplified versions is one way to keep products affordable amid rising costs.

- Considering new price promotions that reward loyalty. Such offers could include discounts for repeat purchases, longer-term commitments, or larger quantities.

- Ensuring consistent price communications to customers, employees, and investors. Message delivery should also be customized in terms of format, channel, and language for each audience.

- Preparing to explain higher profits after a price increase. Price increases could coincide with higher profits due to gaining customers, stockpiling, promotions, or other reasons that have nothing to do with the price increase itself.

Eurasia Group on Trump Establishing a Lower Tariff Wall. Although analysts had leaned into the view that President Trump was building a “durable tariff wall” to drive reshoring to the U.S., this week’s rapid capitulation provides a better understanding of the White House’s pain threshold and the administration’s appetite for destruction. The wall crumbled before companies were forced to raise prices, stop production, and/or lay off workers. It seems likely that it wasn’t the market sell off that led the administration to bend, but the disruptions in the financial plumbing [bond yields] that were threatening to spiral out of control. This suggests there is still space to escalate further against specific countries, although the administration is likely to be more targeted and deliberate in the future. With China, the only part of the wall left standing, it will become even more difficult for the two sides to draw down from their current stances. The Chinese seem prepared to ride out the storm, and the U.S. has centered them in the middle of their protectionist policies. While 125%+ tariffs are unlikely to be the endgame, it is unclear how negotiations will unfold, and there is no clarity on how they will begin. A credible end-result looks close to the Trump campaign plan: a 10% floor for most countries, a 60% tariff for China, and targeted sectoral tariffs that are negotiable at rates of around 25%. Sectoral tariffs, which are likely to be low enough to avoid broad economic disruptions, will be a key focus going forward, both for the industries they affect and the countries that export these goods.

“Inside Baseball”

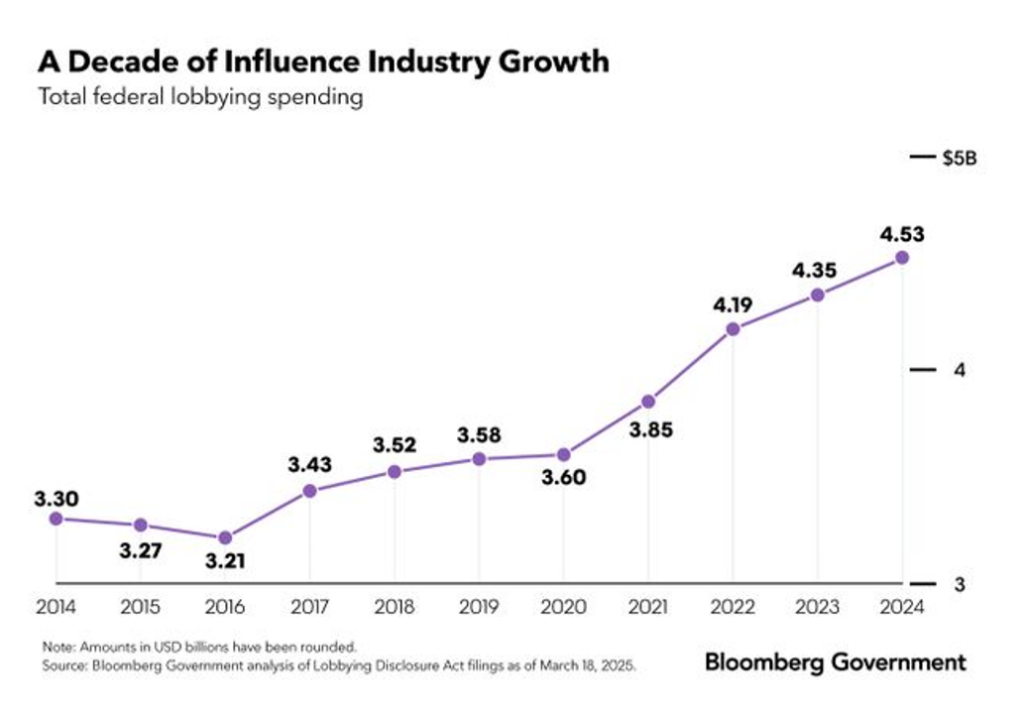

D.C. Influence Industry Spending Hit Record $4.5 Billion in 2024. While the yearend omnibus bill helped firms expand their revenue, total advocacy spending grew by 3.9%, outpacing inflation. In fact, Washington’s influence industry grew to a new high in 2024, with clients turning to lobbying professionals as they sought to shape federal policies. Required disclosures, which cover much but not all federal advocacy activity, showed $4.53 billion in spending last year, up from $4.35 billion in 2023. That revenue was driven by evergreen issues such as tax, health, and appropriations as well as emerging ones including artificial intelligence and cryptocurrency. The lobbying increase outpaced the 2.9% jump in the Consumer Price Index, reflecting a true expansion of overall lobbying income. Some of the largest firm registered double-digit gains, while smaller players doubled or in some cases tripled the amounts reported in Lobbying Disclosure Act filings.

In Other Words

“Well, I thought that people were jumping a little bit out of line. They were getting yippy, you know, they were getting . . . a little bit afraid,” President Trump after announcing a 90-day tariffs pause.

Did You Know

Seeking to avoid war with Britain and France, President Jefferson implemented the Embargo Act of 1807, which banned all U.S. trade with foreign nations. While the embargo’s aim was to cripple the English and French economies by denying them American goods, the action devastated the U.S. economy, particularly in the Northeast. In March 1809, Congress replaced the Embargo Act with the Non-Intercourse Act, which allowed trade with nations other than Britain and France.

Formula of the Week

The White House’s Tariff Formula. President Trump threw markets and the global economy into chaos with his tariff agenda—now paused for 90 days. Although the White House described their tariffs as reciprocal, meaning they should be equal to half the rate of tariffs and non-tariff trade barriers imposed by other countries, the American Enterprise Institute (AEI) broke down the formula used to calculate the tariffs and found significant errors. First, the tariff formula took the U.S. trade deficit divided by U.S. imports from a given country and divided that number in half. However, this neglects that trade deficits are composed of more than just tariffs and non-tariff trade barriers; capital flows, supply chains, comparative advantage, geography, and many other economic factors are also pieces of a trade deficit. Second, the formula used an elasticity of import prices with respect to tariffs of 0.25—it should have been 0.945. The Trump administration based their elasticity on the response of retail prices to tariffs rather than import prices. When correcting for elasticity, the resulting tariffs would be more than 30% lower than President Trump’s proposed tariffs. Following the administration’s pause, trade partners now have a 90-day reprieve before this tariff agenda, based on mathematical errors, may shock global trade again.